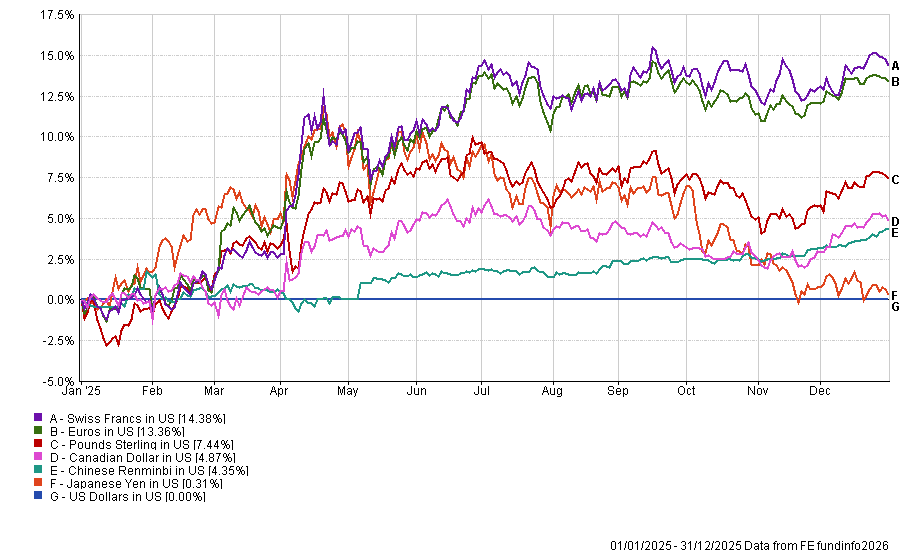

The US dollar has been on a turbulent ride since Donald Trump secured his second term in the White House, swinging from a steep decline in 2025 to a rebound in more recent weeks.

Last year’s ‘Liberation Day’ tariff announcements sent the dollar tumbling, contributing to a near-10% fall in the dollar index – its worst annual performance since 2017. That weakness continued into January 2026, when the dollar hit four-year lows against other major currencies.

Performance of the US dollar vs other major currencies in 2025

Source: FE Analytics

However, the trend reversed last month as the conflict between the US, Israel and Iran erupted, triggering safe-haven flows, lifting oil prices and reducing expectations of US Federal Reserve interest rate cuts.

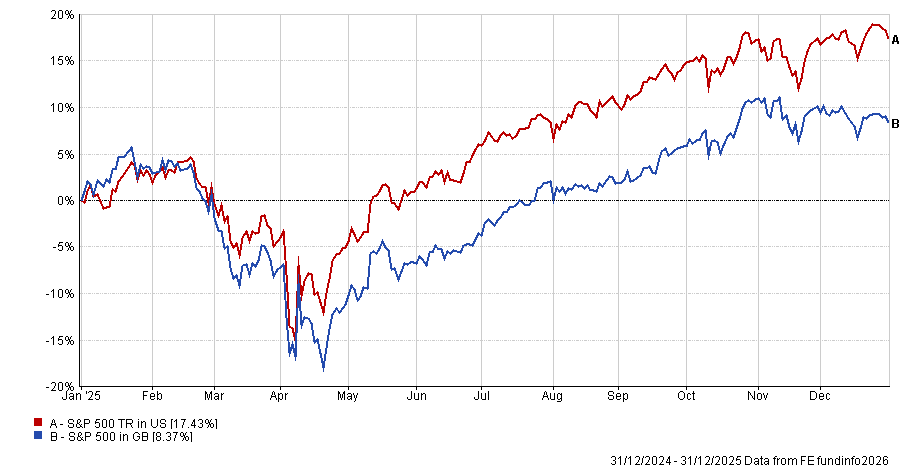

For UK investors, these swings matter because, when a foreign currency falls against sterling, the value of overseas assets in portfolios can drop.

