BlackRock's MyMap fund range has trimmed equity exposure by around 1% and cut its longstanding gold position last month but the manager remains overweight risk, arguing that stretched valuations are not concerning enough to de-risk fully when no recession looms.

Chris Ellis-Thomas, manager on the multi-asset range, said the modest reduction was driven by caution over US market valuations but stressed the funds remain constructive on growth.

“We don't think a valuation reset comes about in a vacuum,” he said. “Markets don't just reset without stress, probably a recession or an earnings downturn, which we don't forecast now.”

The portfolio changes reflect the fund's outlook for 2026, built around three themes: navigating risks, earnings taking the helm and minding the debt iceberg. In practice, that has meant staying overweight equities while moderating exposure slightly.

“On risk, we took a small amount of equity risk off the table but stayed at positive risk overall,” Ellis-Thomas said. “The simplest way to think about it is a scale from plus 2 to minus 2. We went from slightly above plus 1 to slightly below plus 1.”

The range has been overweight equities for a couple of years on the view that the economy remains sound. “We're still positive on risk because we think the economy is fine. We don't see an elevated chance of recession and haven't for a while.”

The US economy likely troughed in the fourth quarter of last year, he argues, and should reaccelerate through 2026, though only back to trend growth. That backdrop, combined with expectations that political noise around tariffs will fade and interest rates will move lower, supports an “earnings taking the helm” view.

“This upswing in growth through the year will play out through corporate earnings,” Ellis-Thomas said.

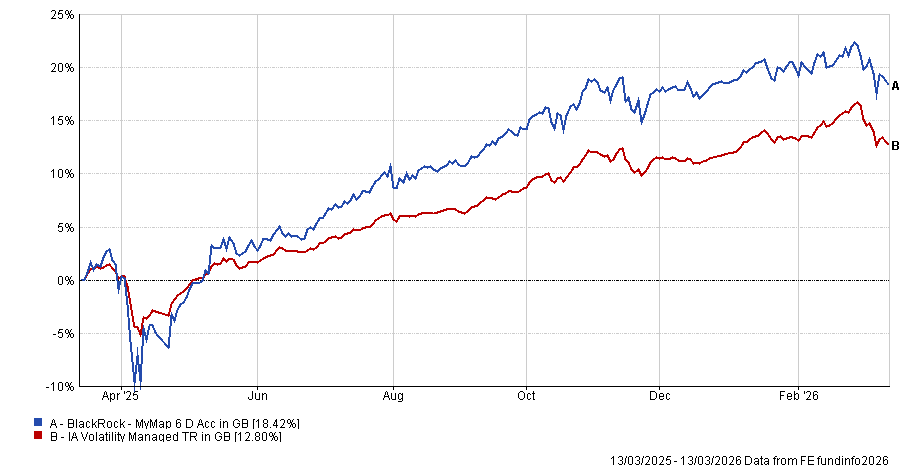

Performance of fund against index and sector over 1yr

Source: FE Analytics

US and emerging markets favoured

Regionally, the range has maintained its tilt towards the US and emerging markets while pulling back from Europe. Ellis-Thomas sees profit resilience in America driven in part by its dominance in AI.

“In the US, we see profit resilience and a continuation of the US being dominant in the majority of the things that feed into AI, which means a much higher likelihood of profit resilience and profit growth there,” he said.

Growth in Europe has recovered but not to the levels expected in the US. “Valuations are not so compelling in Europe that there would be any rationale for us to lean into that.”

Europe outperformed strongly in 2025 but the European rally was driven by specific factors around fiscal policy and interest rates rather than broad-based strength, he noted.

“This year, where we see recovery and growth coming through is mainly in the US. There hasn't been enough change in Europe for us to pivot,” he said.

The funds maintain a slight overweight to UK equities, though Ellis-Thomas noted the FTSE 100's drivers are global rather than domestic, making them “much more related to global growth and the dollar”.

Emerging markets have become less China-focused over recent years and now offer multiple tailwinds, including a weaker dollar, industrial metals prices and other factors supporting exporting parts of the market. In addition, stocks have a “much better valuation starting point than developed markets”.

Gold trimmed, bonds underweight

The fund's gold position was trimmed at the end of last year from 3.5% to 2%. The rationale for holding gold remains intact, Ellis-Thomas said, but the rapid price appreciation warranted taking profit.

“We thought, and still think, the longer-term drivers for gold probably remain in place, but it had run so hard that taking some risk off the table was merited,” said Ellis-Thomas.

Gold's role has evolved since MyMap launched in 2019. “Since bond yields have recovered, its role has pivoted slightly. It's still less correlated to equities and bonds, but there's also a narrative around de-dollarisation and central banks expanding what they hold on their balance sheets, he said.

That trend is likely to continue, he argued, though the pace of future gains is uncertain.

Elsewhere, MyMap has maintained a longstanding underweight to government bonds, driven by concerns that markets have yet to price in fiscal risks.

“We don't think markets yet price the risk associated with fiscal policy, particularly in the US,” Ellis-Thomas said. “There is a large amount of debt required to fund the fiscal trajectory under the current administration and the previous administration's plans.”

While bond yields have become more attractive, he remains cautious. “US Treasuries may not be seen as the same safe haven as in the past and market participants will likely demand a higher risk premium over the long term related to fiscal dynamics,” he said.

The fund has found better value in emerging market local currency debt, which benefits from a weaker dollar and more prudent central bank behaviour.