Japan and the emerging markets are areas several fund managers are backing for a quick recovery to recent drops following the outbreak of the Iran war.

Markets have plummeted in recent weeks after the US and Israel launched strikes on Iran at the end of February, killing supreme leader Ayatollah Ali Khamenei.

In response, Iran has threatened attacks on ships sailing through the Strait of Hormuz, a significant waterway through which roughly a fifth of global oil supply passes.

This has led to an oil price spike and reignited fears of rising inflation, which, alongside weak economic growth, could put many countries around the world into a ‘stagflation’ scenario.

Selling has been indiscriminate, with 95% of funds making a loss since the war began, according to a recent Trustnet study.

Yet not all markets will be as affected by the war as others. Below, we asked fund managers which areas they would back to recover quickly and where investors may wish to buy the dip.

Japan and Korea

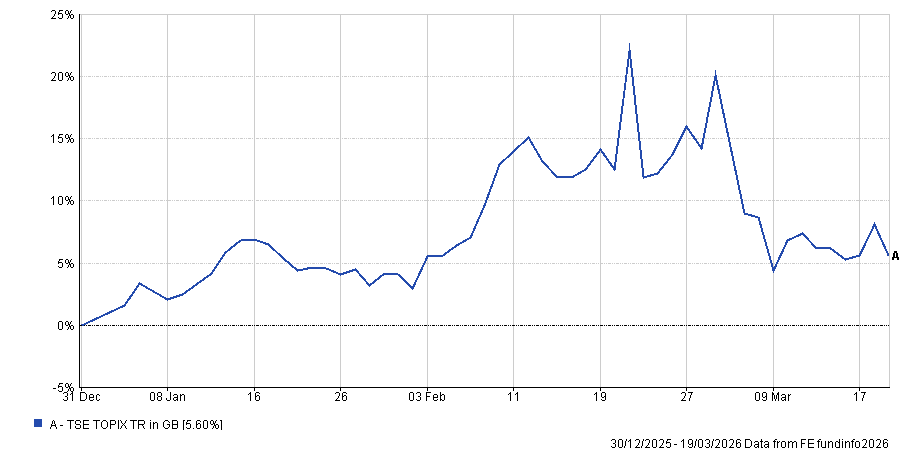

Japanese equities were the choice of AVI Global Trust’s Joe Bauernfreund. The Topix index is up so far this year (5.6% in sterling terms) but is down 9% since 2 February when the first strikes were made.

Performance of index YTD

Source: FE Analytics

“Over the past two weeks, Japanese equities have come under pressure amid a broader global ‘risk-off’ move. However, the magnitude of the sell-off appears disproportionate to underlying fundamentals and has left parts of the market looking oversold,” he said.

“This may present an attractive entry point for investors, particularly given that Japan’s macro backdrop is more supportive than at any point in decades, with sustained wage growth, improving domestic demand and a structural shift away from deflation.”

Corporate governance reforms should also continue with new prime minister Sanae Takaichi now in office, as she is “a long-standing advocate of governance improvements”. Additionally, the first revision of the Corporate Governance Code is due in July, which should also improve governance.

“While recent equity performance has been driven largely by exporters benefiting from yen weakness, domestically focused small-caps remain particularly compelling,” he noted.

“Many are cash-rich, undervalued and increasingly positioned to unlock shareholder value as reform pressures intensify.”

Bauernfreund also highlighted Korea, the market he backed last month as his favourite pick for 2026. The Kospi index has sharply underperformed other major markets in recent weeks as the country is more sensitive than most to energy price spikes, but he noted that ongoing equity market reforms and the compelling valuations remain intact.

