Past performance does not predict future returns. You may get back less than you originally invested. Reference to specific securities is not intended as a recommendation to purchase or sell any investment.

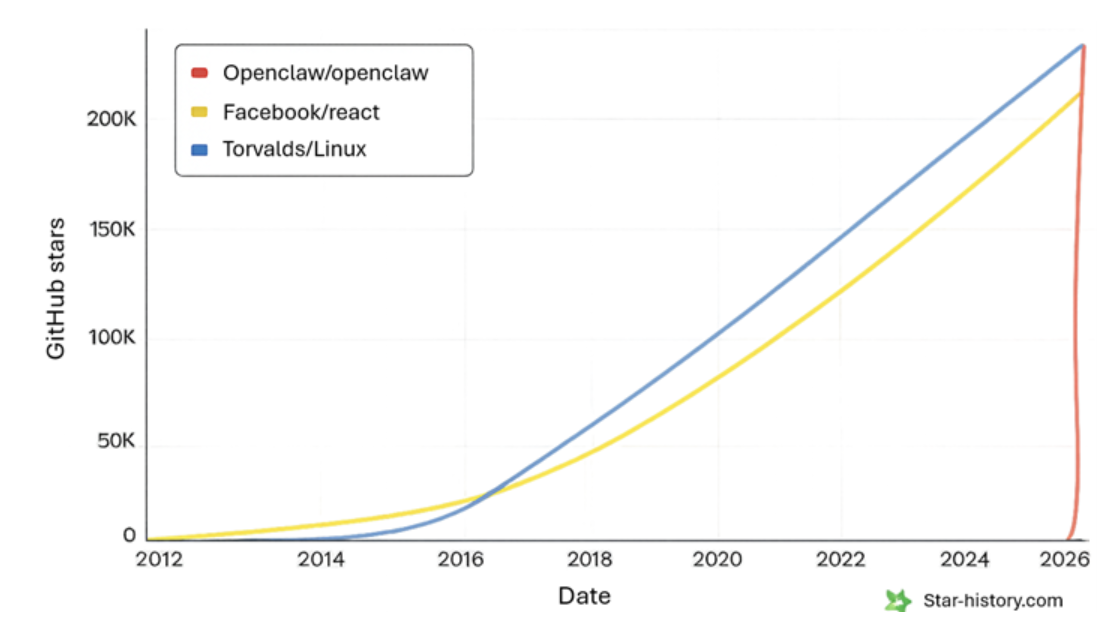

The strategic importance of Claude Cowork, Claude Code, OpenAI Codex and Palantir AIP isn't that they're "better copilots", it's that they reveal a new mode of software creation and enterprise penetration emerging simultaneously. Small teams now ship useful products in radically compressed timelines, and agents themselves are part of the build process. Peter Steinberger's OpenClaw is a striking example: a small open-source agent project became viral at a rate akin to GPT-3 and has reshaped the entire AI industry – one product created by one person that has introduced agential AI to the masses. Cowork was built in two weeks by itself with no humans in the loop. The same agentic systems that automate work are now accelerating the creation of the next generation of agentic products.

Inference inflection arrives

Source: Nvidia company earnings release, Q1 2026

That creates a recursive loop. Agents help build better agents; better agents automate more workflows; those workflows become wedges into the enterprise; usage and context improve the next product. This is the classic disruptor playbook, but faster than traditional SaaS. The product doesn't need to replace Salesforce, ServiceNow, GitHub or SAP on day one. It lands inside one painful workflow, proves productivity, absorbs context, and expands until the agent becomes the primary interface through which work is executed. The incumbent is demoted from workflow owner to system of record.

