The rise of AI and dominance of technology stocks over the past few years started to abate in 2025, with Rathbones fund manager James Thomson suggesting the signs are there for a significant broadening out in markets this year.

The “concentrated technology story” has come to a head, with investors citing notable fears that some of the largest companies – namely the ‘Magnificent Seven’ stocks – have become overvalued.

However, while he hoped valuation concerns would encourage people to look elsewhere, the Rathbone Global Opportunities fund manager acknowledged that this is “not enough” to dissuade investors.

“You actually need to see many more ingredients in place before you start to see a broader church making a contribution to returns,” he said.

As such, he uses a six-item checklist to see whether markets will indeed broaden out, noting that most, if not all, need to be met for this to be achieved.

Source: Rathbones, Piper Sandler portfolio strategy

The first is improved housing activity, which he noted is a big contributor to economic growth, as it represents most people's largest asset.

“Higher rates and [people on] 30-year mortgages in the United States mean people have been stuck [with] very little transaction activity going on,” the FE fundinfo Alpha Manager said, as they struggle to find mortgage rates akin to their current offers.

“They've got a juicy 30-year deal that they’re on and they don't want to move because they would suddenly go onto a much higher rate in their new home.”

This has slowed the housing market but there are signs this is changing, with mortgage rates starting to dip. While they may not be as cheap as they were before rates began to rise in 2021, they have moved below previously prohibitive “psychological levels”, meaning housing turnover is starting to tick up.

This should help the likes of DIY store Home Depot, a consumer stock he owns in his £3.6bn fund. There is a presumption that the business will not benefit from an improvement in housing activity this year, so any shift will be beneficial.

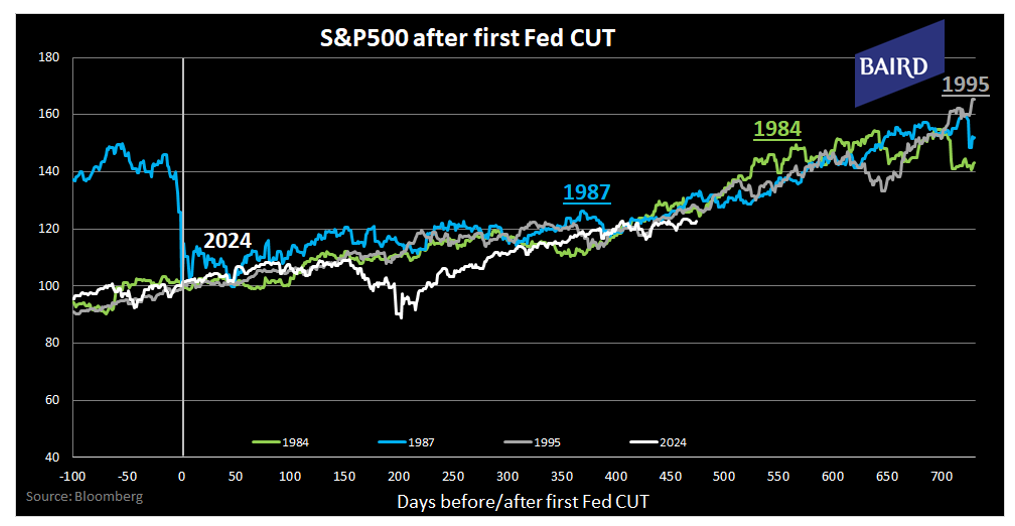

Next is the Federal Reserve easing rates for at least 12 months – something that has now occurred. The US central bank started to cut rates in September 2024, bringing them down from 5.25-5.5% to the current 3.5-3.75% range.

“Often you get Fed easing because they're trying to stave off a recession but in this case there's no recession in sight,” he said, which makes a good time for investors to make money as “historically it's very good for stock markets”.

Source: Rathbones, Baird

“There should be a nice following wind from those rate cuts if we don't get a recession, and I don't think many people are talking about recession risk now – although they certainly were a year ago,” said Thomson.

Next up is money growth, which is the supply of money available. This was improved last year when the Fed announced an end to its quantitative tightening programme.

Tracking M1 (physical money in circulation), M2 (M1 plus savings and money market funds) and M3 (all of the previous plus longer-term deposits and institutional money), he said there is more credit available than there has been in recent years, with banks and private credit proving “generally stimulative” at present.

