Bonds have been back in favour over the past few years as rising interest rates have pushed yields higher, giving fixed-income investors better long-term return prospects than they have had for much of the past decade.

This rise in popularity has brought about the return of the 60/40 portfolio, which incorporates a 60% weighting to equities and a 40% position in bonds.

Yet Credo Dynamic has a positioning far more akin to those popular in the 2010s during the era of lower interest rates, with just 23% in bonds and a 22.8% position in alternatives.

Alternatives rose to prominence during the post-financial crisis era as interest rates were on the floor and investors in search of reliable income turned to other assets such as property, infrastructure and private credit to achieve meaningful returns.

In recent years, with developed market base rates around the world climbing to 5% or higher, bonds (and particularly government bonds) have become far more appealing.

FE fundinfo Alpha Manager Rupert Silver noted that his Credo Dynamic fund had as much as 45% in fixed income at its peak, which coincided with the Liz Truss mini-Budget, but said he is “not particularly impressed with corporate bonds or gilts” right now.

“Things change quickly”, he added.

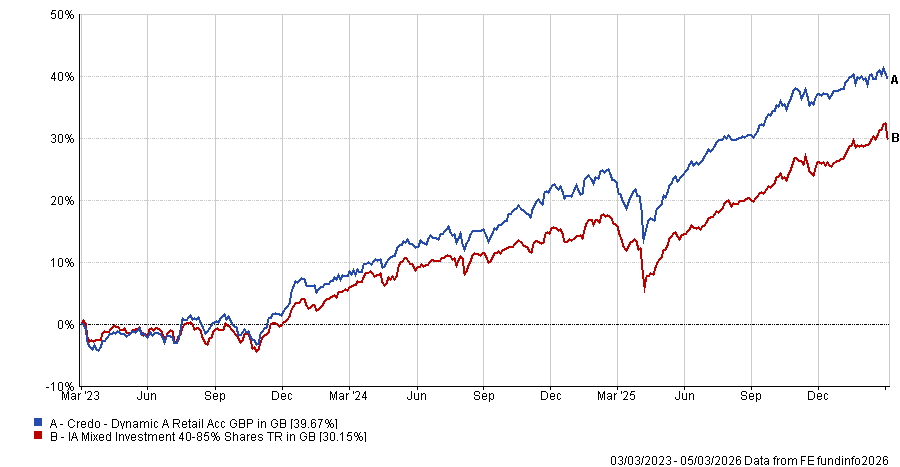

These changes have contributed meaningfully to returns, with the £114m fund a top-quartile performer in the IA Mixed Investment 40-85% Shares sector over the past three and five years, while also beating its average peer over 12 months.

The fund has sat in the top 25% of its peer group in each of the past three calendar years, with recent Trustnet research showing it has ticked (just about) all the boxes for investors in recent years.

Performance of fund vs sector over 3yrs

Source: FE Analytics

Within bonds, his typical preference is investment-grade credit, where investors can get “significantly higher returns” for taking “a fraction more risk”.

However, today spreads are “the tightest they’ve ever been”, meaning there is very little compensation for credit risk. As a result, co-manager Ben Newton noted the fund is largely weighted to short-dated government bonds, with maturities of less than three years.

“In corporate bonds, we don’t see the value because of the spreads and with gilts, we want to go quite short, which makes it more cash‑plus. As a result, we want to achieve an attractive return somewhere else,” he said.

But the return to alternatives is not just due to a dearth of options in the fixed-income space, they said, noting that there are some “super exciting” opportunities among alternative assets.

Silver noted: “We think we can get much higher returns over the long term in alternatives and hold assets in the portfolio that have near‑zero correlation to equities.”

The fund is allocated to commodities, which surged in 2025. The bucket was led higher by gold and other precious metals, which boomed as investors turned to safe havens amid geopolitical concerns.

More recently, oil has spiked following the start of military action in Iran by the US and Israel last week, which has given the broad commodity sector another leg higher.

Another sleeve that has performed well for the trust is real estate investment trusts (REITS), where there was a “big wave of takeovers”. Newton said: “Last year was an outstanding year for the alternatives section, particularly within commodities and REITs.”

The managers also venture into investment trusts for more traditional equity portfolios – not just for real estate and other alternative assets. For example, the Merchants Trust is a 1.6% position in the Credo Dynamic fund.

Here, they argued that the rationale is centred on valuation. Although the discount “wasn’t super exciting”, they bought the trust on a 6-7% discount to net asset value (NAV), which is “boring in a sense when compared to some of the quirky 20% ones”.

However, the long-term track record of the trust (it has beaten the FTSE All Share over the past decade) and the discount on offer made it a “lovely way” to access UK equities at a time when the managers were “running away from US large-cap equities” on valuation grounds.

They argued that, should UK equities continue to outperform the US (as they did in 2025) and the trust continue to beat the FTSE All Share benchmark, this discount could close.

For much of the three years prior to 2024, the trust traded on a premium, with Silver suggesting the discount could come in by between 2% and 4%, bringing it closer to par, or “maybe more” if it were to return to its pre-2024 levels.