Several venture capital trust (VCT) fundraising offers are at risk of closing early before the end of the tax year as investors rush to secure 30% upfront income tax relief before it falls to 20% on 6 April 2026.

These vehicles raise capital periodically by issuing new shares through fundraising rounds, which typically remain open until a target amount is reached or a deadline passes. When demand is high, popular offers can close well before their scheduled end date.

VCTs offer up to 30% upfront income tax relief on investments up to £200,000 per year, tax-free dividends and an exemption from capital gains tax on the shares. They invest in small, early-stage UK companies and are considered high-risk, but the tax incentives are designed to compensate for that risk. Shares must be held for at least five years to retain the relief.

Chancellor Rachel Reeves confirmed the cut to 20% relief in November's Budget, triggering a surge in demand from investors keen to lock in the higher rate while it lasts. Earlier today, the Unicorn AIM VCT announced that its current offer to raise £20m has been 90% subscribed and decided to utilise the overallotment facility and increase it by a further £15m in the largest fundraise in the company’s history.

The tax allowance reduction shifts the emphasis firmly onto manager quality, according to Peter Hicks, research analyst at Chelsea Financial Services. “With a smaller tax cushion, investors need proven exit discipline, sensible fee structures and genuine alignment of interests to drive returns,” he said.

As with all VCTs, investors should take a long-term view and not invest solely for the tax benefits. Against that backdrop, Hicks highlighted two below: Pembroke for alignment and shareholder-friendly charging and Gresham House for scale, momentum and track record.

Pembroke VCT

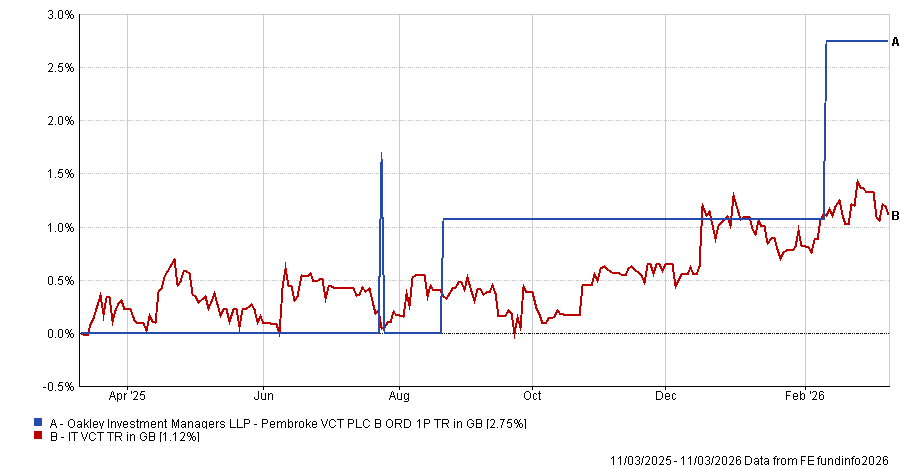

Launched in 2013, Pembroke has built assets under management to £260m and has consistently hit its 5% annual dividend target since 2021. Recent exits include a partial sale of experiential travel platform Secret Food Tours, generating a 5.3x return, and sustainable luxury womenswear brand ME+EM, which delivered a 16.2x return on its exit in 2022.

Hicks said the strongest argument for the VCT is the alignment of incentives with both investors and investee companies. Where possible, Pembroke commits capital alongside founders under the same investment terms. Crucially, the manager does not charge performance fees on unrealised valuation gains – fees are only earned when value is realised in cash.

“This is an excellent approach and one that should be commended more loudly,” Hicks said. “Pembroke's performance fee arrangements go against the grain of how most other VCTs structure their charges.”

Manager Andrew Wolfson is also “unapologetically pro-special dividend”, Hicks noted. When possible, the priority is to return capital to shareholders. “In tandem with the charging structure, this philosophy places shareholder outcomes front and centre, and is exactly what investors should demand as the tax tail becomes less generous.”

A quarter of Pembroke's portfolio companies are already profitable, with the largest holding, consumer health-tech business Lyma, recently gaining regulatory approval for use in the US. Performance over one year stands at 2.8%, with a five-year return of 13.5%. Over 10 years, the trust has delivered 49%, sitting in the middle of the VCT Generalist sector.

Performance of fund against index and sector over 1yr

Source: FE Analytics

Gresham House VCTs

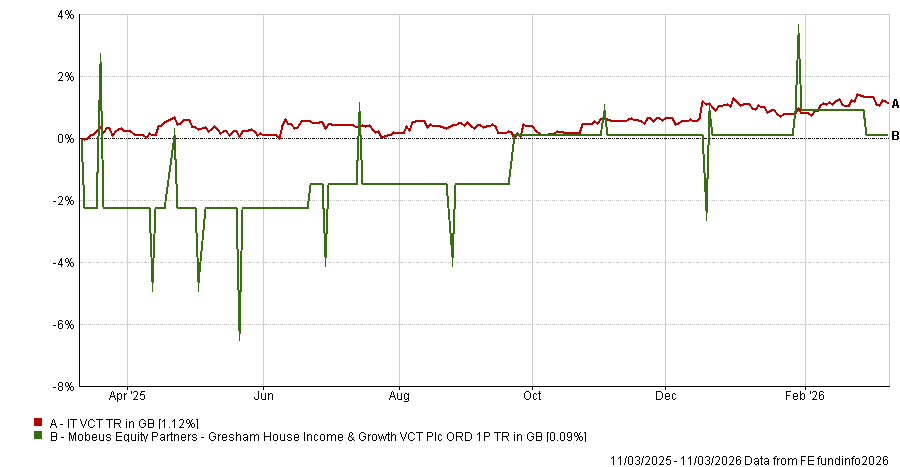

Formerly Mobeus, the Gresham House VCTs are among the most popular in the sector. Their £90m fundraise in September 2024 reached capacity in eight weeks, a reflection of the track record: Gresham House Income & Growth VCT 1 and 2 are the best performing in the AIC VCT sector over 10 years, delivering tax-free total returns of 136% and 162% respectively.

Since March 2022, the VCT has made six highly profitable exits, realising proceeds of £123m against a cost of £74m. “Achieving this against the harsh economic backdrop of recent years underlines the strength of the investment process,” Hicks said. Proceeds have supported a strong dividend track record that has frequently exceeded the new annual target of 7% of net asset value.

This year's raise was brought forward due to the upcoming reduction in income tax relief. Hicks said the decision was correct: when relief was last cut in 2006, VCT sales collapsed by 65%.

Gresham House Income & Growth VCT has returned just 0.1% over one year but 33.1% over five years and 130.5% over 10 years, placing it in the top quartile of the sector.

Performance of fund against index and sector over 1yr

Source: FE Analytics

Hicks acknowledged that some investors may question the trust's cash position, which stood at £73.76m (34.3% of net assets) as at 30 September 2025. However, he argued that this liquidity places the manager "in pole position to support existing winners and capitalise on new opportunities as competitors retrench".

The rule changes accompanying the relief reduction – which broaden the qualifying universe and allow for larger scale-up investments – are a key positive that should not be overlooked, he added.

“Whilst the more headline-grabbing reduction in income tax relief is disappointing, the underlying qualifying rules are constructive.”