A £10,000 pay rise should be cause for celebration. But for working parents earning around £100,000, it can trigger a tax bill that wipes out the entire increase – and then some.

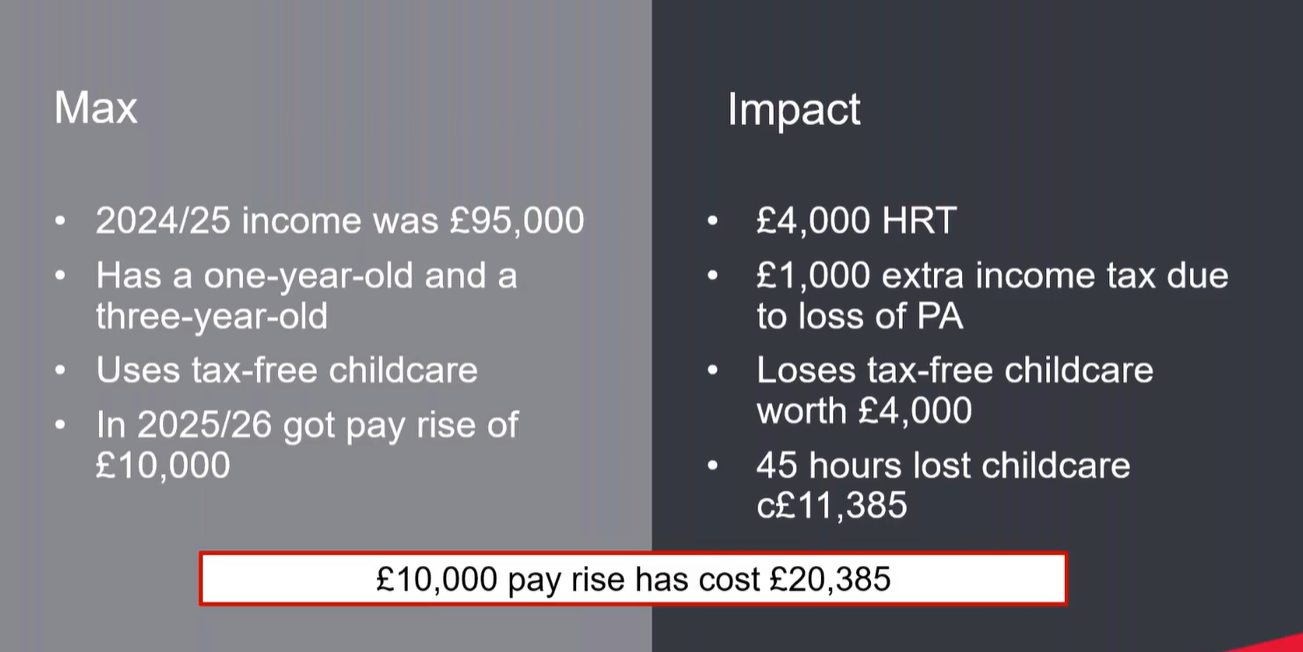

Lisa Webster, senior technical consultant at AJ Bell, used an example case study to illustrate the problem. ‘Max’ has a one-year-old and a three-year-old child. His partner also works. In the 2024/25 tax year, he earned £95,000 and this tax year, he receives a £10,000 pay rise, taking his salary to £105,000.

It sounds great, but there are costs. As a higher rate taxpayer, Max now pays £4,000 extra income tax on the raise. But this is not all.

As £5,000 of the raise pushes him over the £100,000 threshold, he will begin to lose his personal allowance at a rate of £1 for every £2 earned above that level, costing him another £1,000 in tax.

But the real damage comes from childcare. Crossing £100,000 means Max loses entitlement to tax-free childcare, which had been providing a £2,000 government top-up per child – a £4,000 loss.

He also loses 45 hours of government-funded childcare per week. Based on survey data from childcare charity Coram, that works out at approximately £11,385 per year.

“Having a £10,000 pay rise has cost him £20,385,” Webster said. “We talk about the 60% tax rate, but for working parents it can be significantly worse.”