As shown in the graph below, although the S&P 500 (in dollar terms) would have made around 17% in 2025, UK investors made less than half at 8.4%.

Performance of S&P 500 in dollars vs sterling in 2025

Source: FE Analytics

Against this backdrop, Trustnet asked fund selectors which funds and investment trusts could help investors limit their exposure to dollar volatility or cushion its impact.

Direct beneficiaries of a weaker dollar

Emma Bird, head of investment trust research at Winterflood, focused on emerging market equities with her pick of BlackRock Frontiers Investment Trust.

“Many emerging market countries and companies issue debt in US dollars, with a stronger dollar making this debt more expensive to repay, as well the fact that periods of US dollar weakness can trigger investors to seek higher returns outside of the US,” she said, noting that the trust would likely perform well in such an environment.

The £344.5m trust is co-managed by Sam Vecht, Emily Fletcher and Sudaif Niaz and charges a 10% performance fee on annualised excess NAV returns against its blended benchmark. It is currently trading at a 5% discount to NAV.

“Frontier markets are currently trading at an historically wide valuation discount to developed markets and the managers of [the trust] believe that this valuation discount could narrow in the near-term as a result of investors looking to diversify away from the US,” Bird said.

Meanwhile, Quilter Cheviot senior fund analyst Carly Moorhouse, suggested the value-biased Merlin Fidelis Emerging Markets, co-managed by Aaron Macksey and Sam Dyson.

It is a well-diversified portfolio of 60-80 companies across 20 different developing countries and therefore currencies.

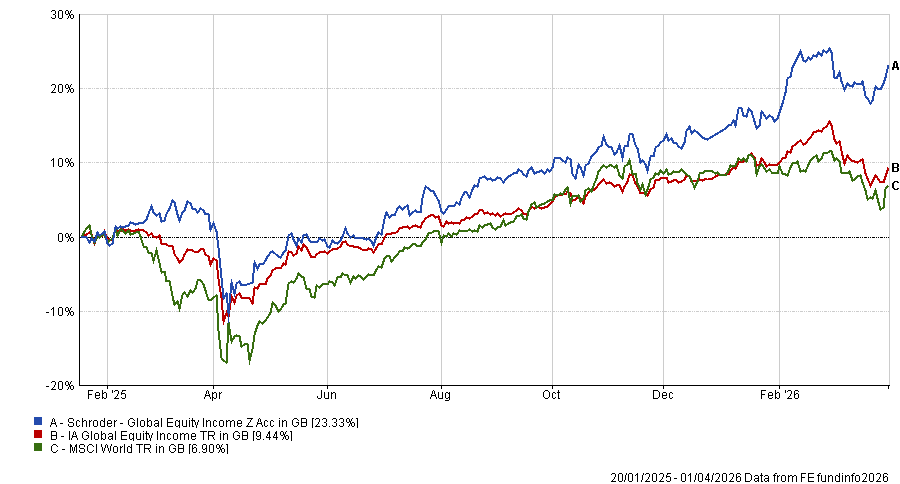

A global fund with little US exposure

Paul Angell, head of investment research at AJ Bell, noted that holding less in US assets can limit the impact of US dollar volatility on an investor’s portfolio.

He said Schroder Global Equity Income “is a good diversifier to a weaker US equity market given its relatively low US weighting, with around 35% versus 70% for the MSCI World index”.

“Additionally, its deep value bias should also provide a cushion to broader market losses, with the fund sitting on just an 11x price to earnings (P/E) as of 28 February 2026 versus 24.7x for the global index,” Angell added.

The fund, which is co-managed by Simon Adler and Liam Nunn, is overweight Japan, Germany, France and the UK versus the index.

It has also delivered a top-quartile return in the IA Global Equity Income sector in three of the past 10 discrete calendar years – most recently in 2025, when it gained 18.3%.

