The Iran crisis has exposed a fundamental misunderstanding of when bonds protect investors and when they do not, according to Luke Hickmore, investment director for fixed income at Aberdeen.

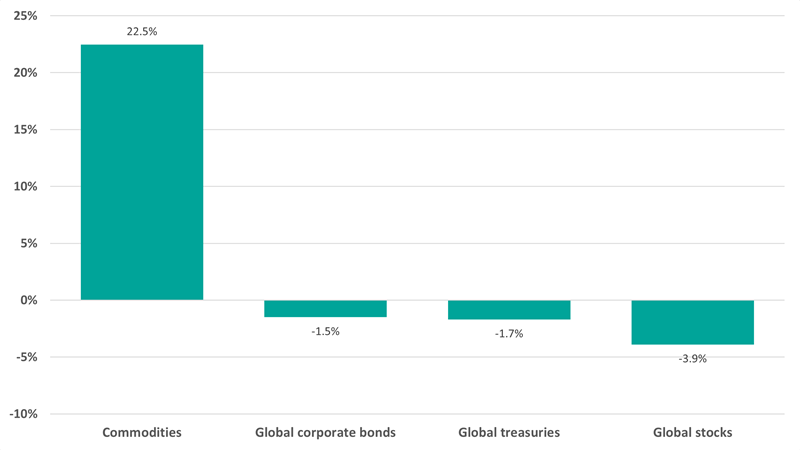

Since the US and Israel launched their attack on Iran on 28 February, the Bloomberg Global Treasury index has fallen 1.7% (in sterling terms) while the Bloomberg Global Aggregate Corporates is down 1.5%.

This is better than the 3.9% fall in the MSCI AC World over the same period but a worse outcome than some investors might have expected during a period of market stress, owing to the status of bonds as a perceived safe haven.

Performance of asset classes since Sat 28 Feb 2026

Source: FinXL. Total return in sterling between 28 Feb and 15 Mar 2026

Below, Hickmore explains what investors need to understand about bonds during a time of heightened geopolitical tension.

1. Why bonds have not behaved like a traditional safe haven

Brent crude rose from $73 per barrel on 27 February to over $100 by 8 March, briefly hitting $126 at its peak. The effective closure of the Strait of Hormuz, through which roughly 20% of global oil supply passes daily, drove the surge.

UK gilt yields climbed to a six-month high of 4.8%, while US 10-year Treasury yields rose to 4.21-4.27%. By historical convention, bond prices should have risen as investors moved into safe havens.

However, Hickmore said: “This time is different. The shock is coming through energy prices and inflation, not through a collapse in demand.”

In past geopolitical crises, investors rushed into government debt, driving prices up and yields down. The Iran crisis has done the opposite because the primary economic consequence is an inflation shock, not a demand shock.

Higher oil prices threaten to keep inflation elevated, which erodes the purchasing power of the fixed-income bonds' pay. Investors have responded accordingly.

“When inflation is the problem, bonds do not provide shelter,” Hickmore said.

2. What investors mean by a ‘premium’ and why they are rising

‘Premium’ is the extra return investors demand for taking on extra risk. When uncertainty rises, the price of lending money rises with it.

Hickmore identified three distinct premiums rising simultaneously in today’s bond market. There is a higher inflation premium (reflecting the risk that oil keeps inflation elevated), a higher term premium (for uncertainty about where interest rates ultimately settle) and a geopolitical risk premium layered on top of both.

Treasury inflation-protected securities’ breakeven rates, which measure market inflation expectations, are near one-year highs. The IMF has estimated that every 10% increase in energy prices in 2026 is expected to add roughly half a percentage point to global inflation.

“None of these premiums are visible on a single line of a spreadsheet. But together, they push yields higher,” the manager said.

3. Geopolitics and the return of the risk premium

Iran’s new supreme leader, Mojtaba Khamenei, has declared that the closure of the Strait of Hormuz will continue as a tool to pressure the enemy.

Around 200 vessels remain anchored outside the strait and shipping insurance rates have risen four to six times over in recent weeks. Qatar, which supplies 12-14% of Europe’s LNG, has warned it may declare force majeure on exports if the war continues.

Hickmore noted that conflict in an energy-producing region widens the range of possible outcomes. Supply disruptions, shipping bottlenecks and sudden price spikes all become more probable even if the worst outcomes are avoided and markets price that wider uncertainty.

“This is where the geopolitical risk premium comes in. Investors demand additional compensation for lending in a world where inflation shocks are more likely and policy responses are less predictable,” the manager explained.

“Crucially, this premium does not disappear just because markets have ‘calmed down’ for a few days. It stays in place as long as the underlying risks remain unresolved. That is why yields can stay elevated even in the absence of fresh bad news.”

4. Bond yields reflect uncomfortable truths

A Bank of England rate cut in March, which futures markets had considered near-certain after four cuts in 2025, is now in serious doubt. Fed rate cut expectations have been pushed out to September at the earliest.

Hickmore argued that higher oil prices have brought “three uncomfortable truths” to the fore: inflation risks have not gone away, central banks do not have unlimited freedom to cut rates while energy prices are rising and geopolitics carries a real economic cost that cannot be ignored.

UK chancellor Rachel Reeves warned parliament on 9 March that UK inflation is likely to rise in the coming months. Meanwhile, a Bank of England rate cut in March, which futures markets had considered near-certain after four cuts in 2025, is now in serious doubt and Fed rate cut expectations have been pushed out to September at the earliest.

“Bond yields are reflecting all three,” he said. “Until oil prices stabilise and geopolitical risks recede, investors are likely to continue demanding a higher premium for holding bonds. That is not panic. It is rational pricing in a less predictable world.”

5. Why this matters in the UK

The UK faces the Iran crisis from a position of particular vulnerability. It is a major energy importer, services inflation has already proven stubborn and households were only beginning to see some relief on energy bills when the conflict began.

For the gilt market, Hickmore identified two direct consequences. Higher inflation risk pushes gilt yields up as investors demand greater compensation for holding long-dated government debt, at the same time as fresh energy price pressure gives the Bank of England less room to cut rates, even if economic growth remains weak.

“There is also a fiscal angle. Higher gilt yields feed through into higher borrowing costs for the government over time,” he concluded.

“That tightens the budget constraint and reduces room for manoeuvre elsewhere. In that sense, rising oil prices do not just affect motorists and energy bills; they show up in the cost of financing the state.”