Bond markets have developed a “false sense of security” that is blinding them to the risks on the horizon, according to FE fundinfo Alpha Manager Nicolas Trindade.

Part of this, he said, is because investors are struggling to look forward. For example, bond markets are underestimating the impact of tariffs, which have “only just started to bite”. Combined with a situation where credit spreads are tight, the market has become “unable to price risk appropriately”.

As a result, bond investors have started to trade quite aggressively, buying higher-yielding bonds because the risks are no longer clear.

“We’re in an odd environment where, because everything seems tight, you convince yourself that everything looks fine”, he said.

But this more aggressive approach to bond markets will backfire for many investors, he argued. “If you chase a rally right up to the end, you’ll often be too late when you try to move around the portfolio”.

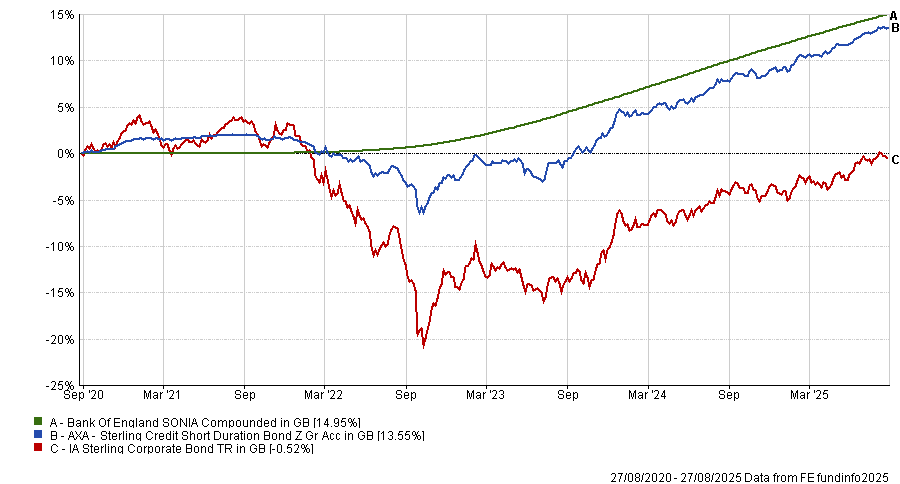

This more cautious approach has paid off for his AXA Sterling Credit Short Duration bond fund, which has delivered the second-best performance in the IA Sterling Corporate bond sector over the past five years.

Performance of fund vs sector and benchmark over 5yrs

Source: FE Analytics.

What’s the process of AXA Sterling Short Duration Credit?

We approach the strategy from a blend of top-down and bottom-up philosophies, because both are crucial.

In fixed income, we believe getting your macro calls right can help you decide your allocations efficiently, but all the value you add could be lost if you select the wrong security.

So we try to pick the names that are attractive not only from a fundamentals and macro perspective, but also in terms of their valuations.

What differentiates the fund?

I think what gives us our edge is our track record. The fund has been stress-tested through Brexit, the pandemic and the market meltdown in 2022 and has consistently delivered on its objectives during those periods.

We try to keep things simple. I think some managers tend to over-engineer and overcomplicate things by using swaps and derivatives that can leave investors confused about what the fund does.

At the end of the day, I buy bonds with up to five years' maturity. By going back to basics, you can offer attractive returns to clients who know exactly what they can expect from us.

What was your best call in recent years?

Starting in 2021, we became worried that inflation would rise more than the market expected, which would be a challenge because the level of yields was not high enough to offset this.

So we decided to decrease risk, reduce our duration and reduce our exposure to BBB bonds, which worked out for us when inflation surprised on the upside.

This put the fund in a strong position going into 2022, when spreads aggressively widened after the UK mini-Budget. We took the opportunity to add a lot of risk because we thought the yields looked very attractive and [prime minister Liz] Truss would have to backtrack because it wasn’t politically sustainable.

As a result, we were only down about 4% in 2022, while the short-dated corporate bond universe was down 8%.

And your worst?

I think our worst call was that we generally tend to be more cautious than the market has warranted, which has caused us to miss out.

For example, when we started to reduce risk and duration in the portfolio in 2021, we probably did it too early in hindsight; there was more upside on the table. But I’m fine with that. I wouldn’t mind being too early on the trade, because I think down the line it will pay off.

For me, I think it’s an easier conversation to have with investors if I capture less of the upside but less of the downside.

Why is it a great time for short-duration bonds in your opinion?

As an investor moving out of cash it makes a lot of sense because cash rates are coming down and the gap between short-duration bonds and cash yields is around 65 basis points, which seems compelling.

It’s a great way to lock in an attractive yield while derisking the portfolio because I think the steepening of the yield curve still has further to go.

The supply and demand picture is not very positive due to the high levels of government debt. Additionally, concerns about the Federal Reserve's independence could have a knock-on effect on UK gilts, particularly if the Fed starts cutting aggressively despite rising inflation.

For those reasons, you should probably expect the yield curve to further steepen, meaning you’re much better off at the shorter end.

Where are the most interesting opportunities right now?

At the start of the year, it was in UK water companies, which came under a lot of pressure due to what was happening at Thames Water. Investors put all of the sector in the same basket, as they tend to do, so we did a deep dive and found several bonds where we could benefit from effective valuations.

We also really like banks because they’re in a sweet spot. The yield curve right now is very steep, which is great for banks because they borrow short and lend long. They’re also not that impacted by tariffs and tend to be more domestic by nature.

What do you do outside of fund management?

I picked up Karate a few years ago with my son. He’s since stopped it but I’m hoping to complete my brown belt this year and my black belt within the next two years.