Performance of the fund vs sector and benchmark since 20 January 2025

Source: FE Analytics

Areas with little-to-no dollar exposure

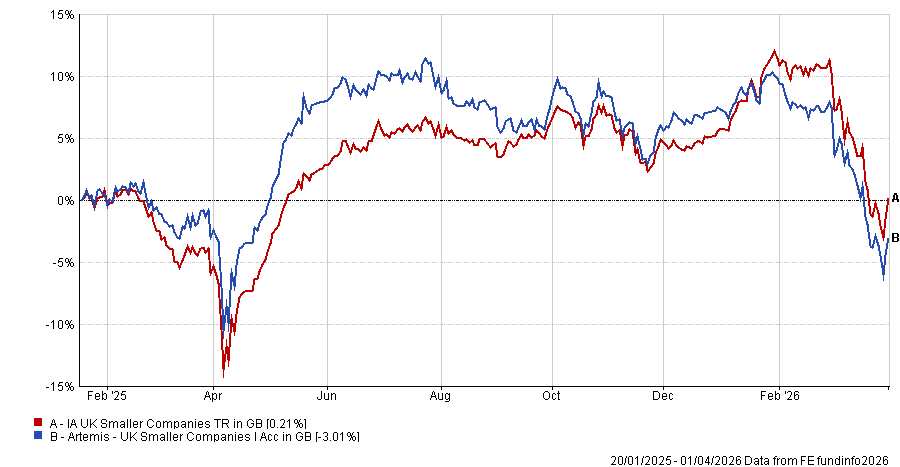

For those who believe a weaker US dollar is likely in the longer term, Ben Yearsley, director at Fairview Investing, also suggested investing in areas with little or no dollar exposure, pointing to Artemis UK Smaller Companies.

“As a fund in an unloved and under-owned sector, it ticks more than just the dollar volatility angle,” he said.

The investment strategy is focused on strict valuation discipline and is based on free cashflow, with its biggest sector weightings in consumer discretionary and industrials.

Performance of the fund vs sector since 20 January 2025

Source: FE Analytics

Elsewhere, Shavar Halberstadt, research analyst at Winterflood, highlighted Ruffer Investment Company’s focus on ‘all-weather’ performance, which incorporates currency risk considerations and aims to achieve capital and income return of twice the Bank of England base rate by investing through internationally listed securities and bonds.

The trust has very little direct exposure – around 6% of NAV as at 31 December 2025 – to the US dollar.

“As noted in the recent interim results, this reflects the managers’ view that the US dollar is becoming a less reliable source of protection due to factors including policy unpredictability, questions around institutional credibility and persistent above-target inflation,” Halberstadt said.

Funds that hedge the risk

Matt Ennion, head of investment fund research at Quilter Cheviot, suggested the £2.9bn RIT Capital Partners – a multi-asset portfolio investing across listed equities, private equity and alternative assets such as credit, hedge funds and gold.

Although he noted the trust has exposure to a “significant level” of US assets at around 50% across all three of these asset class pillars, he said it has a hedging programme “that aims to reduce the overall impact of currency – the US dollar in particular – on total returns for sterling investors”.

“This enables the managers to isolate alpha from asset selection without it being dwarfed by currency moves,” he said, noting that, in the 12 months to 31 December 2025, this programme shielded investors from an 8% US dollar decline versus the pound.

The trust currently trades at a 27% discount to its net asset value (NAV) and has managed a 10.6% average annualised NAV per share total return since its inception in 1988.

Angell also looked to funds which hedge out currency risk entirely, highlighting the £1.6bn Aegon High Yield Bond.

“Funds within the IA Sterling High Yield and IA Sterling Corporate Bond sectors must be at least 80% hedged back to GBP,” he explained.

Co-managed by Thomas Hanson and Mark Benbow, the fund is index agnostic, with the managers believing a passive allocation to high yield bonds is “nonsensical given indices are weighted to the most indebted businesses”, Angell said.

It has posted top-quartile returns in its sector in six of the past 10 discrete calendar years.