"Follow the supply chain" is one of the ways Janus Henderson Investors is translating phenomenally profitable trends in the US into Europe. Nvidia and Microsoft may be grabbing headlines on a global scale but follow the supply chain and you eventually arrive at less hyped and more attractively valued companies in Europe, such as Siemens and Schneider, which are supplying hardware and software to data centres.

Portfolio manager Tom O’Hara has positioned his European equity portfolios to benefit from what he calls the "capex super cycle", referring to governments and corporations spending at unprecedented levels. He is also avoiding the "donors" such as banks and utilities that governments could hit with profit taxes to finance their spending sprees.

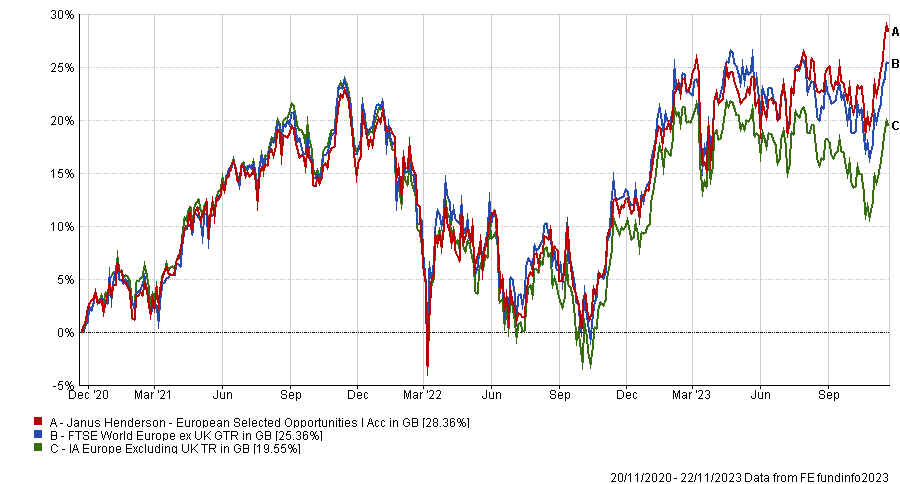

By playing these trends, the £2bn Janus Henderson European Selected Opportunities fund has pulled ahead of the pack in 2023 and is a top-quartile performer over one, three and five years.

It is up 12.8% year to date to 21 November, versus 8.6% for the average fund in the IA Europe ex UK sector in sterling terms and 10.7% for its benchmark, the FTSE World Europe ex UK index.

Fund vs sector and benchmark over 3yrs

Source: FE Analytics

O’Hara, who will take the fund’s reins when veteran stockpicker John Bennett retires next year, tells Trustnet how he is avoiding companies that will get “fleeced” by governments and talks about being the frontman of a band before moving into fund management.

What is your investment process?

We are looking for global champions listed in Europe at the right price.

We’re running an all-weather fund so we don’t skew the portfolio into expensive growth stocks that get hurt when interest rates come down, nor do we go searching for cheap stocks just because they’re cheap. So we sit in the middle, we’re style agnostic and we certainly challenge ourselves to perform in all market environments.

How is the fund positioned currently?

We have a large exposure to what we’re calling the capex super cycle. The US is running a 7% fiscal deficit, which has never been seen before in peacetime, and the government is spending heavily on roads, highways and bridges. Spending on factories in the US is back up to 0.6% of GDP and we’ve not seen that since 1990.

In terms of how we get it, we own Holcim and CRH. They’ve got really strong visibility and growing order books, but they’re still quite cheap because they’re construction businesses that are seen as highly cyclical.

Holcim is on a 9% free cash flow yield. CRH is a bit more expensive but it’s still on 7-8% free cash flow yields. When I put those valuations next to the degree of visibility you’re getting from this new isolationist-minded, fiscally-minded US shift, it’s really cheap.

Not only do we see the government spending more, but big corporates are spending as well. Amazon, Apple, Google, Microsoft and Meta are entering the most capital intensive period in their entire history. They spent $70bn on capex in 2019 and will spend $190bn in 2024 and it’s going to be repeated every year, certainly for the foreseeable future.

Most of what they’re doing is building data centres for cloud computing and artificial intelligence. Siemens and Schneider Electric look after a lot of the hardware and software in these data centres.

Looking to the semiconductor side of things, we think Microsoft is Nvidia’s biggest customer but Nvidia outsources production to Taiwan Semiconductor, which has to order more chip-making equipment and a lot of that comes from Dutch-listed companies like ASM International and BE Semiconductor Industries. We’ve got Atlas Capco because it sells vacuum technology into semiconductor production facilities.

Europe has a lot of the picks and shovels behind the sexy themes and when I can see just how much money is being spent by governments and by corporates, it’s really about making sure you’re in the right places with those picks and shovels.

Do you have any significant overweights?

We have a big overweight to oil companies, which have been in a poor place for the past decade. That has changed management behaviour to focus on paying down debt and paying shareholders, not chasing volume but prioritising value.

We met the oil management teams and they’re all unanimous in their message of capital discipline. Oil stocks are very cheap with 15% free cash flow yields.

Have you sold any stocks recently and why?

We sold Hugo Boss. My colleague had identified a turnaround story but we think it has largely played out. The stock is likely to become a bit more of a proxy for consumer sentiment which is obviously weakening.

Are there any sectors you don’t invest in?

In an era when governments are running higher deficits, they’re going to be greedier and will target banks with one-off profit taxes because voters don’t like banks. Avoid industries that the government might fleece.

We own no utilities for a couple of reasons. Many of the utilities have their profits dictated for them by governments, for instance the guaranteed pricing on windfarms. The other reason is that many of these utility companies are cheap debt junkies. They need debt to build windfarms and other projects. Now debt is much dearer.

What were your best and worst calls in the past year?

Our best calls were the capex super cycle names such as semiconductor capital equipment (BE Semiconductor Industries, ASM International) and building materials (Holcim, CRH).

Our worst decision was getting overweight banks right before SVB hit. We panicked and bought banks believing they would outperform in any European bull market. We have now reverted to our long-term – and largely successful – policy of not owning banks.

What do you do outside of fund management?

I have three young children so that takes up a lot of time. I co-founded a podcast production company called Persephonica, which does The News Agents and a new one called Political Currency, which is George Osborne and Ed Balls shooting the breeze about finance and politics.

I own a brewery called Kelham Island and a pub called Fagans, which are both Sheffield institutions. I grew up in Sheffield so it’s about staying involved in my home city.

And all that is because I needed a new hobby once I gave up the band, RALE, when I had kids. We played Leeds and Reading festivals in the summer of 2017. I was the singer but I play guitar, bass and a bit of piano so in the practice room we had lots of fun just writing and composing together.