FE fundinfo Alpha Manager Anthony Lynch is perhaps best-known for his work on the Mercantile Trust, which he has run since 2012, but he was also named co-manager of the JPMorgan Claverhouse trust in 2024.

He was brought in with co-manager Katen Patel to help longstanding manager Callum Abbot, with whom he has worked with on the JPM UK Equity Plus fund for nine years. The duo also bring experience running an open-ended fund “where the track record has been better over time,” said Lynch.

“I think we’ve taken some of the learnings from the way we managed that open‑ended income fund and we are applying them now in Claverhouse.”

Since his arrival, the trust sits is ninth in the 17-strong IT UK Equity Income sector – exactly where the manager wants to be.

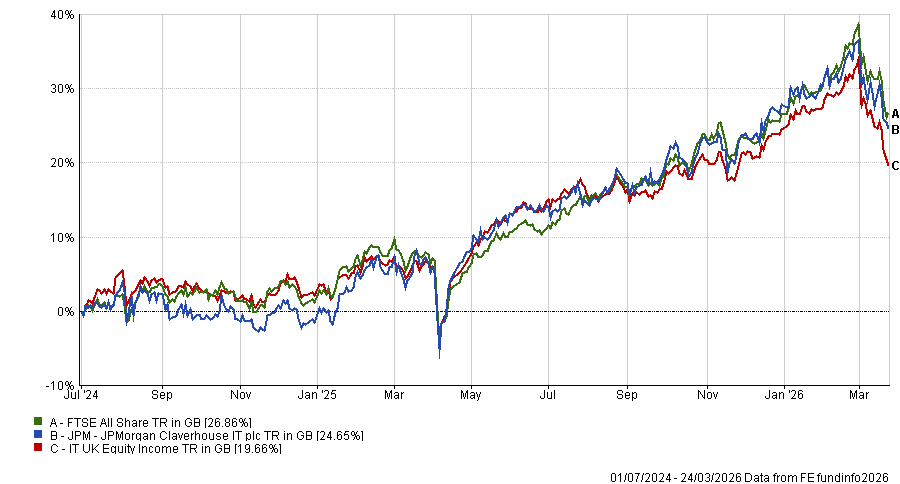

Performance of trust since manager start

Source: FE Analytics

Over the short term, the managers want the trust to be consistent, achieving good returns across the market cycle while avoiding large swings. This, said Lynch, should lead to top returns over the long term.

This is a departure from the trust’s long-term track record, which has been more feast and famine. Top-quartile efforts in 2017, 2018 and 2021 have been surrounded by years of below-average returns over the past decade.

“We are now more fundamental. We do more work on the holdings that we invest in and, as a result, we have higher conviction in those holdings. We’re less likely to suddenly want to change the entire portfolio because of a macro event. That’s something we would observe Claverhouse used to do,” he said.

“We’ve also brought more UK breadth. Katen started in small‑cap, I started in mid‑cap and Callum started in large‑cap. Bringing those three together gives us a really good view of the whole UK market.”

Below, Lynch explains why the trust is not fully geared, why the trustit owns AstraZeneca despite the managers not liking the stock “that much” and how he might be responsible for his son’s football team being relegated this season.

What is your process?

We think that good businesses, where things are getting better and where the valuation is attractive, will outperform. So we systematically screen for companies that have these characteristics.

We then undertake fundamental analysis to make sure that the investment case really stacks up on its own legs.

There are a number of metrics for each of the components of that process. From a valuations perspective, generally we are looking at price-to-earnings (P/E) ratio, free cashflow yield and dividend yield.

When we move to quality, we’re looking for companies that have higher returns on invested capital. That can be a bit of a proxy for barriers to entry and the management making good investment decisions over time.

And then we’re looking for companies that aren’t consistently delivering downgrades., setting We’re looking for companies that set expectations conservatively and then beating them over time.

[Companies must then] either have a very strong dividend yield today or the ability to grow that dividend materially into the future.

Is the trust benchmark-aware?

We focus our time and attention on trying to outperform the benchmark, not on absolute returns over time. From a risk management perspective, that means managing the fund actively relative to benchmark weights. ISo if you looked at our active top 10 relative to benchmark, it would be very different from the absolute top 10.

We go overweight the names we like, such as . Take a name like HSBC. Our view is it is a fantastic business and we want to be overweight. It would be bonkers to underperform the benchmark despite liking HSBC because we refused to express that conviction.

If we don’t like a name we usually own zero. For example, we don’t own a single share in Diageo, even though it’s a large index weight.

But that it not always the case. We don’t like AstraZeneca that much, but we also don’t want to take a huge bet against it. It’s expensive versus GSK, but AstraZeneca has an incredibly strong R&D track record and no obvious patent cliffs.

It can surprise with a blockbuster, so for risk‑management reasons, we keep that one nearer neutral. What we’re trying to do is avoid shocking relative performance versus the benchmark – because that’s what we’re measured against.

What has been your best performer over the past year?

The three best-performing sectors in the FTSE All‑Share last year were aerospace and defence, banks and insurance. We were overweight all three. So the sector allocation –which was a function of bottom‑up stockpicking – was really supportive.

If I had to call out a specific stock, our best contributor was Serco, which is up about 90% over the past year.

Serco is a company with a very chequered history -, it almost went out of business a decade ago. It was a government outsourcer taking too much risk.

But what we spotted 12–18 months ago was that, even though the organic growth was mediocre and it was still losing some big contracts, good quality bid-flow had really picked up, which was highly likely to lead to an acceleration of organic growth.

We were able to buy the shares on 9x earnings and it has re-rated to 15x.

And your worst?

One of the benefits the new portfolio‑management team has brought is clearly a better understanding of the smaller and mid‑cap universe. But one of the problems with that has been that the UK domestics – which are a chunk of that domestic small‑cap universe – have underperformed pretty consistently for the past few years.

We’ve probably been a little bit too early leaning into that part of the market, driven by the fact that domestic confidence hasn't kept up with the actually strong position we're seeing in households.

So byBy being about 10% overweight in small-caps relative to the benchmark, and with that part of the market underperforming by about 10%, that has been about a 1% drag on performance.

Of all the domestics, Hilton Foods would have been the worst. That cost us 30 basis points over the past 12 months and we have now exited.

The trust’s gearing is around 6% but can be as high as 20%. What is the rationale behind the current level?

We’re fortunate to have a £30m long‑term facility that’s priced at 3.2% and I have high confidence that Claverhouse can make a lot more than 3.2% per year over the long term.

With RCFs (revolving credit facilities) you’d be paying about 5-6% interest on one of those facilities [at the moment]. The long‑term return from UK equities is about 6% per year, so you’d be taking on incremental risk for maybe a break‑even return over the long run.

What we’ve done, rather than taking an RCF, is we’ve begun using CFDs [contracts for difference], which means we don’t have a fixed gearing amount that must be deployed, we can draw on it case‑by‑case and it’s actually slightly cheaper than an RCF.

That’s something we introduced about six months ago and we’re still testing it out, but we've been using it to add some incremental leverage.

What do you do outside fund management?

I’ve got two boys, so that takes 100% of my time. They play school sports on Saturdays and club sports on Sundays. Most evenings they have training as well.

I spend a huge amount of time taking them to football, watching them play, and I also coach one of their teams. My track record as a coach is not worth shouting about – I think we’re going to get relegated this year and I’m sure that will be blamed on the coach rather than the players, which is entirely fair.