Source: AJ Bell

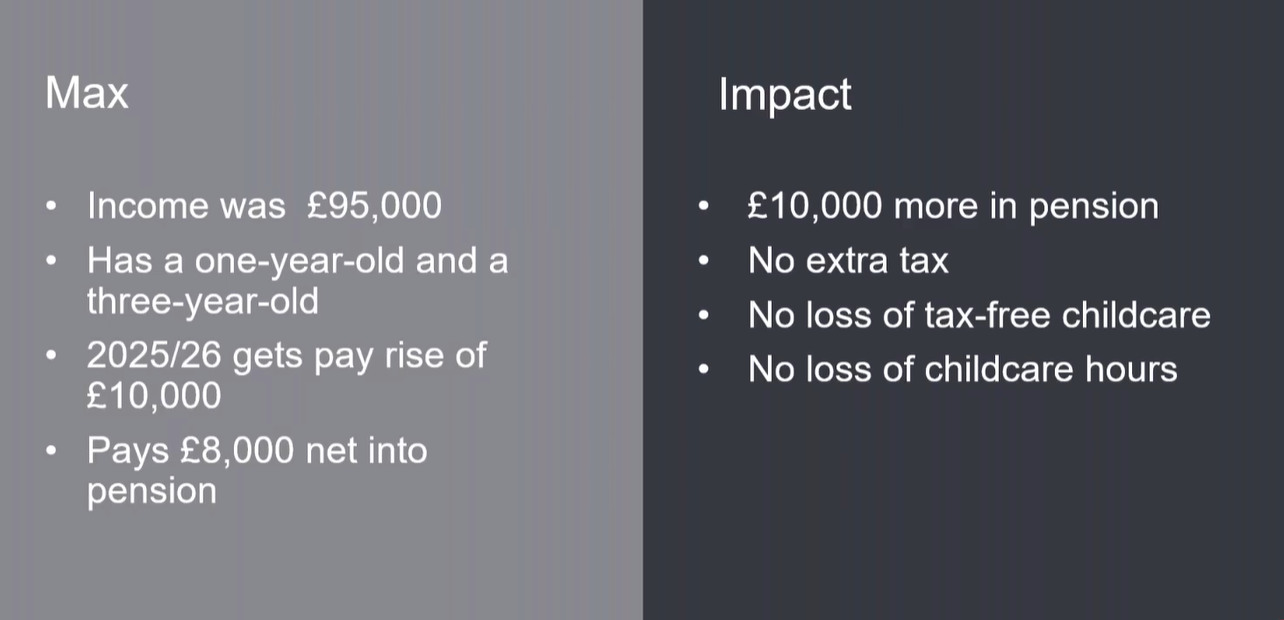

The solution, she argues, is a pension contribution. If Max pays £8,000 net into his pension, he receives £10,000 gross after basic rate relief at source. The additional 20% higher rate relief is reclaimed via his tax return, effectively cancelling out the extra tax he would have paid. More importantly, his net income drops back below £100,000, preserving both tax-free childcare and the funded childcare hours.

“This is a clear example where you want to get income below £100,000,” Webster said. “It shows how important it is to get those contributions in, particularly for people with fluctuating income who might not have known earlier in the year.”

