Alliance Trust is a popular option for core equity holding in portfolios, offering exposure to global equities via nine management groups.

The company made some significant changes last year, turning over more than half of its holdings due to big changes in the markets.

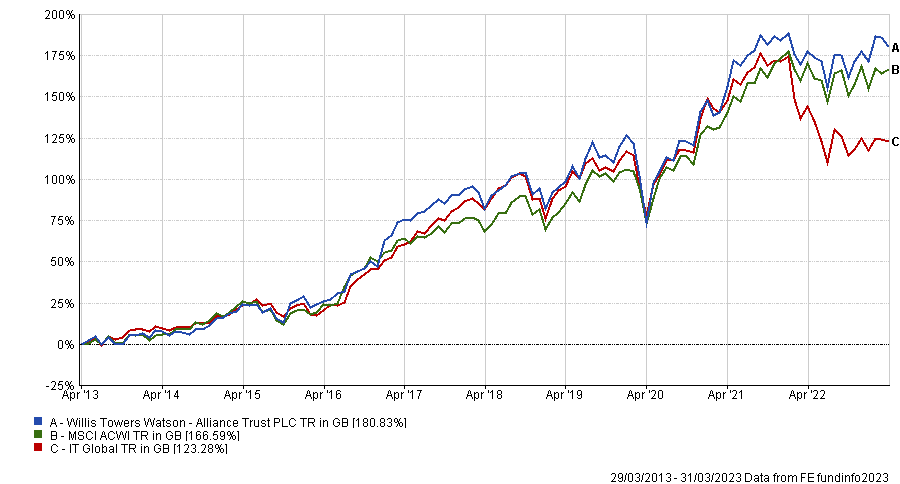

The portfolio is up 180.8% over the past 10 years, which is 14.2 percentage points higher than the average of the IT Global sector. It is, however, part of the sector’s second quartile, trailing behind among others Scottish Mortgage Investment Trust and Lindsell Train IT.

Performance of the trust over 10yr against sector and index

Source: FE Analytics

The trust is also one of the dividend heroes, having raised dividends for 56 consecutive years and Craig Baker, global chief investment officer at Alliance Trust’s management firm Willis Towers Watson, says that the company is well positioned to continue on this trajectory.

Here, he tells Trustnet why the past five years were hard for bottom-up stockpickers and what higher interest rates mean for businesses.

Can you summarise your investment process in three sentences?

It is a multi-manager approach to global equities focusing on finding the world's best bottom-up stock pickers with a long-term time horizon.

It blends them in a way that ensures stock selection drives all of the outcomes relative to benchmark rather than style, country or sector.

We see the trust as a core solution for any UK retail investor. We are essentially doing the job for the individual investor in selecting who are the best stock pickers.

What differentiates you from your peers?

Unlike a single manager approach where the top five to 10 stocks would completely dominate the portfolio, we have a lot of stocks that are pretty much equally weighted.

Overall, it looks nothing like the benchmark. It is made of small decisions on which are the best companies to own rather than a big country position in area X or Y.

What was the trust’s best call last year?

ExxonMobil was the best performing stock with a return of about 108% over the calendar year. It’s not that surprising, because the energy sector is what drove the market in 2022.

Performance of stock over 1yr

Source: Google Finance

What led the market for a number of years through to the end of 2021 was technology as growth stocks were doing incredibly well. A lot of people talked about a switch from growth to value, but the big story was a switch in market leadership from technology to energy.

What was the Trust’s worst call last year?

We were overweight in Salesforce and it produced returns of -42%. It had the biggest impact on the portfolio.

Performance of stock over 1yr

Source: Google Finance

However, none of our positions tend to have too much impact on the portfolio. Our positions tend to not be far off equally weighted, so no stock causes massive positive or negative.

Alliance Trust has increased its dividends for 56 consecutive years. How much reserves do you have?

Our revenue reserves are about £102m and the total distributable reserves at the end of December were £2.9bn.

In 2022, we had a significant increase in receipts from dividends of the underlying companies, so we were more than covered with the dividend that we paid out in 2022. We are not in danger of being concerned about whether we can continue that trajectory of always increasing dividends.

Alliance Trust is trading at a discount. Are you considering a share-buyback programme to raise the share price?

The board does have a share buyback programme to ensure there's some stability in that discount so that investors don't suffer from buying or selling it at the wrong time. That's why the discount has been kept close to that five to six range for the whole of the past six years.

When the whole sector is at a discount, that doesn't imply that a share buyback programme is necessary to get the trust to a slightly lower discount, but it ultimately depends on the board.

You have been managing the trust for six years. What has been the most challenging moment so far?

The biggest issue was that the market was just driven by a very small number of companies doing incredibly well until last year. Bottom-up stock pickers are not going to thrive in an environment where there are just five companies driving everything.

We are starting to see fundamentals driving share prices, so we're pretty excited about what that means for the next few years.

The passive index was almost the best performing portfolio out there for the past five years, but that’s probably not going to be the case for the next five years, which could be a very strong period for active managers.

What is your outlook for the coming years?

Companies that are continuing to deliver despite higher rates will do well, but a number of companies that had primarily survived or thrived because of essentially free money for a long period of time and no recession will have a tougher time now.

I am not necessarily saying that rates are high relative to long-term history but they are much higher relative to short-term history. There isn't that same element of free money and there’s potentially a recession looming.

If you could manage a trust or a fund in another sector, what would it be?

Something in the real assets space would probably be quite interesting: looking for areas that could be a good diversifier to equities and also giving some help in an inflationary environment.