Investment risk systems designed to protect portfolios are instead pushing investors towards danger, according to Nick Clay, manager of the Redwheel Global Equity Income fund.

The problem stems from a flaw in how risk is measured. The industry, and therefore asset managers, have been treating benchmarks such as the MSCI World as the risk-free version of what an active manager does, which means risk systems tell investors to reduce risk by moving closer to the index.

“When you plug your portfolio into risk systems, they tell you that to reduce risk, you need to be closer to the benchmark,” Clay said. “If I want to reduce risk, I need to buy more Nvidia.”

That logic works when markets are broad and diversified. But when the benchmark itself becomes concentrated, narrow and expensive, it becomes risky. “Having a system that tells you to reduce risk by getting closer to the risky thing turns the whole logic on its head,” he said.

The consequence is that either “people know they're taking on too much risk, but their systems won't allow them to move away, or they think their systems are telling them the truth and that getting closer to the benchmark must be safer.

“At extremes in markets, risk systems get turned on their head and tell you to do the opposite of what you need to do.”

Clay's warning comes as markets are experiencing a return to volatility. After three consecutive years in which the MSCI World delivered around 20% annual returns, investors have become accustomed to a backdrop that is anything but normal. The long-term return is around 8% to 9%, he noted, meaning recent years have been massively ahead of the norm.

“Everybody now thinks that is a normal backdrop, whereas when you look back through history, you get long periods of volatility in markets. That is actually a normal scenario.”

In recent weeks, there have been multiple sharp sell-offs, some broad-based, such as those following the outbreak of the war in Iran, some more contained and triggered by relatively small events, such as the launch of new tools for AI.

“A couple of AI bots get announced, and everybody starts to panic, and certain parts of the market get taken out,” Clay said. This is what we saw happen with asset managers some weeks ago.

Overconfidence generates complacency and complacency increases the likelihood that small shocks will trigger violent moves.

To explain this, Clay used the Thanksgiving turkey analogy. The turkey's confidence in the butcher peaks the day before Thanksgiving because the butcher has fed it every day up until then. “The absence of risk that creates the risk itself. It's the complacency that there is no risk to worry about that actually increases the presence of risk.”

The turkeys, in his view, are those who have become over-committed to the continuation of a single trend.

“By over-committed, I mean over-levered. You become so complacent you think there's only one outcome, so you bet everything on that outcome happening. In a world abundant in liquidity, you end up over-leveraging those positions and have no downside protection.”

The shift back to volatility requires a fundamental rethink of how to manage money, Clay argued. When markets go up in a straight line with minimal volatility, investors need to focus on upside capture to keep pace. When volatility returns, the maths of compounding changes.

“When things are more volatile, even if they're still going up, mathematics tells you that you need to do something different. You need to worry much more about the downside than the upside. That's just the maths of compounding.”

The problem is that almost everyone has become obsessed with upside capture after years in an abnormal environment.

“That requires a sea change in the way people think about managing money, where downside capture becomes much more important than upside capture,” he said.

Part of the challenge is human nature.

“The more people involved, the more human bias shows itself. Greed and fear drive us,” Clay said. “When everything goes up, everyone gets greedy. When your neighbour can afford a Porsche after three months, you get jealous.”

Willpower alone is not enough to overcome these biases. “I don't believe I could adopt a moral fibre strong enough to overcome my own bias. I need a discipline that forces me to do something else.”

Redwheel Global Equity Income can only buy stocks that yield 25% more than the market and must sell any stock that yields less. “Those disciplines preclude us from being in crowded trades. It doesn't matter how much Nvidia goes up or how much my risk system screams at me. I can't buy it.”

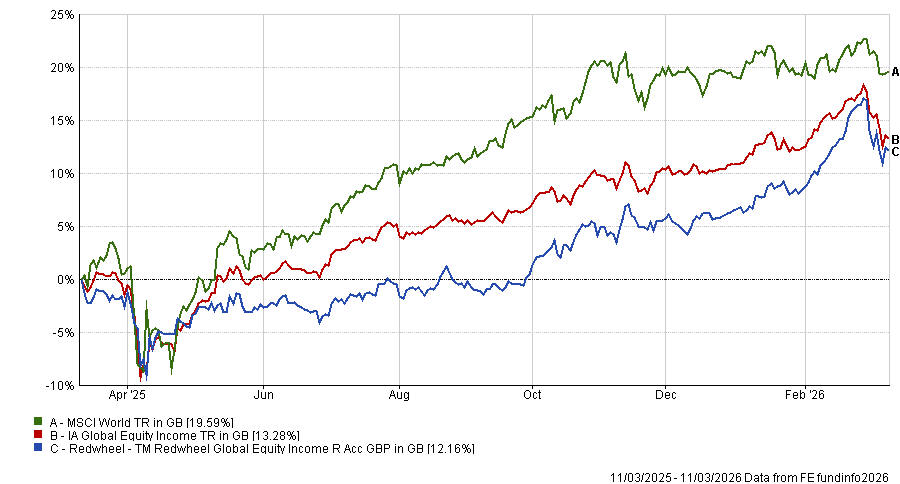

Performance of fund against index and sector over 1yr

Source: FE Analytics

That discipline has kept the fund out of the most expensive parts of the market. America is the fund's largest underweight. Instead, the portfolio tilts towards defensive businesses with pricing power: consumer staples, luxury retailers serving wealthy clients and companies that are either impossible to disrupt or have time to adapt because they provide mission-critical services.

The portfolio's beta is around 0.6, with downside capture running at approximately 60%. “Protecting on the downside is the most important thing,” Clay concluded.