What a difference a month makes. After suffering in March due to conflict in the Middle East, emerging market (EM) fixed income assets enjoyed positive returns in April. The main index for EM hard currency debt, the JP Morgan EMBIGD, was up 2.5% in April; the main index for EM local currency debt, the JP Morgan GBI-EM GD, was up 2.8%; and the main index for EM corporate bonds, the JP Morgan CEMBI BD, was up 1.6%. Returns are positive across the board on a year-to-date basis too.

Markets were cheered by the apparent end of open fighting. Yet risks of a prolonged conflict rose in April after US–Iran peace talks failed during the first ceasefire and the Strait of Hormuz remained largely closed. Although the ceasefire was extended, the strait stayed blocked, keeping headline risk high. While the US reportedly seeks a swift settlement, Iranian leadership prefers to prolong negotiations to extract concessions – and survive the conflict, all the while as risks of a re-escalation resurface. Perceiving the signal amid the noise remains difficult, particularly as market sentiment has reversed repeatedly. Yet sentiment – especially in hard currency debt – remains skewed toward optimism, likely shaped by last year's "Liberation Day" experience, when an initial decline was followed by a robust recovery. It is notable that recent IMF/World Bank Spring Meetings revealed a gap between investor bullishness and political analysts' caution.

With many EM investors entering the conflict at near neutral risk levels, March largely reflected risk rotation in hard currency debt, notably from oil importers to exporters. Local currency debt saw more outright risk reduction instead. Then April delivered a sharp recovery, leaving spreads tighter than at the start of the year. Supported by broad confidence in solid EM economic fundamentals, price action also revealed investor reluctance to take profits despite lingering re-escalation risks. They appear more focused on idiosyncratic alpha opportunities, particularly in frontier markets (FM).

What explains the current interest in frontier markets?

Our recent visit to the IMF/World Bank Spring Meetings, in Washington, DC, where we interacted with officials from international financial institutions and country delegations, offered some insights.

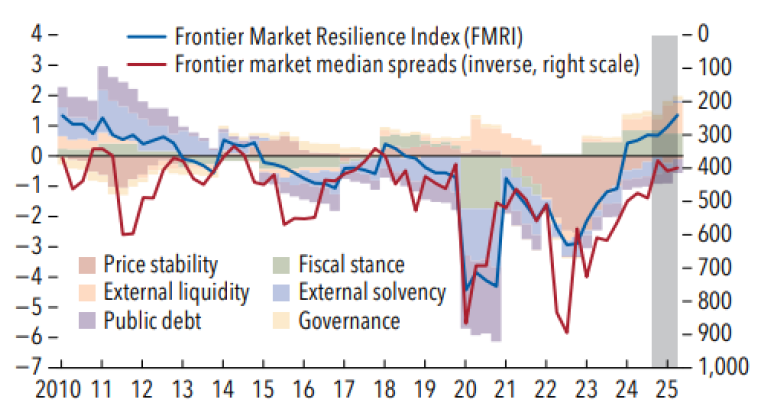

C-rated credits – which are among the riskiest bonds in the EM debt universe – came under pressure in the early stages of the Middle East conflict, but that trend has reversed, and spreads are now tighter year-to-date. The more positive market sentiment after the ceasefire combined with greater FM resilience, which, according to the Frontier Market Resilience Index from the IMF, has improved since 2022 (fig.1). Stronger external positions and lower inflation largely explain the improvement.

Fig 1: Stronger FM go hand in hand with lower spreads

Near-term refinancing needs are also contained, with more substantial maturities coming up in the next three to five years. That said, high public debt levels still weigh on aggregate FM resilience, producing some differentiation amongst credits. This has also been reflected in relative FM performance since the conflict. Should the Strait of Hormuz remain blocked, and energy and fertiliser flows hindered, inflation and balance-of-payments pressures could result in spread widening among the weakest and most exposed FMs. This would also increase their appetite for IMF support. Here are some of the most watched such credits.

The CEMAC region: who blinks first?

The Economic and Monetary Community of Central Africa (CEMAC) is set to benefit from higher energy prices but IMF programmes for its constituents will still likely be necessary because the oil/FX reserves buffer nexus appears looser than thought. "Regional assurances" seem key to secure such IMF programmes. But getting the three largest economies – Gabon, Cameroon and Republic of Congo – on a programme seems unlikely until the turn of the year.

Senegal: plus ça change

An IMF agreement seems some way away, with the Fund arguing for a slower fiscal adjustment to avoid a big impact on economic growth. This brings back on the table a potential debt restructuring. But the authorities have delivered impressive fiscal consolidation over the past year and seem keen to muddle through, with more adjustment and heavy reliance on the regional market for funding. They have often stated their commitment to pay.

