Emerging markets are known for their sharp swings, which makes a strong long-term track record all the more impressive.

But even the long-term outperformers across the IA Global Emerging Markets, IA Asia Pacific ex Japan and IA China/Greater China sectors can experience a challenging year, whether due to cyclical positioning, market-specific headwinds or geographical weightings.

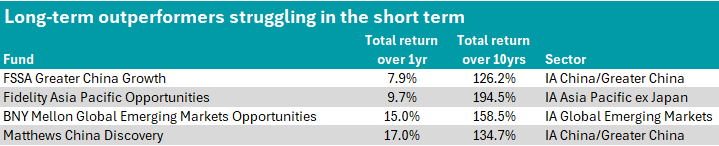

This was the reality for four funds across these sectors. As shown in the table below, that delivered top-quartile returns over 10 years but slipped to the bottom quartile in 2025.

Source: FE Analytics

The largest of the four funds with £890.5m under management is Fidelity Asia Pacific Opportunities, which logged a fourth-quartile return in the IA Asia Pacific ex Japan sector of 9.7% in 2025. The fund’s long-term and high-conviction approach has resulted in the strongest 10-year return of the four funds, delivering 194.5%.

Its year-to-year return record over the assessed 10-year period has largely been consistent, maintaining first or second quartile returns – albeit with a brief dip into the third quartile in 2022 with a 11.5% loss. It has been in the fourth quartile for returns since 2024, however, gaining 3.1% versus the 10% sector average.

FE fundinfo Alpha Manager Anthony Srom, who has managed the fund throughout the past decade, employs a bottom-up approach, selecting between 25 to 35 stocks.

FundCalibre analysts said Srom’s track record of minimising volatility is “impressive”, adding that his “high-conviction and disciplined approach helps this fund to stand out from its peers”.

Notably, Fidelity Asia Pacific Opportunities is overweight markets which struggled in 2025 – specifically, it has a 33.1% weighting to China versus the 26.5% weighting in the MSCI All County Asia Pacific ex-Japan index and a 13.8% allocation to India versus 13.3%.

In contrast, the fund is significantly underweight South Korea – at 3.2% versus 15.6% – missing out on the region’s strong 2025 performance as a beneficiary of the AI boom.

RSMR analysts noted that the manager’s high conviction approach and contrarian outlook does mean there can be periods in which the fund underperforms and so is better suited as a satellite holding unless investors are “willing to exercise a degree of patience and can weather returns that might not track those of the benchmark over the short term”.

Meanwhile, the £447.7m benchmark-agnostic FSSA Greater China Growth had the weakest return in 2025 of all funds in the IA China/Greater China sector, gaining 7.9% over the year. The next weakest return in the sector was managed by Comgest Growth China, which gained 10%.

FSSA Greater China Growth typically holds between 40 to 80 stocks, with its strong quality-growth bias reflected in the largest positions – TSMC (9.8%), Tencent (8.7%) and Huazhu Group (4.1%). It also demonstrates a strong focus on technology, with more than a quarter of assets allocated to the information technology sector.

RSMR analysts noted that the fund “tends to lag a cyclical risk-on market environment where lower-quality stocks perform strongly but outperformance has been demonstrated over the longer term, especially in difficult market conditions”.

However, they maintained the fund is a lower risk option for investors seeking exposure to Chinese equities.

It is managed by long-standing FE fundinfo Alpha Manager Martin Lau and Helen Chen, with the former maintaining his Alpha Manager title since the awards were created in 2009. He remains on the fund, although investors should note that Chen took over leadership on 1 March 2025.

Following review post-management change, Titan Square Mile retained its Responsible ‘AA’ rating for the fund, noting that Chen has demonstrated strong expertise and leadership, while Lau’s continued involvement ensures continuity and stability in its management.

Matthews China Discovery is another fund in the IA China/Greater China sector featuring in the table, despite making the strongest one-year return of the group. It is also the most expensive, with an OCF of 1.25%.

Renamed from Matthews China Small Companies to Matthews China Discovery in August 2024, the fund has seen its assets contract sharply from $380m in 2023 to $108.3m.

In December 2025, Matthews announced the return of Tiffany Hsiao to the driving seat of the fund – she previously managed the strategy before leaving in 2020. She replaced the prior team of Andrew Mattock, Winnie Chwang, Hardy Zhu and Sherwood Zhang.

So far in 2026 (up to 24 February), the fund has posted a top-quartile return over 21.4% – well ahead of the sector average return (3.8%) and the MSCI China Small Cap index (9.9%) – although this is a very short measurement window.

As of 31 January 2026, the fund leans heavily into areas of structural growth, running significant overweights in information technology at 29.7% versus 12.6% in the benchmark and industrials at 26.3% versus 13.3%.

Finally, BNY Mellon Global Emerging Markets Opportunities delivered a 15% return in 2025 and 158.5% over 10 years.

The fund, which sits in the IA Global Emerging Markets sector, has a long-term objective of compounding capital over five years or more. However, performance has not been without setbacks, as it has suffered losses in multiple years across the assessed period, losing 20% in 2018, 1.5% in 2021 and 14.1% in 2022.

The strategy has experienced relatively high managerial turnover, passing through the hands of Paul Birchenough, Ian Smith and Liliana Castillo Dearth before Alex Khosla took over lead management in May 2025, joined by Aditya Shah as deputy in September 2025.

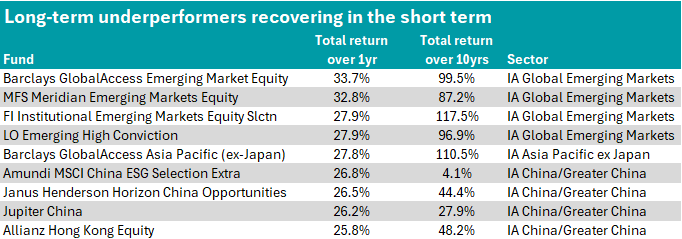

Just as these long-term leaders struggled last year, the opposite was also true for several funds that have historically lagged – including Barclays GlobalAccess Emerging Market Equity, MFS Meridian Emerging Markets Equity and FI Institutional Emerging Markets Equity Slctn.

Source: FE Analytics

As part of this series, Trustnet has also looked at global equity income, the US, Japan, small-caps and multi-asset.