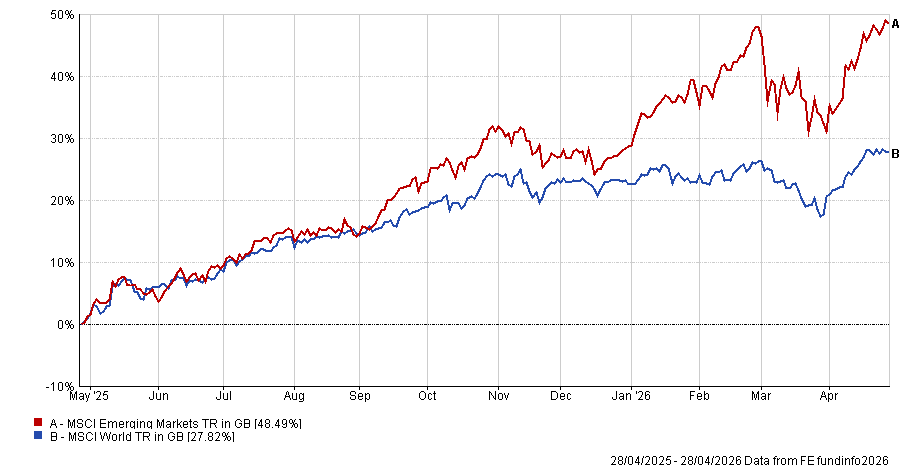

Emerging markets are up almost 50% over 12 months, trouncing the returns from their developed market peers. Yet investors harbour many historic prejudices that may be stopping them from acknowledging the opportunity available, according to Baillie Gifford’s Ben Durrant.

The manager of the Baillie Gifford Emerging Markets Growth fund said there is a huge gap between the perception of emerging markets and the reality.

“Externally, emerging markets are still seen as dangerous places to invest, but when we look at the companies themselves and the financial performance, it’s starting to look reckless not to have exposure to emerging markets,” he said.

Performance of indices over 12 months

Source: FE Analytics

Much of investors’ hesitancy has centred around three main arguments. The first is that investors do not want to be early, as they have had poor experiences in the past. However, Durrant argued recent returns suggest that the “behavioural hurdle” should be easier to overcome.

The second is concern over China, where “fear, uncertainty and a lack of understanding have driven misperceptions”.

While the country has historically delivered strong GDP growth, equity returns have failed to match this. Part of this is because companies competed aggressively to lower prices – benefiting consumers but not shareholders. The other reason was that households chose to build wealth through property rather than markets.

“With the property market under pressure, the government needs to create new outlets for savings, which means reforming the equity market,” said Durrant, who noted that the stock market is “being repositioned as a place for long‑term returns rather than speculative trading”, with improving corporate quality and shareholder returns.

The third part has been that there has been no need to invest in emerging markets as investors have been able to make strong gains from developed countries, primarily the US.

“The US was the best place to get exposure to the world’s leading software companies. Investors paid handsomely for that – for every unit of GDP growth the US delivered, you got roughly three units in stock‑market returns. Low interest rates helped that dynamic as well,” said Durrant, highlighting that this was the opposite of what occurred in China.

“The other factor was that the US was a simple, safe place to invest. It was the global political and economic hegemon, the dollar was king and you were paid well to be there.”

However, “everything is changing” now, with the world entering a “multipolar” period where there is no clear winner and investing will become more complicated.

“Complexity favours diversification – and that favours emerging markets,” said Durrant, who noted that emerging markets account for roughly 40% of global GDP but just 10% of global equity indices.

Where are the opportunities?

Durrant, like almost all Baillie Gifford managers, invests with a long-term mindset by picking companies he believes can grow faster than the market. As a result, he said investors need to ask three key questions: what will matter over the next decade, who will solve the biggest problems and who will benefit?

Durrant said that if he polled investors, the answers would range but would likely include some variations of energy transition, artificial intelligence, and the source of future global growth.

“All of those are centred on emerging markets,” he said.

Taking the energy transition, he noted that the premise is in place for how it could work. The current issue, however, is a manufacturing challenge, something he described as a strength of emerging markets.

For example, the fund owns Zijin Mining, a company that has added more than double the copper production over the past five years of its Western rivals combined, said Durrant.

“You then have companies like CATL, which, as a single company, makes more than a third of the world’s batteries. If you want a decarbonised economy, you need to rely on emerging markets,” he said.

Turning to AI, while much of the euphoria has centred around US businesses such as Anthropic and OpenAI, emerging markets are where the hardware producers that enable the technology are housed.

“Companies like SK Hynix, which produces the majority of global high‑bandwidth memory,” he said. “Around 80% of the memory that sits on or next to an Nvidia chip comes from South Korea. Yet SK Hynix trades at under 4x earnings as people don’t appreciate the growth.”

Lastly, on global growth, he said that consumption still matters and consumers still have a big role to play in the global economy. Again, this is where “emerging markets dominate” with a broadly increasing middle class.

Examples of ways to invest in this are MercadoLibre in Latin America and SEA in Southeast Asia, which process more daily transactions outside the US than Amazon, but are valued at roughly one-tenth of the US giant’s market capitalisation, he said.

“When we look across the range of aspects that matter for the future – energy, intelligence and growth – they all seem to focus on emerging markets. There are great companies across the world and you can pick out pockets, but the crux of what matters for the future is enabled by or inside emerging markets,” he said.

“That doesn’t feel fully acknowledged at this point in time.”