The fourth factor is that 10-year government bond rates have fallen for 12 months – something that has occurred in the US – while the fifth is a reduction in oil prices, which acts as a consumer bellwether.

“Go to the pump in the United States and gas prices are really low. So that is very stimulative,” he said, as it means more money in people’s pockets to spend.

Although the oil price has risen in recent days after US and Israeli forces conducted coordinated strikes on Iran, killing supreme leader Ali Khamenei, it remains significantly lower than its peak in 2022.

Lastly, fiscal stimulus (or government spending) should increase in the run-up to the mid-term elections later this year, said Thomson, as president Donald Trump tries to “maintain control” of Congress.

“So I think a lot of ingredients are in place for a broadening out trade, whereas historically, even though valuations were telling us that they [non-technology stocks] were cheap, there wasn't anything really to trigger or to get a greater level of participation,” he said.

Which signal is most likely to turn negative?

Although all of Thomson’s parameters for a broadening out trade are currently in place, things can change. The biggest risk to markets is the Federal Reserve, he noted, with nominee Kevin Warsh set to succeed chair Jerome Powell in May.

Markets reacted to his nomination worrying that he could be hawkish, although Thomson described him as a pragmatist and likely to cut rates in line with the president's wishes.

However, the manager noted that the new chair’s hands could be tied if unemployment turns and “any pivot in the rate-cutting cycle would bring this thesis to a crunching halt”.

“If we start to get a boom in employment and the unemployment rate starts to come down, that will make it incrementally harder for the Fed to cut,” said the Rathbone Global Opportunities manager.

Rathbone Global Opportunities fund positioning

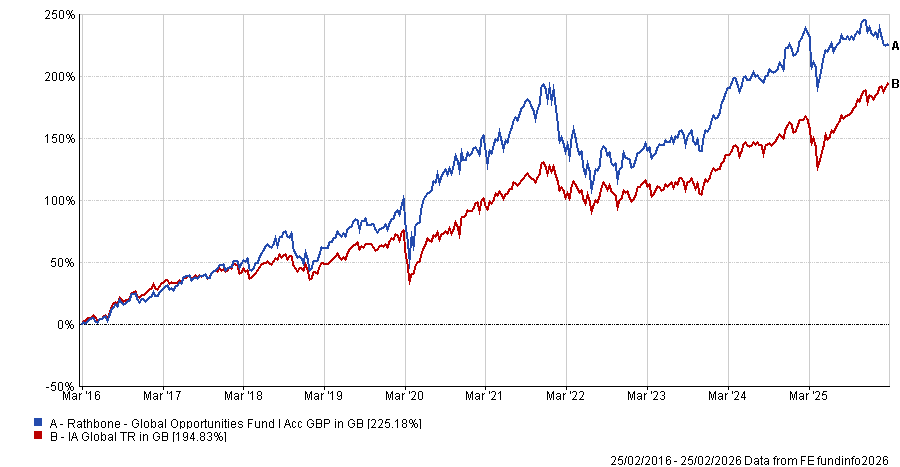

Thomson’s portfolio has struggled in recent years, in particular in 2022 when it lost 20.6%. More recently, it lagged the IA Global sector in 2025, as the fund turned towards its broadening out theme. So far in 2026, returns have not improved, with the portfolio down 2.9%.

Despite five calendar years of top-quartile performance over the past decade, it has slipped to the second quartile of the peer group over 10 years.

Performance of fund vs sector over 10yrs

Source: FE Analytics

“This is an all-weather, balanced and diversified fund and, in the past year, people haven't wanted that. They don't want balance and diversity – they want concentration in a few key themes,” he said.

“And that’s fine when it’s working. But when you get setbacks or a broadening out, you won’t participate, because you have shunned some of the companies that weren’t participating historically.”

His fund is invested in stocks that “ haven't been at the forefront of the bull markets”, with Thomson noting that “a broader, more balanced market would benefit us”.

Consumer discretionary (26%) is the largest sector allocation ahead of technology (19.8%) and industrials (17.7%), with 74.8% invested in the US, 17.2% in Europe and 7% in the UK.