The worst is over. No, I am not claiming that stocks and bonds are going to rebound and that the troubles of the global economy are at an end. This week we officially passed ‘Blue Monday’, the day when things are allegedly at their bleakest.

It is named because the weather is at its coldest, the days are their shortest and the Christmas break is firmly in the rear-view mirror, meaning this time of year can be particularly hard.

Throw in a cost-of-living crisis in 2023 and it is fair to say that the shade of blue this week was much darker than usual.

Economic news in the UK painted a mixed picture. Today, consumer spending figures showed that we are now starting to meaningfully tighten our purse strings, with retail sales down 1% over the Christmas period.

There was some respite however, as inflation dropped for the second month in a row, with some analysts suggesting that it could encourage the Bank of England to slow down its pace of rate rises and end its tightening programme much earlier than expected.

Of course there were disagreements, with other commentators suggesting these figures meant nothing and that people should continue to plan for the path the Bank is currently on. Only hindsight will give us the answer.

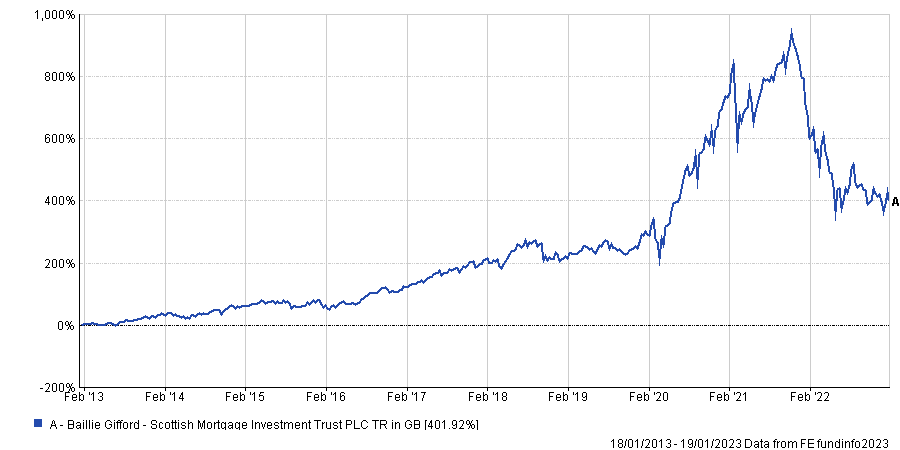

Away from economics, one noteworthy event was that Investec analysts downgraded the once-mighty Scottish Mortgage investment trust to a ‘sell’.

For context, the trust was the best performer in the IT Global sector for many years post the financial crisis and still holds the title of the highest-returning trust over five and 10 years.

But recent performance has been poor. Over 12 months the trust is down a third, while it has more than halved since its peak in November 2021.

Total return of fund vs sector and benchmark over 10yrs

Source: FE Analytics

Analysts Alan Brierley and Ben Newell said this week that they believe there is still more pain to come (so much for my opening line), with three main causes for concern.

First is the ramp-up of gearing, which has increased from less than 10% to 17% today. “We struggle to reconcile this sudden appetite for gearing. Given the extremely high-beta characteristics of the listed equity portfolio, and significant exposure to private investments, the risks are clear,” they said.

Second is the expectation for a late-stage venture capital reset, with a “value lag” for private companies (the difference between the price today and the last time it was valued), suggesting there could be further pain when these companies are re-rated.

A recent fall in its listed equity portfolio means that the trust now has around 35.9% of assets in private businesses, above the 30% self-imposed limit given to the managers.

Third, the analysts suggested that the unsupportive backdrop for the growth style of investment will continue, with more rate rises and quantitative tightening.

While the trust is supposed to be a long-term investment and is clear about how it allocates capital, the analysts said it was “vulnerable to a sharp correction”.

Perhaps there will be a “much more attractive entry point” in the next few months, they admitted. Still, for now, the trust seemingly is a high-risk proposition with the potential for further pain.