Investors who have been trying to cut their technology exposure this year in pursuit of diversification will have noticed how hard it is as more industries and geographies become increasingly dependent on the AI theme.

Fund managers are having similar problems in their asset allocation decisions, including Gabriel Sacks, manager of the Aberdeen Asia Focus trust, who has spent the past six months cutting some of the best-performing tech names in his portfolio only to end up with a higher headline allocation to the sector.

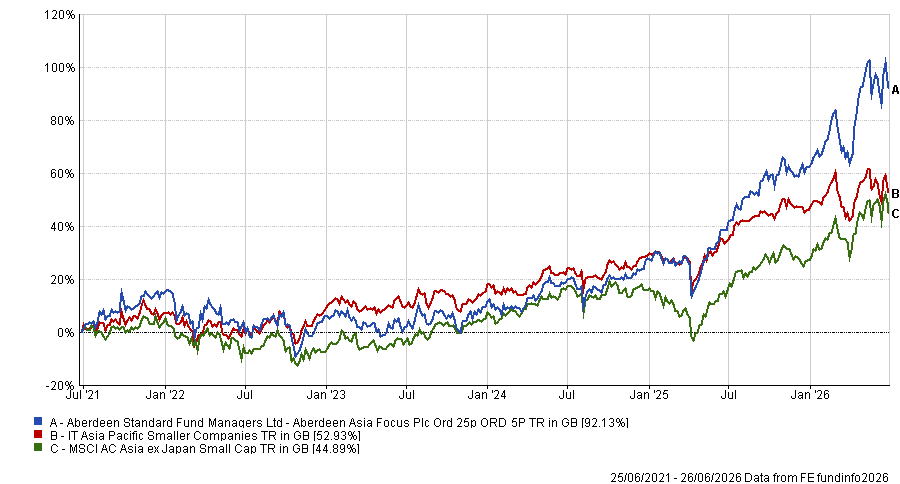

Aberdeen Asia Focus invests in smaller companies across Asia excluding Japan and Australia. It has returned 47.5% over the past year and 99.2% over five years. Its active share sits above 95%, meaning it’s different to the exposure investors would get with the benchmark. But this hasn’t spared Sacks from the structural problem of tech gobbling up indices.

Performance of fund against index and sector over 5yrs

Source: FE Analytics

Relative positioning is important for Sack because he uses the benchmark as a reference point for portfolio construction.

“We use the benchmark as a reference point for portfolio construction, so we want to be clear as to why we overweight or underweight a particular country or particular sector,” he explained.

“And it's not the key consideration, but it is a consideration when it comes to the weights of stocks. We try to keep a single stock to no more than 10% of our tracking error.”

Because of this, and despite his efforts to cut AI names, Sacks has ended up with even more exposure, as the benchmark weighting has moved higher. As he trimmed, Korean and Taiwanese names have re-rated so sharply that his relative tech weighting has kept rising regardless.

“We've been taking a lot of profit from our AI winners, which has been a bit early,” he said. “We've probably left a bit of money on the table, but we think it's for the right reasons – to diversify and to avoid concentration.”

Two of his largest tech positions, Chroma ATE and Taiwan Union, had been 10-baggers over the four-to-five-year period prior to Sacks cutting. To complicate things even more, selling into strong earnings momentum is difficult.

“When you see that level of return and re-rating, we think it's prudent to top slice, even though the earnings are coming through very strongly,” he said. “The earnings are beating expectations, so when you're in that environment the stocks can continue to run. But what makes us a little bit nervous is perhaps just how sharp the moves have been.”

Retail money flooding into Korean ETFs has added to that unease. “Obviously we don't know if we're going to be early or late, but we felt it was the right thing to do.”

Despite six months of selling, Sacks ended up with more exposure, not less. As he trimmed, Korean and Taiwanese names re-rated so sharply that the benchmark moved faster than his sales.

The market moves have been massive. “If you look at the top 10 markets these days, six out of 10 would be Asia – that includes Japan – but things like Korea and Taiwan have gone pretty bananas lately,” he said. “These are bigger markets than the UK and combined their large-caps are bigger than China and India’s [large-caps] combined.”

Asia now has the same problem as the US, Sacks said, with a handful of names accounting for a disproportionate share of returns: “A third of your portfolio might be in three or four companies.”

Taiwan Semiconductor Manufacturing Company accounts for a large slice, with Samsung Electronics and SK Hynix taking most of what remains.

For Aberdeen Asia Focus, which invests in smaller companies, the exposure looks different but the theme is still present.

“It's not as concentrated [as the index] in single stocks, but it's more concentrated in the AI theme,” Sacks said. “You are getting diversification from single-stock risk, but you do have exposure to a theme.” His direct tech exposure sits at around 24%, against tech's near-50% share of the large-cap index.

“We were probably overweight tech a couple of years ago. We're becoming underweight, but the absolute weight of tech in Korea and Taiwan has increased, so it has drifted higher.”

Sacks remains constructive on the AI supply chain, as there are a lot of small-caps that are even more geared towards advanced manufacturing.

“TSMC is a big beast but you have [smaller] businesses where the revenue base is coming from zero and that business is growing very fast.”

Having taken profits on his biggest winners, Sacks rotated into other tech names further down the supply chain: advanced packaging, liquid cooling and semiconductor testing companies where expectations remain lower relative to what the businesses can deliver: “We've cut a few things early, but we've rotated into things that have also done very well.”

The harder question is whether any of that concentration is warranted by what comes next. Sacks is reasonably confident on capex through this year and into 2027 but uncertain thereafter.

“The discussion is now more around 2028,” he said. “I don't think they can sustain this level of capex, unless you see a very significant change in how these companies are monetising AI.”

Beyond the AI supply chain, Sacks came back from a recent Korea visit with two other themes. One is the disruption China's manufacturers are starting to cause in areas the Koreans considered secure, including semiconductor testing equipment, where Chinese domestic producers are taking share. Memory chip manufacturing could follow, though Sacks put that several years out.

The other is K-beauty: a cluster of smaller cosmetics and skincare companies with export momentum into Western markets, ranging from original design manufacturers to distributors aggregating hundreds of indie brands.

He also flagged shipbuilding as an area where Korean companies are now fielding orders related to AI data centre infrastructure, including floating data centres.

Vietnam is where Sacks is most positive on a valuation basis, while India remains attractive on growth but the entry price is a hurdle.

Indonesia and the Philippines face more consumer pressure, while Vietnam, by contrast, has a current account surplus, a strong export base and a government growth target of 8% – ambitious, he conceded, but the earnings from the companies on the ground have not contradicted it.

The fund's India weighting sits at around 18%, above the roughly 10 to 11% allocation in the large-cap benchmark, which Sacks cited as one of the ways Aberdeen Asia Focus diverges from a passive allocation to the region.