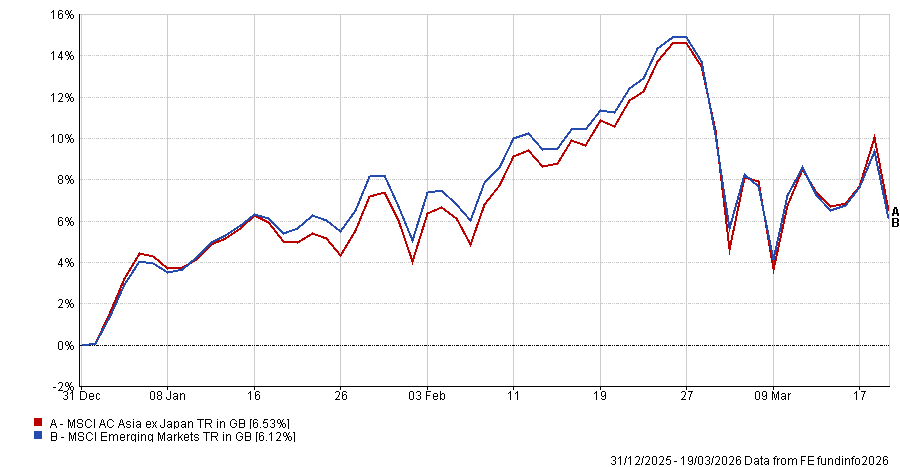

Emerging markets and Asia

Darius McDermott, managing director at Chelsea Financial Services, said it is almost impossible to know when the dip has finished and does not think now is the time to “buy the dip aggressively across either developed or emerging markets”.

However, he added that the long-term investment case for emerging markets remains intact and investors with a longer-term mindset who were thinking of investing anyway could look to begin building positions now with the market down.

“Economies such as India and Indonesia are entering a demographic sweet spot, with young and expanding workforces that contrast sharply with the ageing populations of developed markets,” he said.

“At the same time, government balance sheets across many emerging economies are generally stronger than those in the developed world and parts of Asia remain global leaders in areas such as robotics, automation and AI-driven manufacturing.”

“In the near term, the situation remains fluid and we would prefer to exercise patience rather than rushing to buy the dip. However, periods of volatility often create opportunities over time and, for long-term investors, the structural drivers supporting emerging markets remain firmly in place,” he concluded.

On Asia, he noted the continent is home to some of the biggest energy-importing countries in the world but said the impact on listed companies can be less than many assume.

“Energy typically represents only a moderate share of costs across most sectors, meaning the longer-term implications for corporate earnings may be more limited than the headline macro risks suggest,” he said.

Performance of indices YTD

Source: FE Analytics

For investors seeking exposure to the region, he highlighted Guinness Asian Equity Income for focused Asia exposure, while Invesco Global Emerging Markets could provide broader diversification across emerging economies.

Saudi Arabia

Investing in the Middle East may seem like the ultimate contrarian trade at present, with Iran targeting other Gulf states as part of its retaliation.

Sebastien Mallet runs the T. Rowe Price Global Value Equity strategy, so is used to taking positions that most would avoid.

“Geopolitical shocks often trigger broad risk-off moves across emerging markets, which can create significant market dislocations. In our experience, sharp sell-offs driven by geopolitical headlines have historically proved to be good entry points where the underlying fundamentals remain intact,” he said.

He chose Saudi Arabia as his pick for a market that could rebound. Iran has targeted the country, but Mallet said the “direct impact on Saudi Arabia may be more limited than markets initially fear”.

“The country still has alternative routes for oil exports through the East-West pipeline, which could help mitigate disruption if needed. As a result, we feel the initial moves may have been overdone and certain sectors like financials appear attractive at present.”

Do not buy the dip

Not all managers thought now was a good time to invest, however. Mirabaud Asset Management’s Paul Middleton stated he was unconvinced investors should buy the dip.

“At the time of writing, it is not clear to us that the current sell-offs in markets can be bought with a high degree of confidence,” he said.

“To be buying the dip here, you would need to either have a high degree of confidence that the war will end very quickly or you need to be able to make the case that some assets are trading at distressed levels and that buying at these levels has generated good returns over the long term.”

Taking the MSCI Japan index as an example, he said the index is down around 10% since February in dollar terms but still trades on a price-to-earnings ratio of 17x.

Previous lows have reached 12x earnings, suggesting that there could be further for the market to fall if things get worse.

“These are not distressed levels. To buy the dip you need more of a view that the war will end quickly,” he said.