To cut through the noise, the evidence to watch for is accelerating top-line growth as these products scale across the economy, and an equally telling absence of it where incumbents are getting hollowed out. The clearest single datapoint is Anthropic eating Microsoft alive in real time. Microsoft's Consumer Microsoft 365 business; two decades of investment, hundreds of millions of paying users, the default productivity suite for the modern white-collar workforce generates roughly $7.5 billion in consumer annual revenue. Anthropic, four years old, has scaled from ~$1 billion annual recurring revenue at the end of 2024 to a reported ~$40 billion run-rate by April 2026 as Claude Code, Cowork and enterprise API usage compound. The most valuable consumer software franchise of the previous era is being lapped more than five times over by a single AI-native challenger, in a fraction of the time.

From applications to objectives

The old model: a human opens software, decides what to do, performs a sequence of actions, updates the system. The agentic model: the user states an objective, the agent gathers context, acts across tools, asks for approval when required, and updates the relevant systems automatically. The scarce asset shifts from the database to the execution layer.

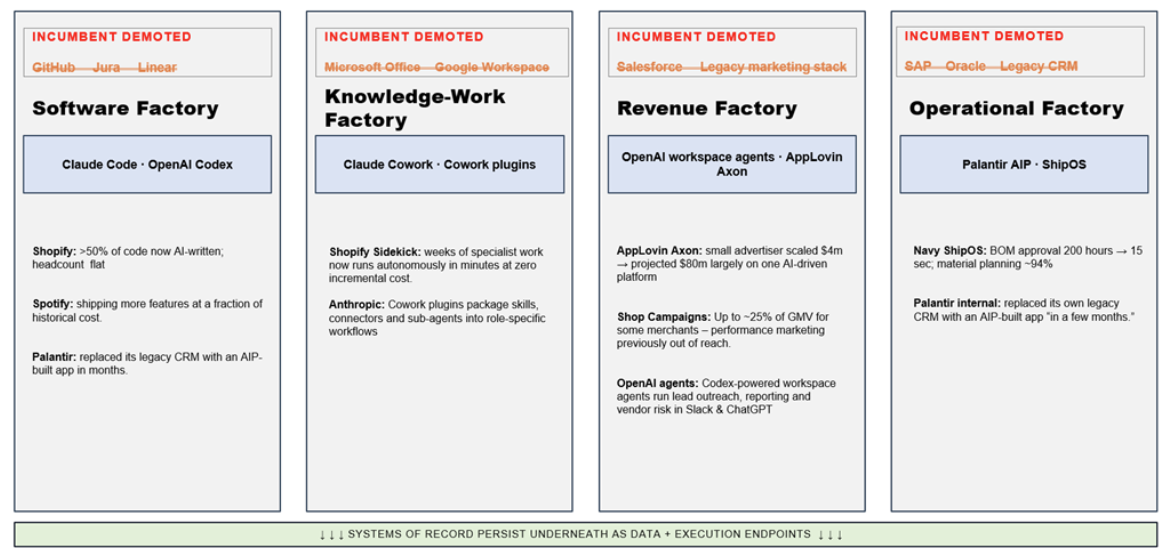

The agentic wedge — four attack surfaces

Each agentic product lands in one painful workflow, proves productivity, absorbs context, then expands. The incumbent gets demoted from workflow owner to system of record.

Source: Liontrust – Agentic AI: the new enterprise wedge

The first land motion is narrow by design. Claude Code lands with developers because coding is high-frequency, high-friction and measurable. Cowork takes that pattern into knowledge work: messy folders, PDFs, spreadsheets, emails. Palantir AIP attacks high-stakes operational workflows. The wedge isn't "transform the enterprise"; it's "fix this bug," "draft this memo," "approve this bill of materials."

The productivity proof points are no longer speculative. Palantir's ShipOS, deployed with the US Navy, dropped manufacturing bill of materials approval time from 200 hours to 15 seconds and reduced monthly material planning time by 94%. AppLovin's Axon platform is doing the same thing on the demand side of digital advertising — its CEO Adam Foroughi described AI-generated video ads as "really, really tough to tell that they're built by AI instead of a human being, and the cost is exceptionally low relative to what a human-generated video would cost," and laid out a system "where an advertiser can onboard, generate high-performing ads, and scale campaigns profitably without ever needing to talk to a human."

