Jupiter Japan Income and Baillie Gifford Japanese Income Growth are two of the favourite options for those seeking exposure to Japanese dividend payers, but there are some key differences between them that investors need to be aware of.

Japanese equity has often been considered by UK-based investors to be a niche and driven by thematic interests such as robotics or Abenomics, but there are a number of reasons to consider the country.

Hawksmoor senior fund manager Daniel Lockyer said: “Japan is worth having exposure to, as we see more and more corporate activity going on and a lot of cheap companies that are likely to pick up with higher dividends, more buybacks, consolidation and M&A activity.”

The country is opening up towards shareholders and becoming more keen to pay out excess cash on the balance sheets, creating more opportunities for income investors. But which funds should they be looking at?

Jupiter Japan Income and Baillie Gifford Japanese Income Growth are quite closely matched funds despite fairly different portfolios. The former has 50% of its weightings allocated to technology and consumer products; the latter has a more differentiated approach.

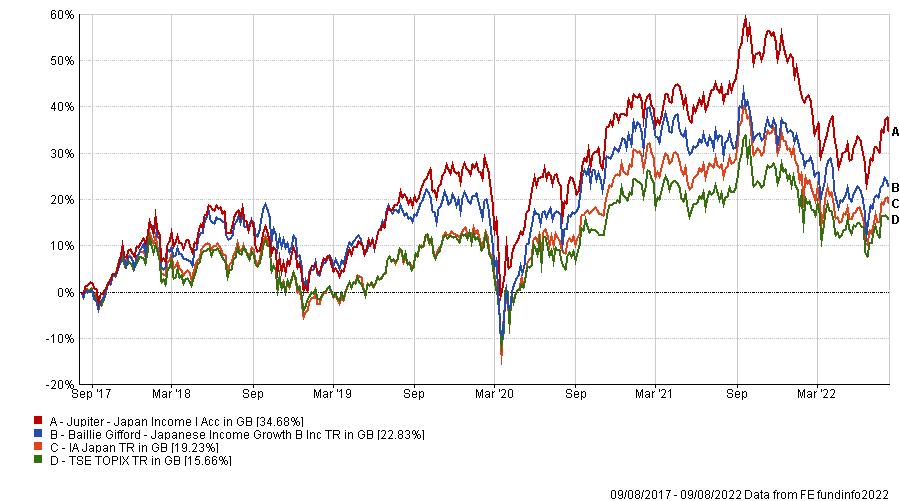

Through different strategies, they both have outperformed their IA Japan peers and the Topix index over the long term. On a five-year horizon, Jupiter Japan Income returned 34.7% and the Baillie Gifford fund made 22.8%, against 18.2% and 15.7% of the sector and index, as shown below.

Trustnet asked three experts which of the two funds finds place in their portfolios, and why.

Performance of funds vs sector and index over 5 yrs

Source: FE Analytics

Andrew Merricks, manager of 8AM Focussed fund, highlighted Baillie Gifford’s “strength in depth across their Japanese equity team, albeit following the group’s growth style bias”, which has struggled more recently.

“But the fund has performed perfectly OK and with over £700m in assets it certainly has its supporters,” he added.

However, Merricks is partial to concentrated investments and preferred the more focussed Jupiter’s fund, with its 38 stocks rather than the 58 of its Baillie Gifford peer.

“Jupiter Japan Income is more concentrated in the consumer discretionary, financials and industrials sectors, which may have contributed to the Jupiter fund’s 5% outperformance of its rival between August and December 2021.”

To the argument that concentration accentuates manager risk, Merricks replied: “That is what one should be investing in an actively managed fund for.

“The fund also appears to offer more consistency and seems to edge performance over most timescales.”

But UK investors shouldn’t be misled by the title ‘income’, he warned.

“By Japanese ‘income’, we are talking around 2%, which might be a tad underwhelming for a traditional UK investor,” he said.

“Baillie Gifford has other Japanese funds, so they needed to differentiate. But with Jupiter, the name choice is slightly more puzzling, as they doesn’t have any other Japan funds to compete with.”

Kelly Prior, investment manager in the multi-manager team at Columbia Threadneedle Investments, also thought that Baillie Gifford’s is a total return strategy and not pure income, backed by the belief that the most sustainable way to invest from an income perspective is through a growth in earnings which are paid back as dividends in certain companies cases.

“Baillie Gifford put more emphasis on cash flow generation businesses. To this end, any significant shifts in sector exposure will be driven by a shift in long-term conviction on this basis, rather than trading short-term price moves,” she said.

“Jupiter Japan, in comparison, are more sensitive to valuation but are similarly driven by earnings growth, ultimately leading to better income. On balance the Jupiter fund arguably offers a purer approach if you had just one fund in this space, and is likely to be more responsive to shorter term gyrations in the market. It also has fund size on its side, having a much smaller pool of assets to be run alongside.”

Finally, Hawksmoor’s Lockyer, who has owned both, now only owns Jupiter Japan Income.

“We sold Bailey Gifford about two years ago, mainly because the two funds do something very similar,” he said.

“Jupiter, however, takes a more balanced perspective and is not as focused on high-growth companies. Back then it was decided that we wanted to reduce our overall exposure to growth. And the Jupiter income fund also has a higher yield.

“If we had to choose between the two of them, we would choose to be Jupiter Japan. But if we were allowed to have a broader brief, the small companies area is particularly attractive in Japan. In this space, we would recommend M&G Japan Smaller Companies.”