Currency decisions have become critical to portfolio returns in a way they haven't been for years, according to Vincent Mortier, chief investment officer at Amundi.

“You can be right on a macro view but you can destroy all the performance through the currency,” he said. “We saw this last year. The performance of securities in euro or sterling terms is not the same as in US dollar terms.”

Mortier's warning comes as diverging monetary policies and what he calls a “big debasement at play in the world” create wider currency swings than investors faced during the low-rate era. The challenge is particularly acute for investors building positions in Asia, where the opportunities are spread across markets with very different currency dynamics.

“Currencies are more important in a portfolio, and it's a competition of the weakest countries,” Mortier said. He expects the US dollar to remain sustained by America's high deficit spending and the need for yields to stay attractive to foreign buyers. Emerging market currencies, by contrast, should strengthen as their more orthodox monetary policies look increasingly appealing.

The renminbi has already strengthened recently and should continue, while the yen is also attractive after being too heavily shorted. The euro sits in between, though Mortier expects it to strengthen as well. For the first time in 30 years, he said, Amundi is starting to like Japanese government bonds, which are becoming more attractive for domestic investors.

That currency backdrop shapes how Amundi is positioning across Asian markets. Mortier pointed out that current benchmarks make little sense for investors seeking growth. The MSCI All Countries index is 65% US, with just 3% in China and 3% in India.

“If you are a retail investor, it doesn't make sense. You have only 6% in India plus China. I don't believe it is accurate,” he said.

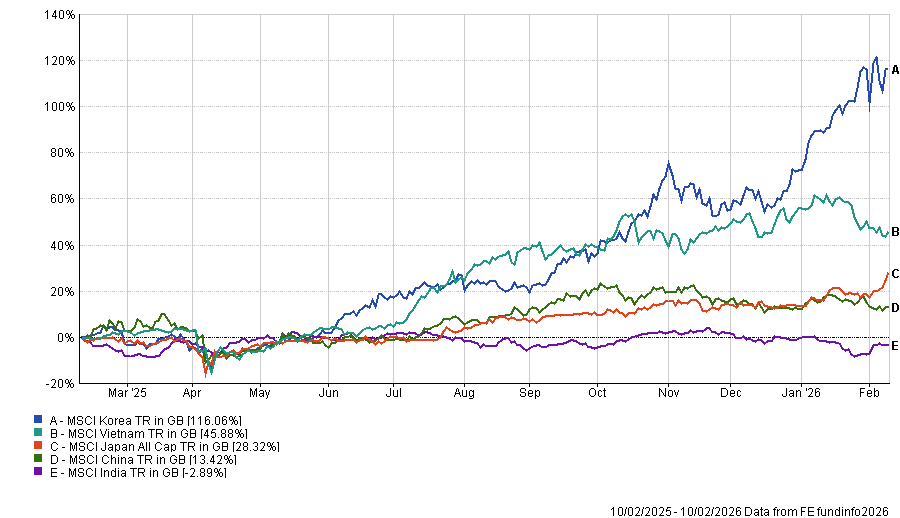

Where the opportunities are

Korea was last year's standout performer, driven by earnings upgrades in semiconductors and other sectors where the country has strength, such as nuclear power, transformers for the US power grid and shipping.

But according to Ji Park, senior emerging market equities manager at Amundi, the more interesting story for 2026 is the government's value-up programme – a push for better corporate governance and capital allocation.

Performance of fund against index and sector over 1yr

Source: FE Analytics

“In 2024, Korea was the cheapest market. There was a lot that was quite negative about the market. At that point, the president was kind of on his way to impeachment, so the valuations were really depressed,” Park said. “No one would have forecasted that 2025 would have been such a great year for Korea but this new current government is really focused on value-up.”

She expects earnings to remain strong and performance to continue as the policy gains momentum.

Meanwhile, Claire Huang, senior emerging market macro strategist at the firm, described Japan as a “posterchild in Asia of the rising middle power” under the newly elected Sanae Takaichi.

The timing for fiscal expansion has never been better. A decade ago, the IMF orthodoxy of fiscal consolidation would have made such policies difficult. Now, geopolitically, higher defence spending is not only acceptable but expected. Germany's shift at the February 2025 Munich security conference signalled that fiscal austerity is being rethought across developed markets.

“Takaichi is doing fiscal expansion when timing is really tailing for her and when Japan has the strongest government balance sheet right now,” Huang said.

In China, markets are “bifurcated”, according to Park, with strong exports and industrial production sitting alongside weak domestic demand.

Yet the market has decoupled from this macro reality. Chinese equities performed very well last year, driven partly by the DeepSeek effect in January and partly by a reduction in geopolitical risk premium as investors compared Chinese policymakers favourably to the Trump administration.

Here, the opportunity is stock-specific. Park highlighted technology, materials, healthcare and financials as sectors where the firm is positive.

“In China, there will be very much a domestic tech market that doesn't really service the US or any other market. It's very much geared to helping the domestic economy,” she said.

As for the other emerging market heavyweight, India, it underperformed last year, held back by tariff concerns and an index composition overweight in sectors being disrupted by AI. But valuations now look more attractive.

“There are a lot of companies that are very well managed. They do care about capitalisation. They do care about the long-term structure of their businesses,” Park said. With tariff issues behind the market, she expects consistent, resilient earnings growth.

Vietnam, meanwhile, is being overlooked despite offering what Park described as a very exciting opportunity. The country has just gone through a political transition and implemented reforms that should support longer-term growth. She likes exposure to the growing middle class through consumer stocks and financials.