The hollowing-out, not replacement

The first sale is productivity. The second is context. Once an agent proves useful, it connects to more systems: GitHub, Slack, Microsoft 365, Jira, CRM, ERP, data warehouses. It stops being a point tool and becomes a work graph. Code is especially strategic: it's the hidden operating system of the modern enterprise. An agent that understands the codebase, APIs, deployment logic and internal tooling has a path into the company's operating model.

Palantir is already living this thesis internally. As Shyam Sankar described on the Q1 2026 call: "This is also why we are seeing the death of legacy software. AIP replaces static workflows not by replicating the playbook, but by eliminating the need for one… This quarter, we replaced our old expensive CRM with an AI-first solution built on AIP in a few months that users absolutely love." The signal matters because it shows the disruptor consuming its own dog food: an AI-native platform displacing a category-defining SaaS incumbent inside a public company's own four walls.

Shopify shows what land-and-expand looks like once the AI surface starts producing economic outcomes. Harley Finkelstein described how Shop Campaigns has changed the economics of customer acquisition for small merchants: "For some of those smaller merchants, Shop Campaigns is contributing as much as a quarter of their total gross merchandise value. That is not a nice-to-have. That is a growth engine. Shopify is giving them economies of scale that were previously only available to the largest brands." This is the agentic wedge in motion; a small initial integration becomes a meaningful share of a customer's revenue, which deepens dependency and expands the budget pool available to the platform.

Palantir's most striking customer example reframes the question agentic AI is actually asking. As Shyam Sankar put it: "A major telco set out to automate 10 million customer calls a year. The real insight was that the most dissatisfied customers never call. They churn silently. The reframe was counterintuitive. Don't use AI to reduce calls, use it to generate them, an AI advocate that proactively calls on every customer's behalf." The point generalises: the strongest agentic deployments aren't faster versions of existing workflows. They are workflows that weren't economically feasible before and they expand the addressable budget rather than cannibalise it. The incumbent risk is therefore not immediate replacement but hollowing-out. Salesforce still holds customer data, but the agent prepares the account plan, drafts the outreach, updates the opportunity.

The budget pool and the cost structure

Traditional SaaS sold seats. Agentic AI sells work completed, time saved, throughput increased, revenue generated. The addressable budget isn't only software spend, it's labour, outsourcing, BPO, offshore development, QA, support, analytics and internal tooling.