Source: AJ Bell

Other pinch points

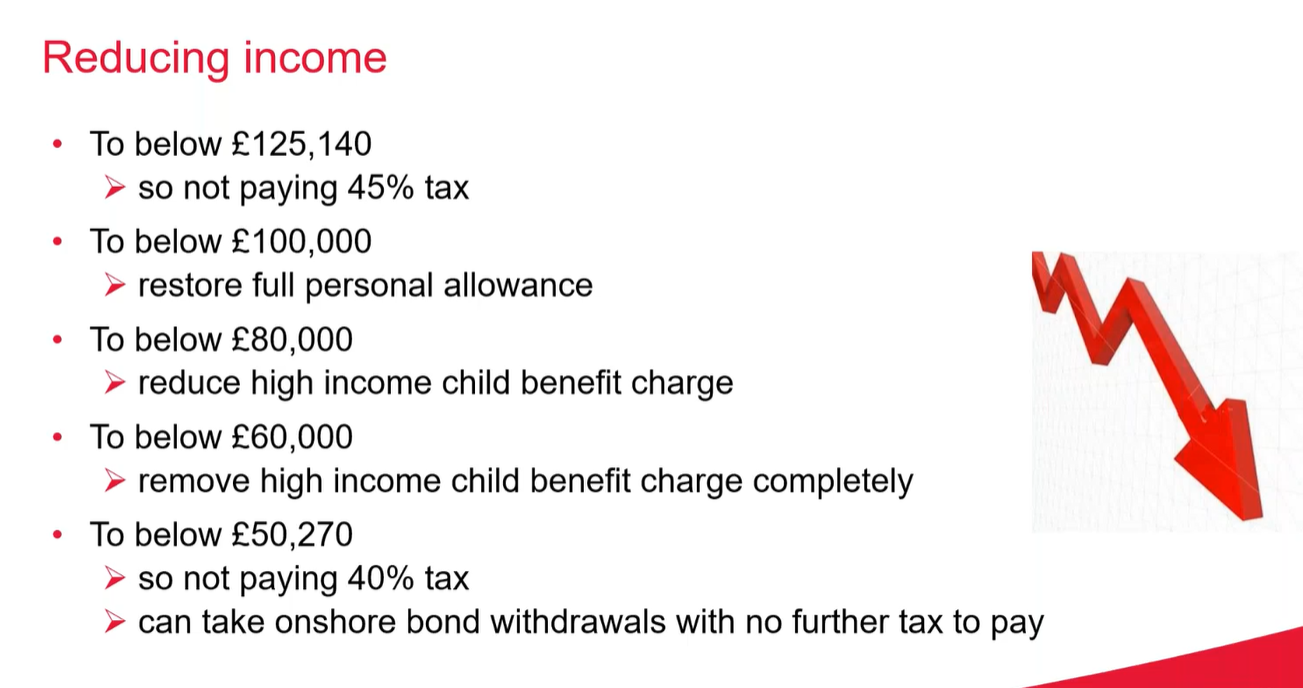

The £100,000 trap is not the only threshold where pension contributions can deliver outsized benefits. Webster highlighted several others worth considering before the tax year ends on 5 April.

For those earning above £125,140, reducing income below that level not only avoids the 45% additional rate but also restores the £500 personal savings allowance, which disappears for additional-rate taxpayers.

Parents with income between £60,000 and £80,000 face the high-income child benefit charge, which claws back child benefit at a rate of 1% for every £200 earned above £60,000. Reducing income below £60,000 eliminates the charge entirely.

Dropping below £50,270 moves a taxpayer from the higher rate to the basic rate, restoring the £1,000 personal savings allowance. It also means onshore bond withdrawals are no longer subject to further tax, provided income remains below that threshold.

“There are lots of pinch points where reducing income can be even more beneficial,” Webster said – illustrated in the figure below.

Source: AJ Bell

Personal pension contributions attract full tax relief for relevant UK individuals, which includes anyone with UK earnings such as salary, bonuses, commission or self-employed income. It also includes UK residents, Crown employees serving abroad and their spouses, and individuals who have left the UK within the past five years.

Contributions must be made before age 75 to qualify for tax relief, however, and the maximum annual contribution eligible for relief is the higher of relevant UK earnings or £3,600 gross (£2,880 net after basic rate relief at source). The £3,600 limit applies even to non-working spouses and children.

Crucially, the amount that can be contributed with tax relief in any given year is capped at 100% of earnings in that tax year. Unused annual allowance can be carried forward for three years, but carry forward does not override the earnings limit.

The standard annual allowance is £60,000, though this can be reduced to £10,000 for those who have already taken taxable income from a defined contribution pension (the money purchase annual allowance), or tapered down to as low as £10,000 for those with adjusted income above £360,000.

Tax year-end considerations

Webster stressed that pension contributions are particularly valuable for those with fluctuating income like the self-employed, but even for employees who, if they get bonuses, might not know exactly what they're going to earn.

By the time the tax year draws to a close, the picture becomes clearer – and so do the opportunities to mitigate tax through pension contributions.

She also pointed to the compounding benefit of getting money into a pension wrapper early. “Once your money is in your pension, you then get compound tax-free growth, so no income tax to pay and no CGT [capital gains tax] to pay,” Webster concluded.