While some investors in UK equities remain patiently hopeful that UK small- and mid-caps will rebound, others are not prepared to make that call.

Callum Abbot, lead manager of the £1.5bn JPM UK Equity Core fund, said he is not actively betting on mid- and small-cap stocks rebounding and the portfolio reflects this.

As of 31 March 2026, over 80% of the fund’s assets are invested in companies with a market capitalisation above $10bn – with just 1.4% in stocks below $1bn (the dollar thresholds likely reflect standard industry practice for outlining market cap).

“If you look at the 2010s, you would have wanted to be overweight smaller and mid-cap companies – in the past five years, you would have wanted to focus on large-caps,” he said.

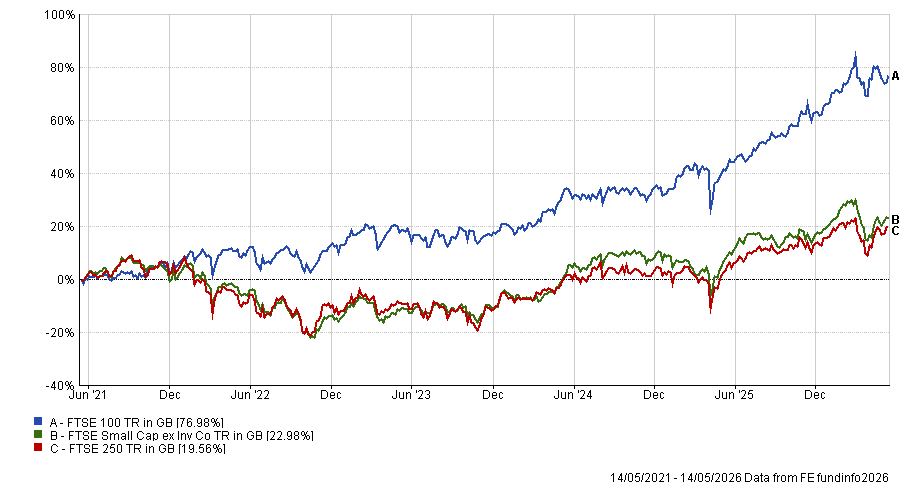

Indeed, over one, three and five years to the end of April 2026, the FTSE 100 has beaten both the FTSE 250 and FTSE Small Cap ex Investment Companies index.

In 2025 alone, the FTSE 100 returned 25.8%, while the FTSE 250 made just shy of 13% and the FTSE Small Cap ex Investment Companies index gained 10.9%.

Performance of FTSE large-caps vs small- and mid-caps over 5yrs

Source: FE Analytics

“If you are taking a big bet on small- and mid-caps, that [divergence] is a big hurdle to overcome,” Abbot said.

“We would rather not take that risk and instead take our risk budget elsewhere and pick stocks that achieve equally strong momentum within that awareness of size risk,” he said.

Below, Abbot discusses the fund’s process, recent stock calls and where he is finding opportunities today.

What is the process of the JPM UK Equity Core fund?

Our investment philosophy is to build a portfolio of around 180 stocks with cheap, better-quality and stronger momentum characteristics, and then manage as much of the incidental risk as we can – things like size risk, macro risk, beta – where we don’t necessarily have an edge and don’t want to use up our risk budget.

We focus that risk budget – our tracking error range is typically around 0.75-1.25% – on stock selection: identifying stocks we think are going to outperform and underweighting those we think are going to underperform.

When we do our stock selection, the starting point is a quantitative screen on value, quality and momentum factors, which ranks every stock in the investable universe. So straight away you have a pretty decent idea of where you want to look and what you want to avoid.

Is the UK stock market as exposed to the struggling domestic economy as some may assume?

Many conflate the UK economy with the UK market. But, if you look at the FTSE 100, the vast majority of revenues come from overseas, with less than 20% of revenues coming from the UK itself. And the FTSE 100 now makes up about 85% of the FTSE All Share because it has outperformed materially over the past five to 10 years.

So what investors actually get is a diversified international market that trades at a significant discount to the MSCI World index.

What are some of your best calls in the past 12 to 18 months?

Some of our recent best performers are the defence-exposed contractors – names like Babcock, which is primarily defence but has some civil work as well, and Serco, which is about 40% defence but also has several other civil lines.

Over the past year to the end of March 2026, Babcock’s share price is up about 60% and Serco is up about 85%. The reason for that success is partly related to general excitement about defence spending across Europe, but also, they are winning contracts.

If you look at their pipelines, there is plenty of reason to think that continues.

Serco is reporting the biggest pipeline it has had in the last ten years and 50% of that is in defence exposure in the US and Europe. Other parts of the business are also going well, and they have really done a great job of making sure their bid process is as effective as possible and winning lots of contracts, which is their lifeblood.

Babcock similarly is capitalising on massive opportunities across all their major divisions.

Where are you finding other interesting opportunities at the moment?

A different name we like is Games Workshop.

They have got the latest Warhammer 40K series release coming this year – they normally do one every other year and it drives a lot of demand.

If you think about big fantasy universes that have been created – like Star Wars and Pokémon – those franchises have demonstrated their ability to monetise their IP.

I think Games Workshop is just at the start of that as it is signing TV deals and leveraging video games, and that helps drive demand back to the original hobby of tabletop miniatures that people buy, paint and play games with.

We see it as a nice structural growth story we can see going on for many years.

What has been your worst call?

We were overweight housebuilders up until the third quarter of last year.

On the face of it, they looked very cheap and that reflected several headwinds: inflation driving interest rates up and hitting affordability through mortgages, the end of Help to Buy, fire safety regulations leading to significant cladding charges on already-built buildings and the well-documented slowness of the planning system.

We were overweight because valuations were cheap; if you looked at the fire safety changes, housebuilders had taken significant provisions; we were seeing inflation coming down slowly; and the Labour government had talked about wanting to free up planning.

As results for the first half of 2025 came in, it became evident that the rate of improvement was too slow. It wasn’t going to be a V-shaped recovery but rather a bathtub-shaped one, so we reduced quite significantly.

We sold out of Taylor Wimpey. In the 12 months up to when we were selling out, Taylor Wimpey was down about 30%, so pretty painful, and the sector had generally underperformed a fair bit in what had been a rising market. It is now one of our larger underweights.

How do you approach stocks or sectors that have had a tough run?

A lot of our philosophy is based on behavioural economics, where one of the key points is to be wary of your emotional biases.

It is very easy to say “I’m never going to own that”. If we see an improvement and we think the cycle has turned, we are always keen to take a closer look.

Rolls-Royce [which is held in the fund] would be a good example. It was tough for the company for around 15 years. It had signed contracts for engine maintenance at the wrong price, had no bargaining power with customers – it was brutal.

Then the pandemic happens, Airbus and Boeing massively changed their workforce, and suddenly the supply-demand dynamics completely turned on their head and Rolls-Royce has phenomenal bargaining power. It’s probably 17-20x off the lows nowadays. And this is a stock many said they would never touch again.

Banks are another example. How many fund managers in the 2010s said banks were structurally defunct and that they were never going to own them? Look at what has happened since 2023 – they are some of the best-performing stocks in the FTSE.

So, on housebuilders, I will never say never. These are on discounts to book now and they normally trade at around 1.4x – so they could probably double when the cycle turns. You just need to keep a close eye on them.

What do you get up to outside of fund management?

I have three young children, so keeping them happy and busy is probably number one outside of work. But I have also always loved sport and reading.