Three years of failing to beat the market have not moved Nick Train. The manager of the Finsbury Growth & Income trust told shareholders this week that his portfolio's heavy tilt towards digital data businesses and consumer franchises has been “inappropriate” but argued it was the right place to be in the long run.

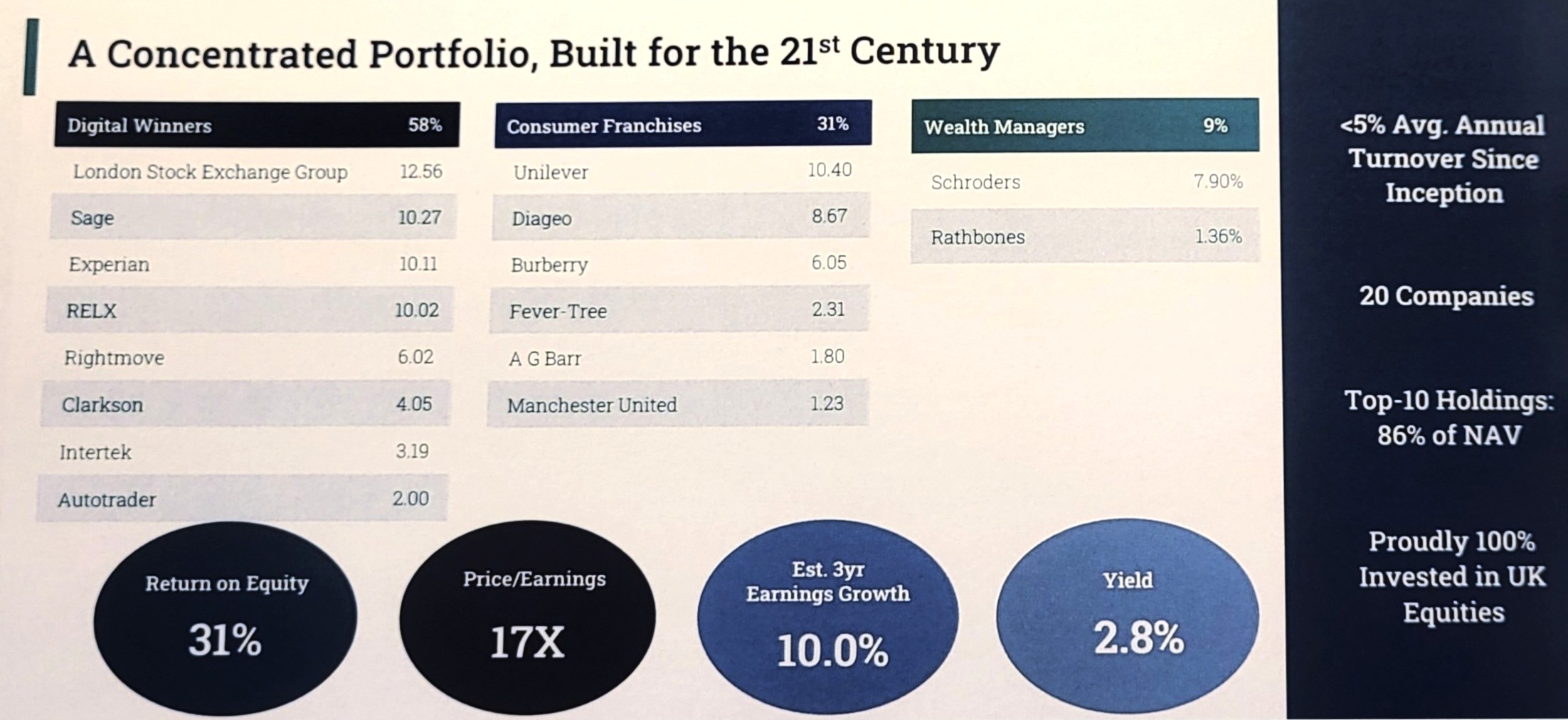

Around 58% of the portfolio sits in what Train calls ‘digital winners’ such as LSEG, Relx, Experian, Rightmove and Auto Trader, which have been losing value in the past three years. A further 31% is in consumer franchises such as Diageo and Brown-Forman and 9% in wealth managers, which have also struggled.

“It was sir Elton John who said that sorry is the hardest word, but I have to say I disagree,” Train said. “Specifically, I am very sorry that Finsbury Growth and Income Trust's portfolio strategy has turned out to be so inappropriate for market conditions over the past two to three years.”

Yet he has no intention of selling, stating that he is “so reluctant to unpick this portfolio allocation and crystallise losses for shareholders”.

