Although deemed the all-weather investment option, absolute return funds should not have to prove their worth by performing well in the coronavirus sell-off, according to Suhail Shaikh, chief investment officer at Fulcrum Asset Management.

Absolute return strategies aim to deliver positive returns, regardless of the market environment by making use of the investment strategies and vehicles available to them.

But this has been difficult for the strategies in the post-global financial crisis, liquidity-fuelled bull market that has seen equities surge.

Indeed, absolute return funds have taken a significant reputational and performance hit in conditions that have favoured long-equity strategies, despite not being expected to outperform those strategies.

Nevertheless, it has been a hard decade or so to make the case for holding the strategies, something Fulcrum’s Shaikh agrees with.

But with the spread of Covid-19 causing governments to go into lockdown and slam the brakes on the global economy and equity markets going through one of the biggest sell-offs on record, some might expect this to be the ideal time for absolute return strategies to flourish.

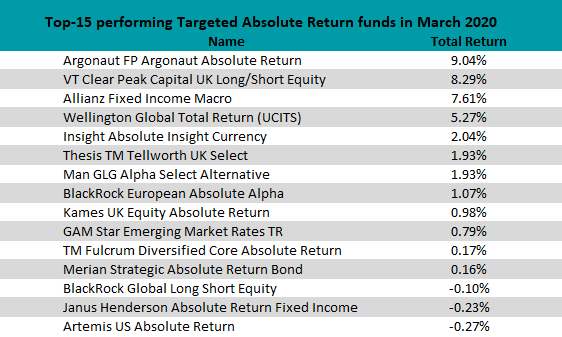

Yet in March only 12 absolute return funds made a positive return from a total of 119.

Source: FE Analytics

However, it is a mistake to judge the worth of targeted absolute return strategies over just one very bad month for markets, said Shaikh – who manages the £173.8m TM Fulcrum Diversified Core Absolute Return fund, one of the few who did make a positive return in March.

The TM Fulcrum Diversified Core Absolute Return fund has around 15-20 different investment ideas per year and, ahead of the Covid-19 crisis, had invested in four: dividend futures, thematic equity investing, volatility trading, and the fiscal spending trade.

“Our fund did make money in March 2020 and I think that’s fantastic but if all you’re looking for is making money when everything else goes direly and badly wrong then it becomes very difficult to make money over the long term,” said Shaikh (pictured). “I could very easily design a fund that makes money every time the stock market drops off, but the hard part is making an [absolute return] strategy for all those hard months when the stock markets go up.

“And I think that the absolute return vehicle and sector should be judged on, ideally, the longer period over three years or five years.”

The idea of just picking random days that equities are down and expecting absolute return funds to have outperformed is wrong, he explained, because that isn’t the outlook you take when investing.

“The reality is that over the last three years – let’s say 2017-19 – to say that over that period absolute returns as a broad industry did not deliver, I think that’s more or less fact,” he said. “And I think that that’s a credible thing to say.

“But, if you then do what many people have done and dump all those absolute return funds and put it all into equities, guess what? You just experienced a 30 per cent loss.”

Shaikh said another important point to consider is that whilst equities have been a strong performing asset class, to get the full return on them you have to have held them from when they last bottomed out to their peak and never panicked. Something, he pointed out, most investors wouldn’t have done.

“In reality you start at £100 and end up at £200 but on route you’ve gone to £50 twice, and a lot of people would fall off the wagon at £50 or £60 and say ‘I can’t take this’ because they don’t know that it’s going to £200 and they think it could be falling down to zero,” he said.

“So controlling that volatility is very important and it’s all good and well to say ‘well equities went up 10 per cent per year over 10 years’, but the question is really, ‘would you have had the stomach to own them through that journey and experience that or not?’

“And that’s the kind of fact that absolute returns and any strategy should be measured against, is the reality of what people have done.”

Rather than focus on the March 2020 sell-off as a standalone event, the TM Fulcrum Diversified Core Absolute Return manager said investors should be looking at how absolute returns perform over the next three years – not the usual rolling three years absolute returns are measured on but 2020-2023.

This is because, according to Shaikh, the coming three years will prove how valuable the strategy is as equities should be too expensive to justify strong returns.

“When you have a 10-year equity bull markets that just keeps going up in a straight line, it’s very challenging to have absolute return [strategies] in your portfolio,” he said “But we need these sorts of episodes to remind people as to why they have absolute return [in their portfolios].

“I think that will bode well for us and others in this space for the next three-to-five years, because the bottom line is that equities are now actually more expensive than they were three months ago when prices were higher,” Shaikh said.

With equity markets falling by over 30 per cent in the sell-off even with the recent rally they’re still down compared to their mid-February peaks.

And with earnings drastically down, Shaikh said it will be a tough few years for equity markets with volatility likely higher as the full impact of the crisis becomes clear.

“I think that we can compete with that,” the Fulcrum investment chief said. “And I think that we can generate higher returns with much lower volatility in the absolute return sector.”

Performance of fund vs sector over 3yrs

Source: FE Analytics

The TM Fulcrum Diversified Core Absolute Return fund has made a total return of 5.34 per cent compared with a 0.8 per cent loss for the average IA Targeted Absolute Return. fund. Although it should be noted that the sector is home to a wide range of strategies. The fund has an ongoing charges figure (OCF) of 0.85 per cent.