A year ago the Labour Party won a historic majority and swept into power with a mandate for a new direction. The promise was to unlock growth and productivity whilst being good custodians of the nation’s moral and financial reputation.

It would be easy to go through the list of key election pledges and assess how far along the road they are to delivering on them. We could talk about policy errors and U-turns, in particular Pensioner Winter Fuel allowances. But in reality, these are symptoms and not the key theme running through the first year of this government.

And, yes it’s the same theme we have had since 2009 and one which has become acutely amplified since the Covid crisis. How does a government spend on its political priorities when, to quote Labour’s Liam Byrne in 2010, when leaving a note for his Conservative successor: “I am afraid there is no money”.

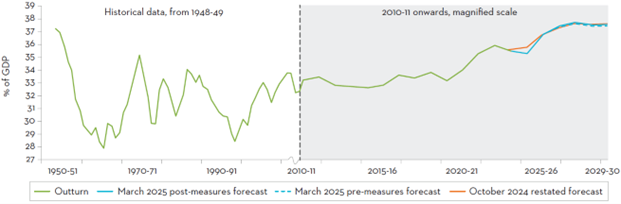

National Accounts axes as a share of GDP

Note: The October 2024 forecast as a share of GDP has been restated to account for revised nominal GDP data in the 2024 Professional Pensions Blue Book.

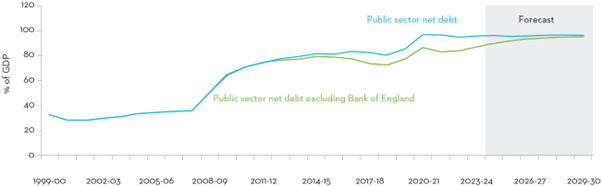

UK debt to GDP

Things were tight in 2010, as the dust settled from the 2008 global financial crisis (GFC) when debt to GDP was around 65% and interest rates were 1%. A decade later after government spending on the Covid crisis, it is now 95% (debt to GDP) with rates at 4.25%; the situation is almost unbearable.

With a natural instinct to boost government spending on health, education and welfare and a need to spend on defence, where is the money coming from?

The first Budget from chancellor Rachel Reeves did some sensible accounting by moving capital expenditure off the debt/GDP target. This has resulted in a series of long-term spending plans being developed for housing, ports, energy and infrastructure. These are hugely significant in re-wiring and re-igniting the UK economy and the focus is right:

- Driving an energy policy to create a sustainable industry with a competitive advantage and enhance investment in artificial intelligence (AI).

- De-bottleneck the roads and the railways, uncork the planning system to allow homes to be built where the jobs are for the c.70m population.

- Ensure that the UK defence industry has the investments and skills as well as the orders to thrive as defence spending rises from 2.5% to 3.5% and then 5% of GDP.

These are important initiatives: long-term investments to allow the UK to raise productivity and attract new investment and growth. But such plans are slow to mature, they do little to improve growth now but much to improve it after 2030.

But what about day-to-day spending? Fuel allowances, pensions, disability allowances, the NHS, schools, the list goes on.

And there are powerful forces telling you, you can’t do it all: Firstly, as Liz Truss found out, there is the bond market. Secondly there are the economic experts deep in government, often labelled as ‘Treasury Orthodoxy’, backing up the bond market. Lastly, there is the Monetary Policy Committee (MPC), whose only worry is inflation, which in the long term must be at 2% and their mandate is to settle the nerves of the bond market.

When the MPC was set up under Gordon Brown in 1997, it was a mistake not to give it a dual mandate, inflation and growth, as you see in the US with the Federal Reserve. In 2021 the then-chancellor, Rishi Sunak, tried to give it a secondary growth mandate but somehow it has slipped off the table. It seems to solely focus on inflation and having missed the signals on the way up in 2022, the MPC now sees inflationary dangers lurking inside almost every data point they can find and rates are very slow to fall.

As a government you need growth, to generate income, to fund promises. Growth rates since 2008 have been around half of the long-term trend and the forecasts for 2025 and 2026 show a continued global growth slowdown. The only hope is that as growth slows and even stops entirely in the next 12 months, is that inflation subsides sharply and it allows the MPC to cut rates. The cuts to rates will have to be similar to what the European Central Bank (ECB) has done, eight cuts and counting, and that gilts follow those rates lower.

If the government are tough on the current spending round – and it’s not started well with the U-turns over winter fuel, Universal Credit and Personal Independence Payments (PIP) – then it’s just possible that if the economy flatlines over the next two to four quarters, with weak oil prices and a strong sterling, these rate cuts could ride to the rescue.

This is the great contradiction that all investors remember, especially the bond market, where bad news suddenly becomes the good news. But in the wait for the rate cuts, the political pressure will rise sharply. Could they, would they hold their spending nerve? Not only does Reeves need to be the lucky chancellor, she needs to ensure that the bond market thinks she has the steel to restrict spending.

Effectively you are left thinking that the economic reality has made the promises of the last election un-obtainable. Unless you can find a new source of tax revenue, which is exactly as US president Donald Trump is trying to do via tariffs. They have tried raising taxes on school fees, pensioners, non-doms and employers, all with less success than they forecasted. Would they raise income tax or even capital gains/wealth tax? What would be the consequences? The risk today is that the government gets caught in an economic doom loop of lower growth, needing more taxes to avoid bond market jitters about government promises and spending, which again prompts lower growth.

The Labour party are caught in an economic bind that would have ensnared any party coming to power. But they did know that. The real question is can they find a way out of it? Find an economic path that gives them just enough room to effect their political choices? Or will they get lucky as weak global growth gives them an interest rate break? At present, caught in a mess they didn’t make, they are making it worse by trying to muddle through.

That will, of course lead them to lose the next election (after all only 20% of adults in the UK voted for them in 2024) and, if the polls are right, usher in Nigel Farage’s Reform Party into power. And that is why the UK’s gilts carry such a premium to their G7 neighbours.

Michael Browne is global investment strategist at Franklin Templeton Institute. The views expressed above should not be taken as investment advice.