Past performance does not predict future returns. You may get back less than you originally invested. Reference to specific securities is not intended as a recommendation to purchase or sell any investment.

This article is featured in the Q1 2026 Future Strategist newsletter, you can read the rest of the newsletter here.

Global equities: A quarter that rewarded diversification

Source: Bloomberg, as at 31.03.26.

The first quarter of 2026 delivered a significant rotation away from the trends of the last few years. Investors who entered January with portfolios concentrated in US large-cap technology – a positioning that had served them handsomely for a very long time – found themselves on the wrong side of a rotation that was both overdue and significant.

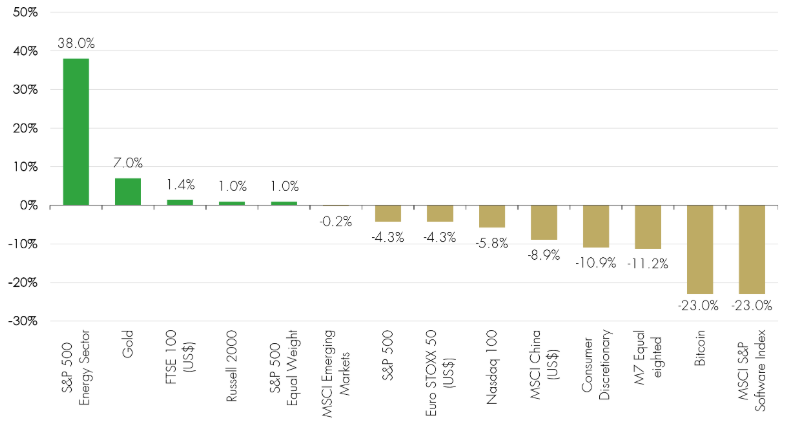

The S&P 500 index fell 4.3% over the quarter, ending a three-quarter winning streak. The Nasdaq 100 fared worse, declining 5.8%, as technology and communication services shed 6.7% and growth stocks as a category lost nearly 10%. Value, by contrast, gained 2.1%, outperforming its growth counterpart in each of the three months.

Headline numbers for US indices concealed significant inter-sector and factor themes below the surface. The equal-weighted S&P 500 index gained approximately 1%, as did the Russell 2000. The index-level decline for the S&P 500 was, in effect, the story of a small number of very large companies having a difficult quarter. This is in contrast to so many periods where the positive drivers have been the small number of mega-cap companies.

In addition to the interplay of large cap with the rest of the market was a very significant change in sentiment towards those companies that may be disrupted by AI. The market has been selling SaaS (Software as a Service) companies under the banner of the AI SaaSpocalypse but this extended into multiple other sectors. The S&P Software index fell 23%, significantly more than the market led by names like Workday -40%, ServiceNow -32%, Adobe -31% and Salesforce -30%. However, the downdraft started to pull in companies in many other sectors like payments, travel and data-rich businesses in the publishing space.

Geographic diversity provides resilience

Outside the US, the picture was more nuanced and, for diversified investors, considerably more logical. International equities finished the quarter with a gain of nearly 1%, outperforming the S&P 500 by roughly five percentage points – the second consecutive quarter of international outperformance.

The MSCI Emerging Markets index declined by a marginal 0.2%, although this flatters the considerable dispersion beneath: Latin America benefited from rising commodity revenues while MSCI China fell 8.9%, weighed down by persistent structural fragility in the property sector.

In Europe, the FTSE 100 index gained 1.4%, a result that owes less to strategic positioning of its constituents than to their heavy exposure to energy and commodities, which happened to be precisely where one wanted to be. The index's long-standing reputation as a repository of unfashionable industries briefly became an asset. The Euro STOXX, lacking such insulation, fell 4.3% in dollar terms. Within European markets, however, Basic Resources surged 18% and Oil & Gas gained 13%.

Oil drove much of the quarter’s dynamics

Airstrikes on Iran and the subsequent closure of the Strait of Hormuz — through which approximately 20% of global oil supply normally passes — sent crude prices surging close to 80% during the quarter; the S&P 500 energy sector returned 38%. The 10-year Treasury yield climbed to 4.32%, its highest since June 2025, as markets repriced the probability of near-term Federal Reserve (Fed) rate cuts towards something approaching zero.

Germany, for its part, offered one of the quarter's quieter but more consequential data points: manufacturing orders rose 7.8% in December and a package of business-friendly fiscal reforms took effect in January. After two consecutive years of contraction, the tentative evidence of stabilisation warrants attention, even if premature enthusiasm has often disappointed before.

The quarter's verdict for investors was straightforward, if uncomfortable: the concentration that drove returns in 2024 and 2025 became the source of underperformance in 2026. We have been making this point since the Liontrust Investment Conference in London in November 2024. Whether this marks a durable regime shift or a temporary correction remains, as ever, the question that markets will continue attempting to answer.

Gold, Bitcoin and the Magnificent 7

Gold (+7.0%) performed its classic role as portfolio stabiliser: not spectacular relative to energy, but decisively ahead of almost every major equity index. Goldman Sachs maintained its year-end target of $5,400 per ounce, citing continued central bank demand and the prospect of further Fed rate cuts later in 2026.

