Environmental, social and governance (ESG) focused investment strategies have endured a difficult spell in recent years, as weakened investor sentiment has led to a steady stream of outflows.

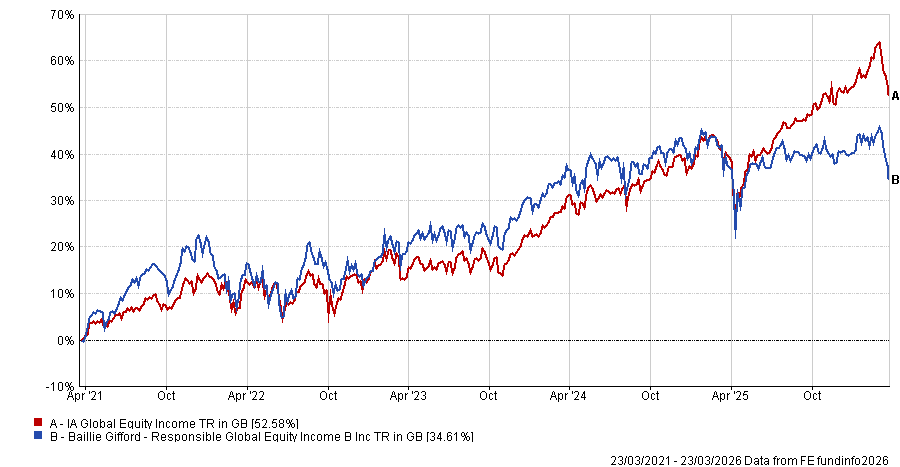

Against that backdrop, the £1.1bn Baillie Gifford Responsible Global Equity Income, co-managed by James Dow and Ross Mathison, has found itself slightly out of step, posting fourth-quartile returns in the IA Global Equity Income sector in both 2024 and 2025.

Performance of the fund vs sector over 5yrs

Source: FE Analytics

Dow maintained that the strategy’s recent challenges reflect the sharp sector and style rotations of the past two years rather than any strain on its responsible investing framework.

“[The fund’s recent underperformance is] not because of responsible investing or exclusions but largely because of the massive rise of AI winners that we – for a variety of reasons – haven’t deemed appropriate for this strategy,” he said.

Dow noted that it would be difficult to include highly volatile stocks such as Tesla in a portfolio built as a “sleep-well-at-night” resilient compounding strategy. “And Nvidia wouldn’t fit that steady profile either,” he added.

He added that Baillie Gifford are long-term investors with a five-year investment horizon, “so our view is that you don’t really see the results of the fund until at least that long into an investment”.

The fund has outperformed over the longer-term, posting first-quartile returns in 2019 and 2020.

Dow remains confident in their approach, adding that “given the geopolitical situation, we might be at the point where resilience might be more valuable”.

What is the process for your fund?

We are trying to solidly grow our unitholders’ capital and income over the long term.

We look for opportunities within the 10% territory – 10% growers, 10% compounders. So we are not super‑rapid growth – which Baillie Gifford is often known for – but we are not a bond‑proxy fund either.

How is the fund ‘responsible’?

For us, being responsible means a range of different measures, as responsible investing is not just a sledgehammer one-and-done approach.

It means UN Global Compact compliance and net zero alignment for climate-material holdings. We also have our own detailed framework – Impact, Ambition and Trust – to make sure that all the companies we invest in are behaving responsibly and improving [their sustainable performance].

As an example of how this translates into investment decisions, we do not own McDonald’s in the fund. It passed our ESG sector and UN Global Compact screens but it did not meet the bar we set for product impact, operational impact and ambition, so we chose not to buy it.

Are there any sectors you currently avoid due to ESG-related risks?

We immediately exclude certain sectors: alcohol, tobacco, gambling, adult entertainment, armaments and oil. But sustainability is a broad umbrella [and some sectors are greyer than others].

While we don’t have an explicit exclusion on animal products or animal testing, for example, we don’t currently invest there.

There are possible negative implications across food, cosmetics and luxury goods that would require proper analysis to be comfortable with it.

Testing something on animals – say, in pharmaceuticals – might be important if the company hopes to cure disease but then you must weigh up whether the harm is therefore justified.

Why are you underweight the US?

We are about 20 percentage points underweight versus the benchmark [MSCI ACWI] and overweight European companies.