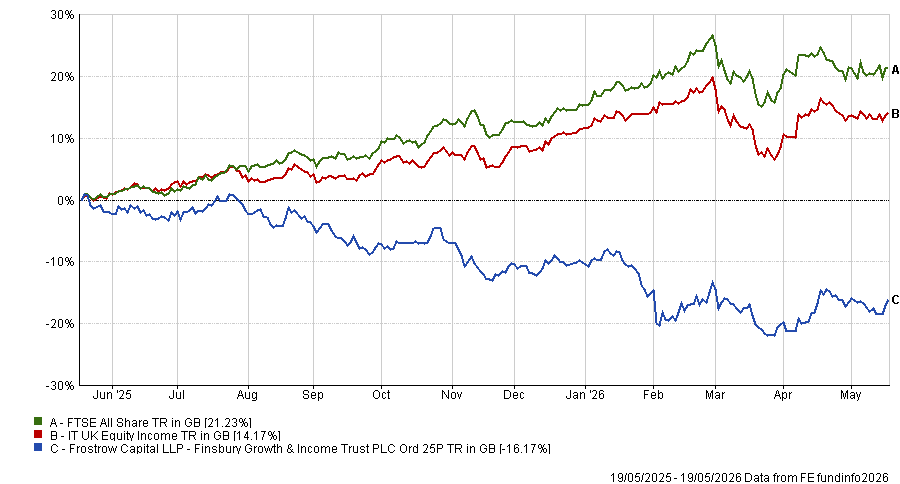

The trust is down 10.1% over three years and 6% over half a decade. This is compared with gains of 45.9% and 67.2% for the FTSE All-Share over the same periods. Over the past year alone, Finsbury has lost 16.2% while the index returned 21.2%.

Performance of fund against index and sector over 1yr

Source: FE Analytics

Train's case for standing firm rests on two propositions. The first is that depressed valuations in the portfolio have begun to attract corporate activity. He pointed to full bids for Schroders and testing and certification company Intertek, both of which remain pending, as evidence that prices have fallen far enough to draw in buyers.

Additionally, spirits company Sazerac made an approach for rival Brown-Forman at a price at least 30% above its current market capitalisation, although the deal now appears unlikely to proceed, according to Train.

Elsewhere, New-York based Elliott Investment Management has taken a stake in LSEG, while activist investors appeared on the AutoTrader share register a fortnight ago.

"When an industry is depressed, industry participants are keen to take advantage of both the depressed trading circumstances and also depressed valuations," he said.

The second argument is more contrarian. The manager believes his concentration in London-listed data platform companies – currently labelled by the market as AI losers – positions the trust to benefit from the growth of artificial intelligence, not suffer from it, as they have proprietary, constantly replenishing datasets that no one else has assembled.

For example, LSEG, the trust's largest holding (12.6%), sits on 33 petabytes of financial data – a 30-year history across more than 90 million instruments, updated 15 million times per second.

That combination of historical depth and constant renewal is what Train believes makes the asset difficult to replicate and increasingly valuable to data-hungry AI models seeking to derive financial insights. The machines, he said, are already paying for access to LSEG’S data and it represents a new revenue stream for the company.

Other examples include Rightmove (6.1%), which logged 69 billion user interactions with its property listings in 2025 alone – data about consumer behaviour and purchasing intentions that Train said no competitor can replicate – and Relx (10%), whose risk division is already operating on a machine-to-machine basis, processing 400 million identity checks a day.

The risk division represented roughly 2% of Relx’ total value two decades ago and, after years of AI-driven growth, now accounts for around half, Train noted.

"Companies that own proprietary data can piggyback off the billions that are being invested by others [AI hyperscalers] to derive proprietary insights from their proprietary data," Train said. "No one has the same scale of exposure that we've built to companies of this type."

The same applies across the portfolio's AI holdings, the manager argued, which is why he sees little sense in selling at current prices. Digital businesses warrant higher valuations than the models many investors built their careers on and he was hesitant to declare any particular valuation excessive.

Discounts on “eternal or semi-eternal assets”, for example spirits brands and consumer franchises, are understandable during a period of rapid technological disruption but that may itself be an opportunity.

The recent underperformance leaves his portfolio in good shape, he argued, with a weighted average return on equity above 30% over the past five years. Meanwhile its price-earnings ratio has fallen to roughly 17x – close to its lowest level since 2013.

Finsbury Growth and Income portfolio

Source: Frostrow, Linsell Train, Bloomberg.

"I don't know if that's the bottom," he said. "But I hope I've given you enough to think about to consider that it might be getting towards a low for the portfolio."