Bitcoin (-23%) had its worst opening quarter since 2018, falling from roughly $88,700 to $66,700 by 31 March – a loss of over $20,000 per coin. In a genuine risk-off environment shaped by geopolitical shock rather than exuberance, Bitcoin correlated downward with equities rather than acting as a hedge. The narrative of digital gold, compelling in calmer times, is definitely receiving a challenge.

The Magnificent 7 (equal-weighted: -11.2%) shed over $2 trillion in market capitalisation from their all-time highs, with every constituent negative for the quarter. This is the first occasion on which that has occurred simultaneously since the AI rally began in January 2023. Microsoft (-21.7%) was the worst performer, with capex commitments in excess of $80 billion prompting investor scrutiny of monetisation timelines for Azure AI. Apple (-6.4%) held up best, its defensive earnings quality and the approaching iPhone 18 cycle providing relative support.

The equal-weighted loss of 11.2% – more than twice the headline S&P 500 decline – underscores how heavily the previous bull market's returns were concentrated in names that, for the first time in several years, the market was unwilling to give the benefit of the doubt to. Dispersion of returns has also become heightened and, therefore, for the first time in many years, making the right choices among the Magnificent 7 has become important.

Read, watch and listen to more insights from Liontrust fund managers here >

KEY RISKS

Past performance does not predict future returns. You may get back less than you originally invested.

We recommend this fund is held long term (minimum period of 5 years). We recommend that you hold this fund as part of a diversified portfolio of investments.

The Funds managed by the Global Equities Team:

-

May hold overseas investments that may carry a higher currency risk. They are valued by reference to their local currency which may move up or down when compared to the currency of a Fund.

-

May encounter liquidity constraints from time to time. The spread between the price you buy and sell shares will reflect the less liquid nature of the underlying holdings.

-

May invest in smaller companies and may invest a small proportion (less than 10%) of the Fund in unlisted securities. There may be liquidity constraints in these securities from time to time, i.e. in certain circumstances, the fund may not be able to sell a position for full value or at all in the short term. This may affect performance and could cause the fund to defer or suspend redemptions of its shares.

-

May have a concentrated portfolio, i.e. hold a limited number of investments or have significant sector or factor exposures. If one of these investments or sectors / factors fall in value this can have a greater impact on the Fund's value than if it held a larger number of investments across a more diversified portfolio.

-

May invest in emerging markets which carries a higher risk than investment in more developed countries. This may result in higher volatility and larger drops in the value of a fund over the short term.

-

Certain countries have a higher risk of the imposition of financial and economic sanctions on them which may have a significant economic impact on any company operating, or based, in these countries and their ability to trade as normal. Any such sanctions may cause the value of the investments in the fund to fall significantly and may result in liquidity issues which could prevent the fund from meeting redemptions.

-

May invest in companies predominantly in a single country which maybe subject to greater political, social and economic risks which could result in greater volatility than investments in more broadly diversified funds.

-

May hold Bonds. Bonds are affected by changes in interest rates and their value and the income they generate can rise or fall as a result; The creditworthiness of a bond issuer may also affect that bond's value. Bonds that produce a higher level of income usually also carry greater risk as such bond issuers may have difficulty in paying their debts. The value of a bond would be significantly affected if the issuer either refused to pay or was unable to pay.

-

May, in certain circumstances, invest in derivatives but it is not intended that their use will materially affect volatility. Derivatives are used to protect against currencies, credit and interest rate moves or for investment purposes. The use of derivatives may create leverage or gearing resulting in potentially greater volatility or fluctuations in the net asset value of the Fund. A relatively small movement in the value of a derivative's underlying investment may have a larger impact, positive or negative, on the value of a fund than if the underlying investment was held instead.

The risks detailed above are reflective of the full range of Funds managed by the Global Equities Team and not all of the risks listed are applicable to each individual Fund. For the risks associated with an individual Fund, please refer to its Key Investor Information Document (KIID)/PRIIP KID.

The issue of units/shares in Liontrust Funds may be subject to an initial charge, which will have an impact on the realisable value of the investment, particularly in the short term. Investments should always be considered as long term.

DISCLAIMER

This material is issued by Liontrust Investment Partners LLP (2 Savoy Court, London WC2R 0EZ), authorised and regulated in the UK by the Financial Conduct Authority (FRN 518552) to undertake regulated investment business.

It should not be construed as advice for investment in any product or security mentioned, an offer to buy or sell units/shares of Funds mentioned, or a solicitation to purchase securities in any company or investment product. Examples of stocks are provided for general information only to demonstrate our investment philosophy. The investment being promoted is for units in a fund, not directly in the underlying assets.

This information and analysis is believed to be accurate at the time of publication, but is subject to change without notice. Whilst care has been taken in compiling the content, no representation or warranty is given, whether express or implied, by Liontrust as to its accuracy or completeness, including for external sources (which may have been used) which have not been verified.

This is a marketing communication. Before making an investment, you should read the relevant Prospectus and the Key Investor Information Document (KIID) and/or PRIIP/KID, which provide full product details including investment charges and risks. These documents can be obtained, free of charge, from www.liontrust.com or direct from Liontrust. If you are not a professional investor please consult a regulated financial adviser regarding the suitability of such an investment for you and your personal circumstances.

Understand common financial words and terms See our glossary