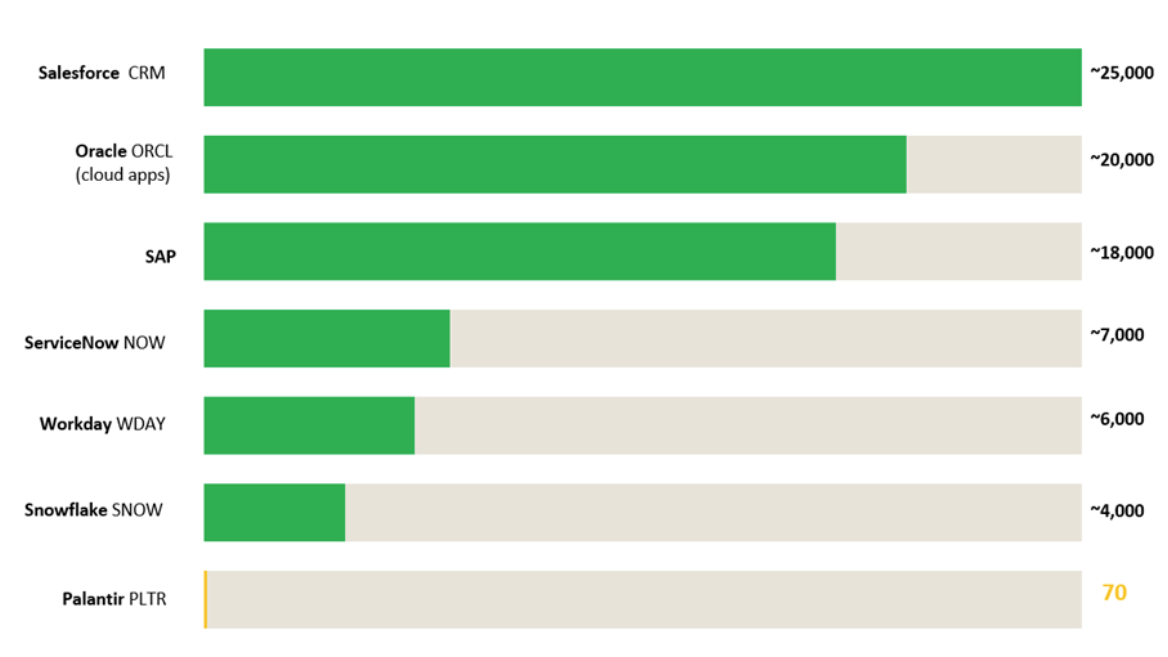

The most provocative version of this comes from Palantir itself. Alex Karp described the company's go-to-market as a near-elimination of traditional enterprise sales headcount: "We have 70 salespeople, a normal company of our size would have 7,000. Only seven of our salespeople actually even really sell. We are doing what a normal company would do with 7,000 salespeople with seven people. We're doubling the US." He doubled down on the cash-flow consequence: "Our free cash flow this quarter is larger than our revenue a year ago in the same quarter." If a 70-person sales motion can deliver triple-digit US growth and >100% organic acceleration, the cost structure of category-leading SaaS — quota-carrying reps, layered SEs, channel margin — is suddenly on the table for re-pricing.

The cost-structure reset

Approximate global sales & marketing headcount. Palantir is running a $7bn+ run-rate business with a sales motion roughly two orders of magnitude smaller than category-leading SaaS.

Source: Liontrust, Incumbent S&M headcount is approximate, based on publicly disclosed company filings and industry estimates. Palantir figure is Karp’s own quoted number on the Q1 2026 call. Visual ratio is illustrative — Palantir bar shown at minimum visible width for legibility.

“We have 70 salespeople. A normal company of our size would have 7,000. Only seven of our salespeople actually even really sell… Our free cash flow this quarter is larger than our revenue a year ago in the same quarter.” — Alex Karp, Palantir Q1 2026 earnings call

The vendors are not just selling that re-pricing to customers; they're realising it internally. Shopify's Harley Finkelstein put the productivity shift bluntly: "AI right now writes well over 50% of our code today, and that number is going up significantly, not down." Spotify's Gustav Soderstrom described an analogous internal step-change: "We're integrating AI across every part of Spotify, accelerating how we build and deliver at a pace we haven't seen before. We're shipping more, faster, and with greater efficiency, lowering the cost per feature while increasing the impact."

AppLovin is generating $1.56 billion of quarterly adjusted EBITDA at an 85% margin while holding the line on headcount — the operating leverage of an AI-native business model rather than a software company bolting AI on top. Customer-side transformation runs along the same axis. Shopify Sidekick collapses work that "a few months ago… [required] multiple specialists, marketing, UX design, copywriting, and often an incremental cost to the merchant and likely several weeks from start to finish. And now it is happening autonomously in minutes at zero incremental cost."

Three compounding loops

The strongest agentic platforms compound through three loops. Context accumulation: the more the agent sees, the more useful it becomes. ServiceNow has trained on "over 95 billion annual workflows and more than 7 trillion transactions," and McDermott reduces the difference between ServiceNow AI and foundation models "to one word, context." Execution learning: every repeated workflow becomes a reusable skill, plugin or template — Anthropic's Cowork plugins and AIP's ontology both follow this pattern. Governance capture: once agents touch real systems, the enterprise needs permissions, audit trails and approval flows. The vendor that governs the human-agent workforce becomes much harder to displace.

