India has been the darling of the emerging markets in recent years, but poor performance in 2025 has continued into 2026, leaving many questions for investors to answer before backing the Asian powerhouse.

One investor who has retreated from the country somewhat for now is Carmignac’s Naomi Waistell, who said her decade-long positive stance on Indian equities started to wane in 2025.

The co-manager of the FP Carmignac Emerging Markets fund said there are still “a lot of fundamental things to like about India”, but warned there are “two things that they don't have in their favour”.

Firstly, she is concerned by the “demographic dividend”, an economic term that describes when there is a vast number of working-age people compared with those of non-working age (children and the elderly). It implies that economic growth should build as there are more workers adding to productivity.

However, Waistell noted that the country must take advantage of this phenomenon while it lasts, with questions over whether there are enough jobs for the number of potential workers.

“How are they going to utilise those people? How are they going to make them productive and create enough wealth for that large society they have? So that’s one question mark – and the jury’s out on that,” she said.

The other factor that has given her pause is the manufacturing base in India moving up the value chain.

“Despite having a big policy push a few years ago on ‘Make in India’, it hasn’t really seen its share of global manufacturing move up,” she said.

This is in spite of the ‘China-plus-one’ narrative, where countries have looked to de-risk supply chains in the aftermath of the Covid pandemic by broadening out their manufacturing hubs to different countries.

“That has gone to ASEAN, it's gone to Mexico – and India hasn't really been able to move up the value chain. That's down to the fact that India spends a very, very small proportion of its GDP on R&D [research and development],” she said.

This has led to a slightly underweight position to India in the FP Carmignac Emerging Markets fund, although she said it may not be a position the fund holds for long.

“Coming into the second half of the year, there might be a moment where that changes and we want to reposition the fund if things progress well in India, but we'll have to see how that goes,” she said.

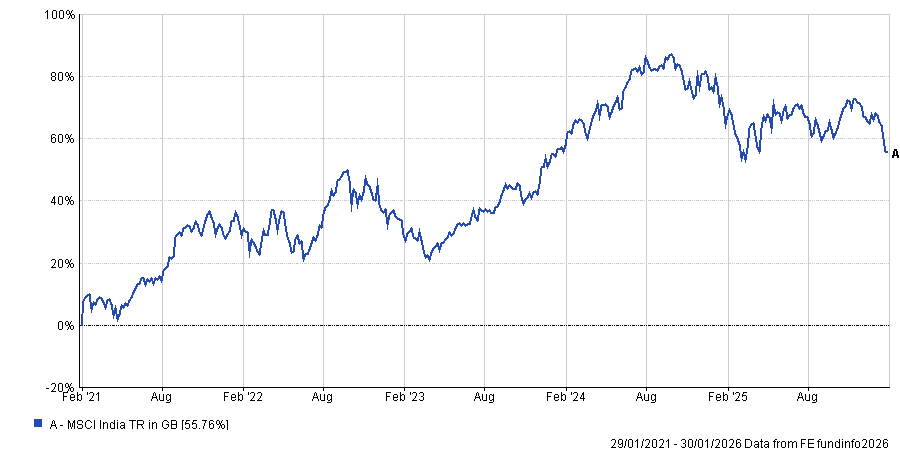

There is much that needs to go right first, however. Firstly, share prices would need to fall further. The market has been one of the standout performers over the past few years, with Indian equities making double-digit gains in four of the five years between 2020 and 2024, with 2022 the only exception.

Performance of index over 5yrs

Source: FE Analytics

What was once the “darling” of the emerging markets took a hard about-turn last year, with Indian equities losing 4.5%. And things have got even worse in 2026, with the MSCI India index down a further 7% already.

There are myriad reasons behind the market’s sudden fall from grace. The lack of a trade deal with the US has “weighed on India” and continues to have a negative effect, with the uncertainty putting off investors.

Indeed, foreign money came out of the country in its droves last year, although she noted that domestic institutions and retail investors have continued to put money in, which is a net long-term benefit.

On the economic front, low inflation meant nominal growth was less than double‑digits for the first time “in quite a little while”, while companies’ earnings growth was lower than it has been historically.

“That's really what has always been at the forefront of the argument: that India's premium is due to higher earnings growth, higher real growth, huge population, the demographic [dividend] and productivity. I don't think any of those fundamentals have gone away, but it has had a slower year.”

This combination has left India with a “valuation problem”, as its high premiums were not backed up by the economic data last year. A reversal of this in 2026 (either through lower starting prices or better growth figures) could play a part in the FP Carmignac Emerging Markets fund moving from its current underweight position.

Another aspect that needs addressing is the country’s perception when it comes to artificial intelligence (AI). While some view it as the premier anti-AI market, Waistell pushed back on this narrative, which she blamed for some of the recent performance.

However, multinational companies are implementing AI and, rather than AI taking jobs, people who do not use the new technology are being replaced by those who can use it.

“India has the second-highest AI penetration rate after the US. And if you weight the female users as well as male users, India comes out on top. This is misunderstood, but it's not really necessarily right now the most obvious thing to invest in, because it's not like a company is innovating,” she said.

“It's not the one who is leading the technology or doing heavy R&D but it's right at the forefront of creating productivity gains and using it in a real way for commercialisation.”

Market perception on the country is “fickle” but, if investors begin to appreciate the country’s use of AI, it could shift the narrative and draw investors’ eyes.

A potential third prong to give Indian equities a leg up would be structural reform. The country undertook a huge policy shift in 2017 with the goods & services tax (GST), which was implemented to replace a raft of other taxes, such as VAT, and bring more money into circulation from the black market.

“We've actually had a bit of a lull in structural reforms coming out of India. When [prime minister Narendra] Modi came to power in 2014, there was a huge wave of structural reforms,” she said.

“That has been digested. To get the performance of the Indian market going again, I think we need to see this next round of structural reform.”