Mozambique: vulnerabilities keep heightening

Discussions on an IMF programme have so far yielded limited results, with differences persisting on fiscal and exchange rate matters, while debt remains on an unsustainable path. Security spending and fuels subsidies also weigh on the budget. A strategy to make do until achieving gas production (2029-2030) seems risky given the shallow domestic market. This has raised concerns about another potential debt restructuring.

Pakistan: resilient with manageable outlook

Despite significant shocks (floods and geopolitical tensions), the economy has shown resilience. The reform programme has remained on track, despite the reintroduction of energy subsidies. While the current account deficit is expected to remain contained, FX buffers are modest, if oil prices stay higher for longer. The near-term outlook for external funding is manageable after the government secured USD 3 billion from Saudi Arabia and issued USD 750 million of eurobonds.

Venezuela: a path to normalised relations

The recent IMF recognition of Delcy Rodríguez's administration is a milestone that could pave the way for other international financial institutions to normalise relations. With Venezuela still not having tapped nearly USD 5 billion in IMF funding during Covid-19, this change could deliver significant support. While the Venezuela Creditor Committee of bondholders recently met Trump administration representatives formally for the first time, a comprehensive debt restructuring does not appear to be a priority at this stage.

Giulia Pellegrini is lead portfolio manager, emerging market debt at Allianz Global Investors

Investing involves risk. The value of an investment and the income from it may fall as well as rise and investors might not get back the full amount invested.

Past performance does not predict future returns. If the currency in which the past performance is displayed differs from the currency of the country in which the investor resides, then the investor should be aware that due to the exchange rate fluctuations the performance shown may be higher or lower if converted into the investor’s local currency.

This is for information only and not to be construed as a solicitation or an invitation to make an offer to buy or sell any securities. The views and opinions expressed herein, which are subject to change without notice, are those of the issuer or its affiliated companies at the time of publication. The data used is derived from various sources and assumed to be accurate and reliable at the time of publication. but it has not been independently verified; its accuracy or completeness is not guaranteed and no liability is assumed for any direct or consequential losses arising from its use, unless caused by gross negligence or wilful misconduct. The duplication, publication, extraction or transmission of the contents, irrespective of the form, is not permitted, except for the case of explicit permission by Allianz Global Investors.

This material has not been reviewed by any regulatory authorities.

This document is being distributed by the following Allianz Global Investors companies: In Australia, this material is presented by Allianz Global Investors Asia Pacific Limited (“AllianzGI AP”) and is intended for the use of investment consultants and other institutional/professional investors only, and is not directed to the public or individual retail investors. AllianzGI AP is not licensed to provide financial services to retail clients in Australia. AllianzGI AP is exempt from the requirement to hold an Australian Foreign Financial Service License under the Corporations Act 2001 (Cth) pursuant to ASIC Class Order (CO 03/1103) with respect to the provision of financial services to wholesale clients only. AllianzGI AP is licensed and regulated by Hong Kong Securities and Futures Commission under Hong Kong laws, which differ from Australian laws; in the European Union, by Allianz Global Investors GmbH, an investment company in Germany, authorized by the German Bundesanstalt für Finanzdienstleistungs-aufsicht (BaFin) and is authorized and regulated in South Africa by the Financial Sector Conduct Authority; in the UK, by Allianz Global Investors (UK) Ltd. company number 11516839,authorisedand regulated by the Financial Conduct Authority (FCA); in Switzerland, by Allianz Global Investors (Schweiz) AG, authorised by the Swiss financial markets regulator (FINMA); in HK, by Allianz Global Investors Asia Pacific Ltd., licensed by the Hong Kong Securities and Futures Commission; in Singapore, by Allianz Global Investors Singapore Ltd., regulated by the Monetary Authority of Singapore [Company Registration No. 199907169Z]; in Japan, by Allianz Global Investors Japan Co., Ltd., registered in Japan as a Financial Instruments Business Operator [Registered No. The Director of Kanto Local Finance Bureau (Financial Instruments Business Operator), No. 424], Member of Japan Investment Advisers Association, the Investment Trust Association, Japan and Type II Financial Instruments Firms Association; In mainland China, it is for Qualified Domestic Institutional Investors scheme pursuant to applicable rules and regulations and is for information purpose only. in Taiwan, by Allianz Global Investors Taiwan Ltd., licensed by Financial Supervisory Commission in Taiwan; and in Indonesia, by PT. Allianz Global Investors Asset Management Indonesia licensed by Indonesia Financial Services Authority (OJK).