Emerging-market bonds are becoming increasingly attractive to investors, supported by stronger valuations, healthier volatility‑adjusted yields and more stable fundamentals than many developed market peers, according to bond managers at M&G.

Eva Sun-Wai, manager of M&G Global Government Bond, said: “When you consider the news flow in 2025 and how much was in the headlines about [US president Donald] Trump, trade wars and geopolitics, if you were to position for a market where you expected very high volatility, you would probably be long long-end government bonds – hoping duration would protect you – and long the US dollar.”

She noted an investor may have also chosen to be underweight risk markets and underweight spreads, yet “none of those trades would have worked last year”.

Instead, Sun-Wai said investors would have fared better in emerging markets last year, noting she has seen “pockets of value creep up in certain markets”.

“Anything euro-linked or Latin American – like Brazil and Mexico – had a very good year,” she said.

“But there are also domestically driven stories, like South Africa, which has rallied strongly and continues to rally. And then there are areas like Chile and other emerging markets getting terms-of-trade boosts from commodities.”

Part of this performance was driven by resilience, with emerging market exports remaining relatively strong despite the headwinds from US trade tariffs, panellists agreed.

“Emerging markets – especially local – look structurally strong to us,” Sun-Wai said. “Even if the dollar strengthens, there is enough divergence and enough pockets of value that you can still see a market that maintains its momentum this year.”

They also argued the gap between the quality and appeal of emerging market versus developed market debt is narrowing, with the distinctions between the two becoming blurrier.

According to Richard Woolnough, manager of M&G Optimal Income, Corporate Bond and Strategic Corporate Bond, this is partly down to responses to the Covid-19 pandemic.

“Emerging markets couldn’t afford to keep people at home, which meant emerging markets didn’t have as much money printing or inflation – their currencies were subsequently stronger and central banks had less work to do,” he said.

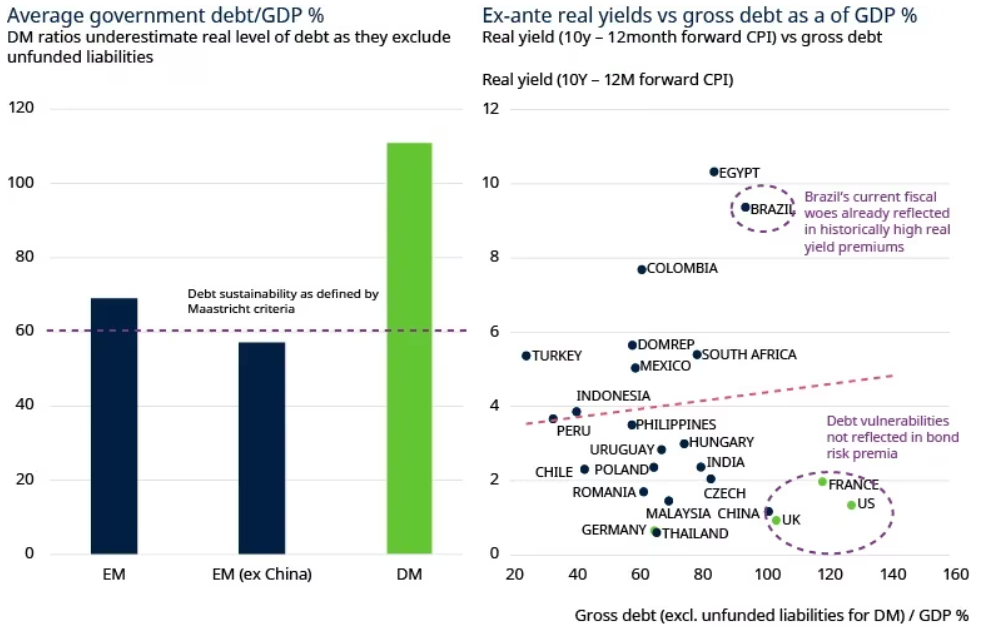

Research from the Schroders fixed income team also revealed a more favourable inflation outlook for emerging markets. As such, the team said that real rates across emerging markets remain “unnecessarily too high”, with 10-year local government bond yields offering value.

“This appeal is reinforced by more favourable public-sector debt dynamics in emerging markets, especially when compared with their developed markets counterparts,” Schroders said.

Emerging market vs developed market debt dynamics and real yields

Source: Schroders, IMF, as of September 2025

The research added that this favourable outlook – particularly for local currency emerging market segments – could be boosted further should the US dollar continue the cyclical downturn initiated last year.

As such, Schroders continues to favour markets such as Brazil, Mexico, South Africa, India and parts of central Europe.

However, it is not only inflation management that recommends emerging markets to bond managers, Sun-Wai maintained.

When assessing the credibility and quality of a region’s debt market, managers often look to governance indicators measured by the likes of the International Monetary Fund.

“In many of these metrics, developed markets are being outscored,” said Sun-Wai. “Croatia and Cyprus outscore Spain, and Uruguay outperforms the US in some cases.”

She added that it is important for investors to look at volatility-adjusted carry and volatility-adjusted yield.

“When you factor in fiscal risk, the ability of these central banks to bring inflation under control and what that means for your real yield outlook, you are actually seeing a very healthy volatility-adjusted picture in emerging markets which corresponds with increased volatility in developed markets.”