Stocks have returned to record highs despite bond markets, commodity curves and real-economy data continuing to price an unresolved energy crisis, investment strategists have warned.

Global stock markets have staged a significant recovery since late March, with the S&P 500 and Nasdaq returning to record highs amid a fragile ceasefire between the US and Iran and early signs of progress in nuclear negotiations.

But the Strait of Hormuz has been closed since 28 February and the last tankers to pass through before the closure are only now arriving at their destinations, meaning the buffer of pre-closure supply has effectively been exhausted.

A ceasefire was announced on 7 April and has since been extended, but shipping through the strait remains well below pre-war levels and negotiations have stalled. Brent crude is trading near $100 a barrel, down from a peak of close to $120 but still around 35% above pre-war levels.

Bond and commodity markets have responded accordingly. UK nominal interest rates have risen by around 50 basis points across the curve since the start of the conflict. Overnight indexed swap (OIS) markets, which entered the year pricing two to three cuts to base rates, now price one to two rises, reflecting a reassessment of the inflation and growth outlook.

Oil and gas price curves continue to show supply tightness in spot and near-term futures contracts. Emma Moriarty, portfolio manager at CG Asset Management, described the gap between those signals and equity market behaviour as “increasingly marked cognitive dissonance”.

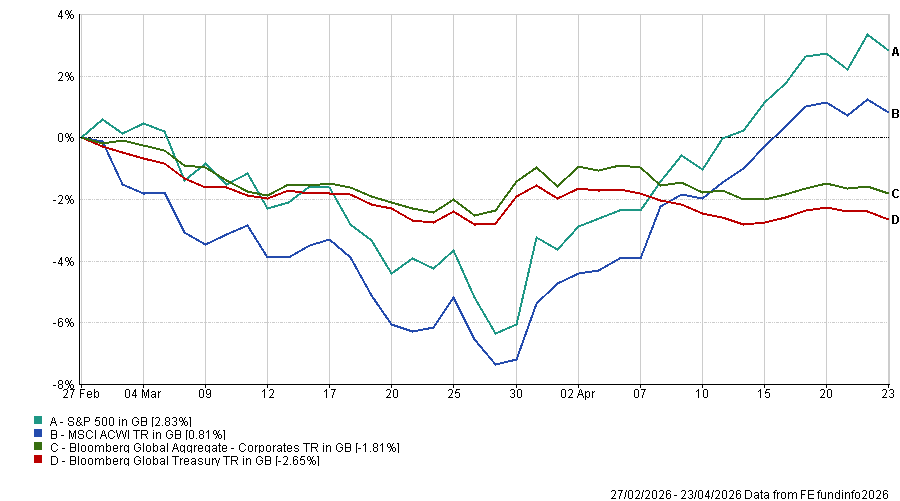

Performance of indices since start of the Iran war

Source: FE Analytics. Total return in sterling between 28 Feb and 23 Apr 2026

The equity rebound has a specific technical explanation. Following a sharp drawdown in March, investors who had cut risk exposure moved back into markets quickly, producing a rally that Benjamin Melman, global chief investment officer at Edmond de Rothschild Asset Management, said ranks within the 100th percentile of 10-day gains recorded by the S&P 500 since 1950.

In his view, the move was driven primarily by short-covering and inflows from underweight investors rather than a material change in the fundamental backdrop. Other investors are also sceptical on the durability of the recent rally.

Laura Cooper, global investment strategist and head of macro credit at Nuveen, added that the conditions sustaining the rally remain conditional: “Markets are holding two contradictory beliefs – record highs and unresolved risk – and trading as though only one matters.”

There is a coherent foundation to the rally, she argued. Bank earnings have surprised to the upside, delivering approximately 14% year-on-year growth. The March retail sales print was the strongest in a year, AI-related enthusiasm has returned to markets and credit spreads have retraced towards early-year levels.

Cooper said consensus S&P 500 earnings growth for 2026 is approximately 18% and Nuveen maintains a year-end index target of 7,500.

The strength is not evenly distributed, however. Growth is concentrated in technology and financial sectors, while broader earnings momentum is more subdued. Elevated gasoline prices continue to weigh on real household spending power, with potential implications for consumer-facing parts of the market.

Valuation metrics add another dimension to the picture. CG Asset Management’s Moriarty noted that the S&P 500 cyclically adjusted price-to-earnings (CAPE) ratio is now in the 99th percentile of its historical range.

The CAPE yield on the index, at 2.5%, has fallen below the 20-year TIPS yield of 2.6%, meaning equities are no longer offering a return premium over inflation-protected government bonds on that measure.

Moriarty also questioned whether AI-driven companies can deliver on the expectations currently priced into markets, noting that higher energy costs weigh directly on the data centre infrastructure that underpins the sector's investment case.

Edmond de Rothschild sees several consequences for different parts of the globe. The US benefits from energy independence, AI-driven investment and greater monetary and fiscal flexibility relative to other developed markets, which Melman said makes it “the main winner (in relative terms) of this new environment”.

The eurozone, where earnings per share is still projected to grow 12% in 2026 and 11.5% in 2027, is a region facing material downward revision risk to both the economy and earnings, he added.

The UK presents a similar tension in a different form. Sterling has held above $1.35, but domestic conditions are softening, with falling job vacancies, elevated labour market inactivity and easing wage growth. An energy-driven rise in headline CPI, combined with persistent services inflation, leaves the Bank of England navigating between an inflation overshoot and a deteriorating growth outlook.

Across Asia, the long-term rise in gas prices – which are up to +120% on some contracts – is also weighing on economic growth and corporate margins.

“The disconnect between stock markets and the momentum of the real economy, akin to a cyclops who only sees the world through one eye, may be a first sign of weakness for the current market regime,” the Edmond de Rothschild CIO said.

Melman identified three fault lines beneath the constructive surface: the energy shock, debt and equity concentration.

The energy shock is deeper than markets are pricing, he said. Gulf producers are cutting output as onshore storage reaches capacity, and the process of clearing stranded tankers, restocking exporting nations and normalising production could take two to three months from any agreement. Fertiliser and food prices face similar pressure.

On debt and leverage, rising sovereign yields are tightening financial conditions structurally. Private credit, where valuations are opaque and liquidity limited, could amplify any external shock even if it shows no systemic stress today.

His third concern is equity concentration. With approximately 14% of S&P 500 earnings growth for 2026 projected to come from technology and cyclical sectors alone, and non-cyclical earnings expectations running around 4% lower, index-level strength is masking a much weaker picture beneath.

Across all four managers, the direction of portfolio positioning is broadly consistent, though the degree of caution varies.

Melman remains overweight equities and credit but recommends building greater portfolio convexity – or options and other asymmetric instruments that limit downside exposure without requiring a full reduction in risk – during periods of lower volatility.

Cooper favours dividend growth for defensiveness, infrastructure for inflation protection and technology for AI exposure. “Any sign of margin pressure, softer guidance, or weakening consumer demand can test the rally’s conviction,” she said.

Moriarty said 45% of her firm’s multi-asset funds are in inflation-linked government bonds at five-year duration, with 24% in risk assets (an underweight) and 31% in managed liquidity.

Cooper finished: “The dissonance cannot hold indefinitely. Markets have been remarkably effective at looking through risks – and may continue to be. But the list of risks is growing as resolutions remain elusive.

“At some point, the weight of what is being ignored could become the only one that matters.”