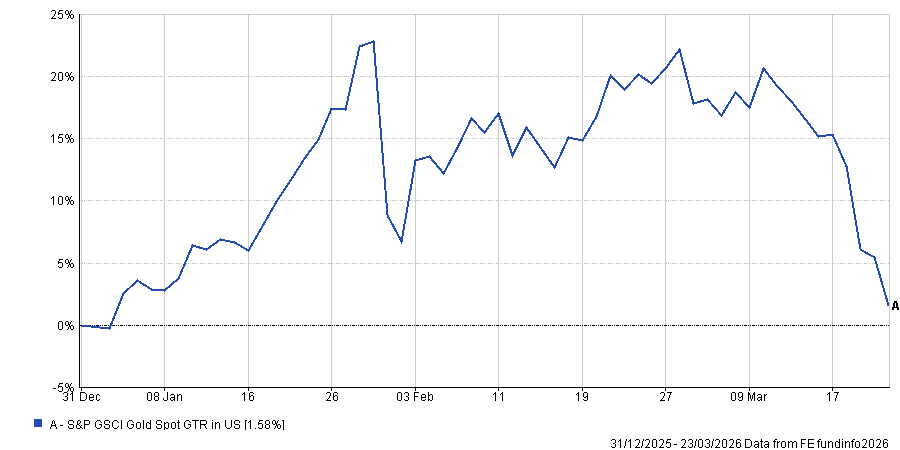

Gold has fallen more than 15% since the Iran conflict began, handing back most of this year’s gains despite the war in Iran creating the conditions that historically favour the safe-haven asset.

The yellow metal hit its all-time high of $5,589 per troy ounce on 28 January 2026, more than a month before the conflict began. Gold had been one of 2025’s best-performing assets, rallying hard on tariff uncertainty, strong demand from exchange-traded funds (ETFs) and buying by central banks.

But since the US and Israel launched coordinated strikes on Iran on 28 February, bullion has fallen more than 15.8% to around $4,394/oz, wiping out almost all 2026 gains to leave the metal up just 1.6% over the year-to-date. Last week was gold’s worst weekly performance in more than 14 years.

Performance of gold over 2026 so far

Source: FE Analytics. Return in US dollar between 1 Jan and 23 Mar 2026

Investment experts point to three forces driving gold’s recent weakness: the strength of the US dollar, rising bond yields and forced selling.

The dollar has surged as an alternative safe haven, undermining gold’s appeal. Jason Hollands, managing director at Bestinvest, explained: “Gold typically exhibits an inverse relationship with the US dollar and the recent strength in the dollar has been a significant headwind.”

Meanwhile, as inflation expectations have jumped on the back of soaring energy prices, government bond yields have spiked globally, raising the opportunity cost of holding a non-yielding asset. Susannah Streeter, chief investment strategist at Wealth Club, said: “As government bonds, in particular treasuries, see yields rise, it makes gold less attractive given that gold pays no interest.”

Neil Wilson, investment strategist at Saxo UK, noted that the US 10-year yield broke out of its prior range last week, UK 10-year gilts hit their highest level since 2008 and German bund yields reached 15-year highs. Markets have fully priced out rate cuts and are now pricing in hikes.

On the forced selling point, Streeter said “investors who have made losses elsewhere in volatile markets are selling to cover positions”, adding that dollar strength also makes gold more expensive for buyers in other currencies, suppressing demand further.

However, at a deeper level, gold no longer seems to be behaving as a safe haven. When US president Donald Trump issued a 48-hour ultimatum for Iran to reopen the Strait of Hormuz over the weekend of 22-23 March, gold fell rather than rose.

Jock Henderson, investment analyst at CG Asset Management, saif the firm’s defensive multi-asset funds exited their gold position on 12 March, realising gains close to all-time highs.

“Recent demand has been predominantly narrative-driven, with strong retail investor flows into gold ETFs contributing to heightened volatility. The crisis in the Middle East has exposed this volatility and reinforced the view that gold is trading as a story rather than on fundamentals,” he said.

“Instead of acting as a diversifier, gold has traded as a proxy for risk appetite. Previously, an investor might expect gold to benefit as a haven asset during a time of conflict or as a hedge against inflation, yet it has sold off as investors look to take risk off the table.”

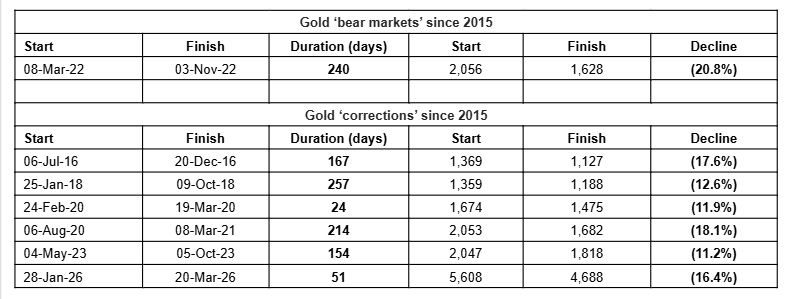

But before writing off the bull run, investors should examine the historical record. This is gold’s third major bull market since 1971 and both previous runs contained sharp pullbacks that ultimately proved temporary.

The first began when US president Richard Nixon withdrew the dollar from the Gold Standard in August 1971. Russ Mould, investment director at AJ Bell, said: “As Nixon began to run up the US federal deficit, and inflation surged, not helped by two oil price shocks, gold motored from $35 an ounce in August 1971 and peaked at $835 in January 1980.”

That run contained three mini bear markets, including a 45.9% decline lasting 18 months between January 1975 and August 1976, and five corrections of between 10% and 20%. Gold still produced enormous gains across the decade.

The second bull run began around 2001, when gold bottomed just above $250/oz. “In the face of zero-interest-rate policies, quantitative easing and balance sheet expansion the hunt was on for stores of value or haven assets,” Mould explained.

That run endured two bear markets, including a 29.7% drop in 2008, and five corrections before gold peaked near $1,900/oz in 2011.

The current bull market, which began with “stealthy gains” from 2015, has already survived a bear market of 20.8% in 2022 and five corrections, including the present one.

Source: AJ Bell, LSEG Refinitiv

“Sceptics who still view gold as a barbarous relic, a useless lump with no yield or even an asset that currently has a cost of ownership of 3.75% thanks to lost interest on cash will all be nodding as the metal slips back,” Mould said.

A pause in rate cuts or early talk of fresh hikes would only widen that cost further but he argued that the conditions for a revival remain in play, even if they are not yet dominant.

The oil-driven inflation shock from the Iran conflict echoes the 1970s stagflation environment that produced gold’s greatest bull run. Mould argued that a recession caused by higher energy costs would stretch government finances further, increasing welfare spending while reducing tax revenues. Any sharp rise in sovereign debt could prompt central banks to return to rate cuts and quantitative easing (QE), both of which have historically supported the metal.

JP Morgan maintains a year-end target of $6,300/oz and Deutsche Bank targets $6,000/oz, both anchored by central bank demand and structural de-dollarisation trends that predate the current conflict.

The question for investors is whether this is a temporary correction within a structural bull run or the beginning of a prolonged reversal. The forces pulling in each direction remain unresolved: inflation against higher rates, dollar strength against sovereign debt and haven demand against risk-off selling.

Mould suggested history offers some comfort to those choosing to hold. “Neither interest rates staying higher for longer nor a stronger dollar may help the investment case for precious metals, but both the 1971-1980 and 2001-2010 bull runs saw several retreats that did not ultimately nullify or prevent major gains, so it may be too early to give up on gold just yet,” he finished.