The vendors are pursuing distinct edges. Palantir is furthest along on operational governance; AIP is described as a "tool factory" for humans and agents sitting on top of the enterprise's digital twin, and its lean go-to-market shows what the operating model of an agent-native enterprise software company can look like. OpenAI's advantage is distribution: Codex into developer workflows, workspace agents into ChatGPT and Slack for repeatable team processes. Anthropic's advantage is agentic depth and workflow design. Claude Code in the software factory, Cowork plugins packaged around real jobs from finance to legal to operations.

The endgame

Not every incumbent disappears. The more likely outcome is a re-ranking of enterprise value. Systems of record persist, but systems of action capture the margin. The vendor that owns the execution interface owns the user relationship; the user relationship captures the workflow; the workflow earns the right to expand into adjacent budgets. Budget migrates from passive software toward the layer that produces outcomes, and the vendors that sell those outcomes will look structurally different from the SaaS incumbents they're displacing, with smaller sales forces, leaner engineering orgs, and pricing tied to work done rather than seats issued.

Agentic AI products are not features. They are beachheads. Claude Code and Codex attack the software factory. Claude Cowork attacks the knowledge-work factory. OpenAI workspace agents attack repeatable team workflows. Palantir AIP attacks the operational factory. Each starts as a productivity tool. The strategic ambition is platform control – incumbents beware you can no longer fake it until you make it.

Read, watch and listen to more insights from Liontrust fund managers here >

KEY RISKS

Past performance does not predict future returns. You may get back less than you originally invested.

We recommend this fund is held long term (minimum period of 5 years). We recommend that you hold this fund as part of a diversified portfolio of investments.

The Funds managed by the Global Innovation team:

-

May consider environmental, social and governance ("ESG") characteristics of issuers when selecting investments for the Funds.

-

May hold overseas investments that may carry a higher currency risk. They are valued by reference to their local currency which may move up or down when compared to the currency of a Fund.

-

May have a concentrated portfolio, i.e. hold a limited number of investments or have significant sector or factor exposures. If one of these investments or sectors / factors fall in value this can have a greater impact on the Fund's value than if it held a larger number of investments across a more diversified portfolio.

-

May encounter liquidity constraints from time to time. The spread between the price you buy and sell shares will reflect the less liquid nature of the underlying holdings.

-

Do not guarantee a level of income.

The risks detailed above are reflective of the full range of Funds managed by the Global Innovation team and not all of the risks listed are applicable to each individual Fund. For the risks associated with an individual Fund, please refer to its Key Investor Information Document (KIID)/PRIIP KID.

The issue of units/shares in Liontrust Funds may be subject to an initial charge, which will have an impact on the realisable value of the investment, particularly in the short term. Investments should always be considered as long term.

DISCLAIMER

This material is issued by Liontrust Investment Partners LLP (2 Savoy Court, London WC2R 0EZ), authorised and regulated in the UK by the Financial Conduct Authority (FRN 518552) to undertake regulated investment business.

It should not be construed as advice for investment in any product or security mentioned, an offer to buy or sell units/shares of Funds mentioned, or a solicitation to purchase securities in any company or investment product. Examples of stocks are provided for general information only to demonstrate our investment philosophy. The investment being promoted is for units in a fund, not directly in the underlying assets.

This information and analysis is believed to be accurate at the time of publication, but is subject to change without notice. Whilst care has been taken in compiling the content, no representation or warranty is given, whether express or implied, by Liontrust as to its accuracy or completeness, including for external sources (which may have been used) which have not been verified.

This is a marketing communication. Before making an investment, you should read the relevant Prospectus and the Key Investor Information Document (KIID) and/or PRIIP/KID, which provide full product details including investment charges and risks. These documents can be obtained, free of charge, from www.liontrust.com or direct from Liontrust. If you are not a professional investor please consult a regulated financial adviser regarding the suitability of such an investment for you and your personal circumstances.

Understand common financial words and terms See our glossary