That stems from a few things: the income mandate and where income is paid; valuations, where European‑listed companies that do most of their business in the US often look more attractive; and durability and resilience.

The benchmark has two‑thirds in the US. If we wanted to hug the benchmark – that feels like a large concentration. Then when it comes to responsible investing criteria, sometimes that is more challenging with US companies, as some have pulled back [due to the anti-ESG backlash in the US] and would not be appropriate for our fund.

However, there is a narrative that the US doesn’t do sustainability and Europe does, which is too binary. The reality we see and invest in is more nuanced. The US is diverse and many companies remain committed to running responsibly.

Regardless of what an administration promotes or demotes on the agenda, companies like US-based portfolio holding Procter & Gamble recognise that customers care about sustainability. It would be bad for business not to move with their customers and with the times.

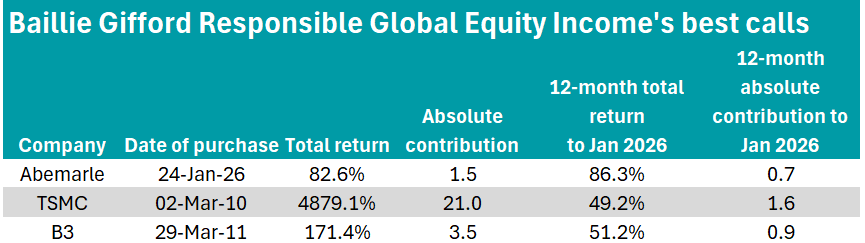

What were your best calls over the past year?

Some of the strongest names in the 12 months to the end of January 2026 were lithium producer Albermale, AI player TSMC and Brazilian financial exchange business B3.

Source: Baillie Gifford

[Each of these funds were purchased when the fund was known as the Global Income Growth Fund.]

TSMC doesn’t require much explanation – it has done incredibly well within the AI surge.

When looking at Albemarle, 18 months ago the stock market believed that electric vehicles (EVs) were dead, nobody wanted a battery anymore and lithium would be oversupplied.

Yet if you look at China – an even bigger market than the US for vehicle sales – EV and hybrid penetration continues to rise and electrification globally continues to go up, even if headlines suggest otherwise. So we added to our position.

Lately, it has become clear this is a supply‑constrained market and demand is growing ahead of supply, so the share price has done extremely well. If oil prices continue to go up, that is also fantastic for Albemarle.

There has also been a lot of pessimism around B3, regarding government intrusion and a new competitor. We have owned the company for over 10 years and we have seen such stories come and go, so we took the view that pessimism was wrong – and that has proved to be the case.

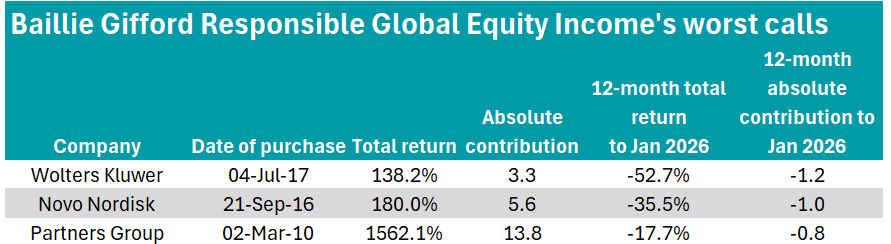

And your worst calls?

On the flip side, the three worst have been pharmaceutical giant Novo Nordisk, information-services business Wolters Kluwer and private asset manager Partners Group.

Source: Baillie Gifford

Partners Group has had a poor period over the past 18 months and Wolters Kluwer is seen as an AI loser by the market, pushing its share price down.

Novo Nordisk is one where two things happened that we didn’t see coming. One is that illegal copycat drugs out of China were able to get into the US market. Normally the US shuts that down quickly but that has not happened and it has been disruptive to the market for Ozempic/Wegovy‑type drugs. That has led to price reductions, which were unexpected.

The other thing is that competition has stepped up, particularly from Eli Lilly, which has had some good products coming onto the market.

The stock market had thought Novo Nordisk was a one‑way ticket to fame and riches, but those two things have gone wrong in the past 18 months and the share price has been hammered.

We have learned that competition in obesity treatments will go back and forth but we have been surprised by how volatile that has been. We are nonetheless holding on because we are confident it will swing back.

What do you do outside of fund management?

Outside work, I have two kids that keep me more than occupied ferrying them around.