There are just three ways for a long-only investor to permanently lose money – and if they fully understand and protect against these risks, it is actually quite difficult to end up out of pocket.

This is according to Richard Stutley (pictured), portfolio manager at MGIM (Momentum Global Investment Management), who says these factors – counterparty risk, high leverage and illiquidity – crop up again and again when you look back through the history of people who have suffered a permanent impairment of capital.

Counterparty risk is the most obvious of these – a counterparty is whoever holds your money, be it an individual, company, fund or country and there is always a possibility they may renege on their commitment.

Yet while it is impossible to make any sort of investment without a counterparty, Stutley said it is easy to protect against this risk through reducing the concentration of your portfolio.

“It only becomes a risk when investors have too much exposure to one counterparty,” he explained.

“The reason you should be exposed to more than one counterparty is that it is very hard to know everything about that individual or company, no matter how much analysis you do.

“Things can go wrong for a variety of reasons. It may be fraud: while you are smart and diligent, so are the people working against you, be they the board of Enron (the company’s true performance was hidden from investors thanks to fraudulent record keeping) or Barings Bank’s Nick Leeson (Leeson managed to conceal the extent of his losses from his bosses, which mounted exponentially as he sought to double-down on his losing positions).

“Times change, oversight becomes stricter, but that didn’t prevent Wirecard’s implosion in June this year.”

Even carrying out your own thorough due diligence by looking under the bonnet of an investment may not be enough to protect you. Stutley pointed to the example of the Allied Crude Vegetable Oil Refining Corp back in the 1960s: even though inspectors checked its tanks for vegetable oil, they didn’t realise they were filled with water covered by a thin layer of oil that floated on top.

Often the reason why a counterparty reneges on its obligation is much more mundane – things simply didn’t work out as planned.

Of course, the obvious way to avoid this risk is to diversify: entrust your money to a number of different counterparties so you won’t face ruin if one doesn’t pay it back. It is also a good idea to evaluate how much residual value there is in your investment if things go wrong.

“Like other investors, you may not have been able to spot that Charles Ponzi’s original strategy – buying postal reply coupons in one market for a lower price than he could sell them in another one – was no longer viable and that he was paying existing investors (and himself) out of money received from new investors,” Stutley continued.

“But you could have looked at the strategy and realised that the only assets in the venture, and hence the only residual value, was inventory – the postal coupons themselves. There were no durable assets that could be repurposed should things not work out.”

Moving on, the manager said the next two risks – leverage and liquidity – are ultimately about the same thing: being forced out of your investment and into cash at a poor price.

Asset prices display excess volatility which means they overreact to new information. Often this overreaction sees asset prices fall significantly below fair value. While these instances of mispricing typically resolve themselves in time, meaning investors ultimately only suffer a loss on paper, Stutley said the danger is they are forced to sell at these depressed prices and therefore do not participate in the asset’s subsequent recovery.

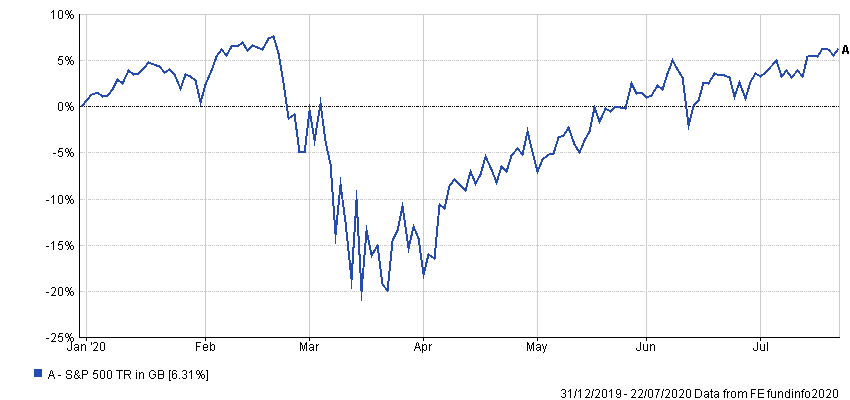

“For example, an investor in the S&P 500 index would have lost 20 per cent of their stake from the start of 2020 if they had been forced to sell at the end of March; that same investor would have instead made 1 per cent if they had been able to hold on to their assets another three months until the middle of July,” he added.

Performance of index in 2020

Source: FE Analytics

“Leverage means debt and debt must be serviced regularly and eventually repaid.”

“These obligations can often only be satisfied by selling assets. Hence leverage may come at a greater cost than simply the interest charge on the borrowing, if it precipitates a fire sale.”

Liquidity means the availability of cash and Stutley said that as anyone who has tried to hire a builder will tell you, “cash is king”.

He added that the golden rule with liquidity is never to need it – avoid the situation where you have to sell an asset to meet a payment.

“Liquidity is difficult to manage for two reasons,” he explained. “Firstly, no matter how closely you try to align your assets and your liabilities, conditions are always changing; events this year are testament to that fact.

“Secondly, liquidity can disappear suddenly. There are more assets in the world than cash to pay for them and hence whenever there is high demand for cash, asset prices usually end up falling to attract this scarce cash.”

Despite these challenges, Stutley said there are still prudent steps investors can take to manage their liquidity.

Most importantly, they need to work out how long it takes for transactions involving their assets to complete as well as the size of the average transaction. They shouldn’t expect to be able to sell an asset more quickly or in greater size than the average deal without offering a discount.

“In sum, history shows that appropriate diversification is the first step to protecting one’s wealth,” the manager continued.

“Try and minimise the chances of being forced out of one’s assets and into cash, due to excessive leverage or else liquidity needs.

“Taking note of these lessons from history is not guaranteed to safeguard investors’ wealth, but it may prevent them from losing money in some of the more common ways.”