The valuation gap between US small-caps and their larger counterparts has grown “too wide”, according to Vanguard analysts, who said they expect the minnows to beat large-caps by some 1.9 percentage points per year over the next decade.

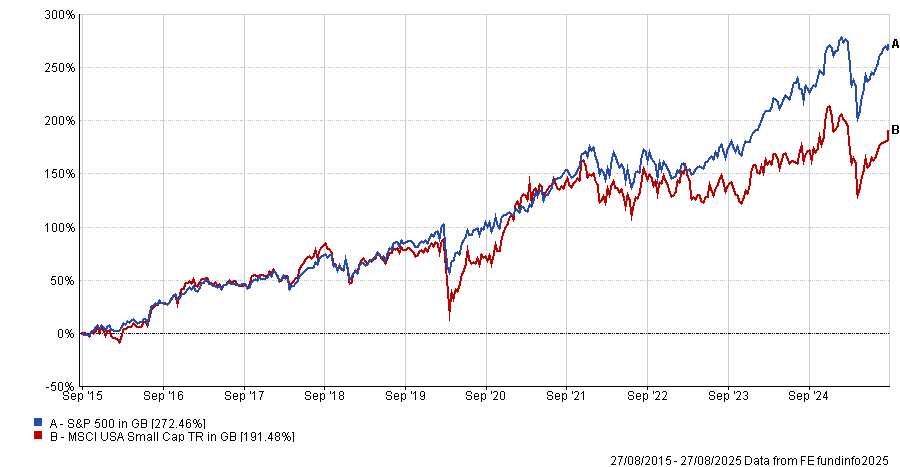

US smaller companies have underperformed for the past 10 years, with the MSCI USA Small Cap index some 80 percentage points behind the S&P 500 benchmark.

However, much of this underperformance came in the past three years, with both indices tracking relatively in line with one another from 2015 to 2022, as the below chart shows.

Performance of indices over 10yrs

Source: FE Analytics

Although smaller companies have begun showing signs of recovery in other parts of the world, in the US there is little sign of the gap narrowing between the smaller and larger end of the market.

Vanguard analysts said: “Tariff concerns are at least partly to blame, as small-caps have historically been more cyclical and economically sensitive.”

But there could also be structural forces at play. For example, they pointed to a deterioration in quality at the lower end of the market, with almost a third of the companies in the Russell 2000 Index making a loss in July, based on annual earnings per share.

This has factored into which companies come to market, with the quality of initial public offerings (IPOs) also falling – particularly in a world with an abundance of private equity money allowing businesses to stay private for longer.

“Much of large-caps’ vaunted valuation premium appears at least partly justified by their superior profitability,” they said.

There are many other factors as well. The dominance of the ‘Magnificent Seven’ stocks (Nvidia, Microsoft, Apple, Alphabet, Amazon, Meta Platforms, and Tesla) in the large-cap arena has disproportionately boosted returns, while technology is less prevalent down the market capitalisation scale (37% of the Russell 1000 and just 12% of the Russell 2000).

Interest rates have also hurt, with big businesses able to lock in lower rates on long-term debt at a time when the interest was cheap, while small-caps are more likely to structure short-term debt deals that roll over their debt at higher interest rate levels.

While the decline in small-cap valuations has been “arguably warranted”, the question is now whether it has gone too far.

Vanguard analysts noted that small-caps are cheap, so even without an obvious catalyst there could be potential to rebound.

“Even when limiting the universe to ‘quality’ companies (those with returns on invested capital of more than 20%), small-cap stocks appear very cheap compared with large-caps of comparable profitability,” they said, tipping the lower end of the market to outperform.

“However, some caution is warranted given the prevalence of small-cap companies with weak profitability and risky balance sheets. Investors may want to consider low-cost active funds where skilled managers can be selective or funds employing factor-based strategies emphasising quality and valuation,” they noted.

Imogen Harris, global smaller companies fund manager at Premier Miton, said it is not just in the US where small-caps have fallen heavily out of favour, however. Global small-caps are currently trading at a discount of 13% to large-caps based on their price-to-earnings (P/E) ratios.

This is a stark reversal from history, when smaller companies traded at an 18% average premium in the four years leading up to the Covid pandemic. This was known as the ‘small-cap premium’ and was given to these companies based on their potential for excessive future growth.

“Although small-caps have delivered higher earnings growth both over the past 10 years and since 2020, large-caps have delivered better earnings since 2022,” Harris noted.

“We have seen small-caps eating into this earnings gap over the past year, but valuation remains at this low ebb.”

Harris said that a loosening rate cycle is starting to become more likely, which should benefit minnow stocks and could provide a catalyst if earnings continue to improve.

Additionally, if there is a continuation of the trend towards more nationalistic tendencies (away from globalisation), smaller companies could benefit as they have “the ability to tap into the domestic markets and be insulated from political trade policies”.