The collapse of Silicon Valley Bank and the takeover of struggling Credit Suisse are “financial cracks” that investors need to prepare their portfolios for, BlackRock strategists have warned.

Stock markets have been falling for the past two weeks, over which time Silicon Valley Bank collapsed after a run on its deposits, authorities stepped in to offer reassurance about the health of the banking sector and, over the week, UBS agreed to buy ‘too big to fail’ bank Credit Suisse.

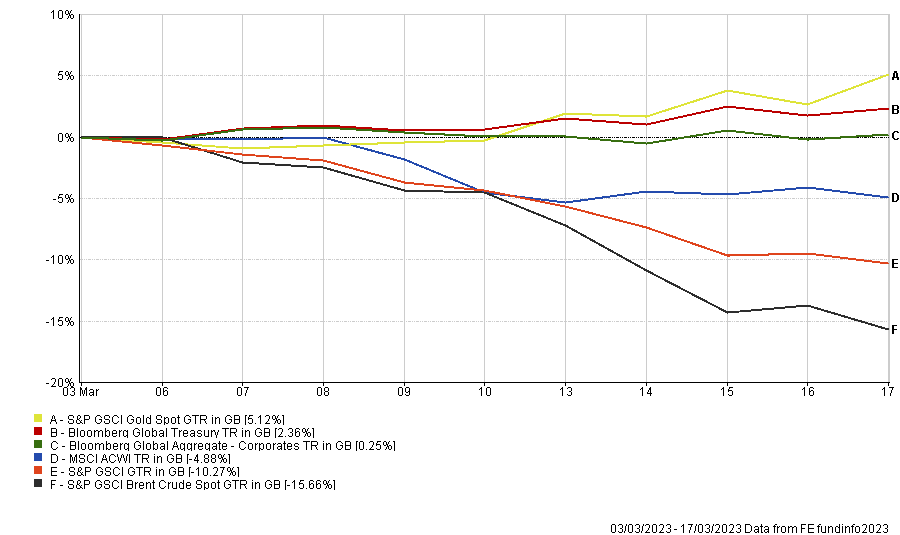

Strategists at BlackRock argued that these cracks in the financial system are a result of central banks’ most rapid rate hikes since the early 1980s. These cracks have caused global equities to fall by close to 5% in the past two weeks, while sending investors running to gold and bonds.

Performance of indices since 6 Mar 2023

Source: FE Analytics

Jean Boivin, head of the BlackRock Investment Institute, said: “The banking stresses that are roiling markets are very different – but what they have in common is that markets are now scrutinizing bank vulnerabilities through a lens of high interest rates. We don’t see a repeat of the 2008 global financial crisis. Some of the troubles that emerged recently were longstanding and well-known, and banking regulations are much stricter now.

“Instead, this is about a recession foretold. Why? The only way central banks could bring inflation down was to hike rates high enough to cause economic damage. The latest financial cracks are likely to tighten credit, dent confidence – and eventually hurt growth.”

When it comes to what this means for investing, BlackRock has three clear takeaways from the events of recent weeks.

The first is that “risk assets are not pricing the coming recession”. This leads it to maintain its tactical underweight to equities – which has been in place since last year – and to downgrade credit.

“We expect reduced bank lending in the wake of the sector’s troubles. The recession is likely to see more credit tightening now. We downgrade our overall credit view to neutral as a result,” Boivin said.

BlackRock had been positive on investment grade credit for some time, arguing that it was one of the assets best-placed to hold up when tighter monetary policy causes the economy to slow, but is now neutral. The firm has also gone underweight high-yield bonds.

Secondly, BlackRock is overweight short-term government bonds. It thinks the coming recession will be “different” in that central banks will cut interest rates to resuscitate growth.

Instead, the firm believes central banks will continue with efforts to quash persistent inflation and will distinguish this from anything they have to do to shore up the banking system.

The European Central Bank did this last week by hiking rates as originally telegraphed while BlackRock expects the Federal Reserve to take a similar approach when it holds its monetary policy meeting this week, especially as recent data suggests core inflation is not on track to drop to the Fed’s target.

“That’s why we could see a reversal of the recent sharp drop in two-year and other short-term government bond yields,” Boivin said. “As a result, we now prefer even shorter maturities for income in this asset class. We stay underweight long-term government bonds and upgrade inflation-linked bonds given our view inflation is likely to stay well above current market pricing.”

The final takeaway is BlackRock’s preference for emerging market assets over those from the developed market economies.

It points out that markets have been focused on the “mayhem in the developed world” while overlooking positives such as Asia’s economic restart from Covid restrictions and China’s supportive monetary policy.

“This should benefit emerging market assets, in our view,” Boivin said. “As a result, we keep our relative preference for emerging market stocks. We also go overweight on emerging market local-currency debt as emerging market central banks near the end of their hiking cycles and possibly cut rates.”