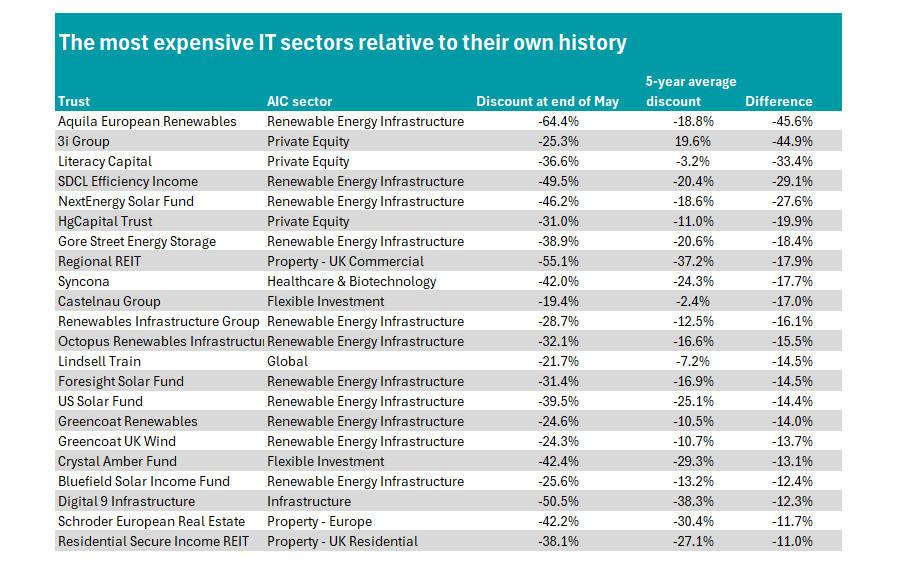

3i Group, Syncona and Lindsell Train are among 22 investment companies whose share prices have become heavily discounted, but it is Aquila European Renewables that is currently the cheapest versus its history.

Cheap trusts can remain cheap for a long time, but those that have recently dropped could represent a buying opportunity if the reason is short-term investor sentiment.

As such, in this study, Trustnet used data from the Association of Investment Companies (AIC) to compare trust discounts relative to their own history to see which have only recently become cheap.

Aquila European Renewables has dropped the most. Its shares have typically been on an 18.8% discount over the past five years but stood at 64.4% at the end of May.

In May, a disagreement between the board and its fund management group Aquila caused a rift. Board members claimed Aquila reneged on selling half of the portfolio, despite the trust being in wind-down.

This month, the chair of the trust has said he is looking into a breach of contract after the firm refused to reimburse legal fees incurred by the failed sale. He also accused the firm of withholding information "material to the company's valuation".

In second place, private equity behemoth 3i Group is significantly cheaper than its medium-term average. The trust, which has traded on an average premium of 19.6%, is currently on a 25.3% discount.

Much relies on the trust's largest holding: Action, which makes up almost three-quarters of the trust. 3i Group plummeted when it warned Action's sales growth was weakening in France, its premier market, and highlighted uncertainty relating to the Iran war.

However, shares may not be as cheap as they were at the end of last month as the trust's fortunes have improved over the past month.

Shares are up almost 8% over the past month after an update from Action encouraged investors. Like-for-like sales grew 3.3% from 31 March to 21 June, slightly below the previous quarter.

It was one of three private equity trusts significantly cheaper than their long-run average alongside Literacy Capital and HgCapital Trust.

Source: FE Analytics

The area to pick up a discount appears to be the IT Renewable Energy Infrastructure sector, which accounts for half of the table above.

Alongside Aquila European Renewables, SDCL Efficiency Income is another in managed wind-down. The third-cheapest trust in the sector is NextEnergy Solar, on a 46.2% discount at the end of May.

It disappointed investors with a dividend cut in March and fell again earlier this month when it revealed a net asset value (NAV) drop of more than 10%.

QuotedData senior analyst Matthew Read said the latest results were "a difficult read for shareholders", although he noted that the reasons for this (policy changes, higher rates and weaker price assumptions) are well understood.

"If the trust can demonstrate that the strategic reset can stabilise NAV and therefore rebuild confidence, the discount has the potential to narrow meaningfully," he noted.

Lindsell Train trust is the sole traditional equity investment company on the list. The trust has suffered the worst performance in its 25-year history, manager Nick Train told investors in the trust's annual report earlier this month.

Still, shares have widened significantly from an average 7.2% discount over the past half a decade to 21.7% today. However, up until 2023 it was rare for Lindsell Train to be on a discount at all, with shares trading on a premium as large as 40% in August 2021.

Although the trust is small, it has been popular thanks to its large investment in Lindsell Train Investment Management, which enjoyed a meteoric rise in the 2010s as the quality-growth style of investing paid dividends for investors.

Another lone wolf, Syncona is the standout from the IT Healthcare & Biotechnology sector, with shares on a 42% discount at the end of May, 17.7 percentage points below its five-year average.

Earlier this month the trust revealed results that were encouraging to analysts at both Peel Hunt and Jefferies, which both rated the trust as a 'buy'.

The former said the discount (which has widened further) "significantly undervalues the portfolio", while the depth of its late-stage clinical assets "offers a diversified way to play the biotech recovery at a deep discount to a well-tested NAV".

Analysts at Jefferies noted that Syncona's modest NAV drop during its final quarter did little to change the overall picture for the year, with the trust "still likely reliant on a positive clinical readout and/or portfolio M&A to drive both stronger performance and the committed return of capital to shareholders".