For most of the past decade, running a UK equity income fund meant relying on a narrow group of large-cap dividend payers. A handful of mega-caps dominated the yield available in the market and managers who wanted to grow their dividend had limited room to manoeuvre. That has changed, says Alan Dobbie, manager of the £583m Rathbone Income fund.

“The fund yields about 4.1% and we’ve increased the dividend in 31 of the last 33 years,” he said. “It’s now a healthier environment, with income more evenly spread across sectors and market caps, giving us more choice.”

After Covid, many large-caps cut dividends and did not restore them to previous levels. Shell now yields around 3.5%, BP 4.5% and Lloyds 4.5% – not the 6% or 7% yields the sector used to depend on. Income has spread down the market-cap spectrum, which suits a fund that currently holds just under a quarter of its portfolio in mid-caps.

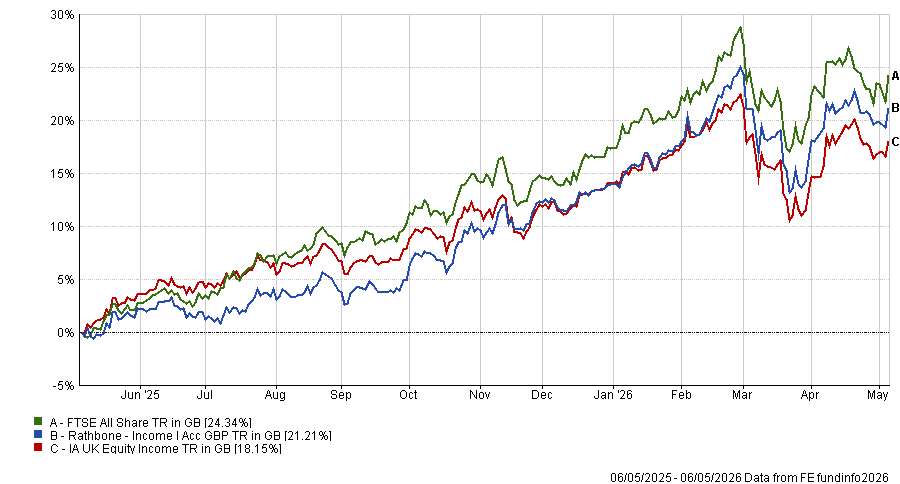

Rathbone Income returned 22.96% in 2025, ranking 24th out of 65 funds in the IA UK Equity Income sector and ahead of both the sector average of 18.67% and the FTSE All Share return of 24.02%. Year to date in 2026 it has returned 4.7%, ranking 13th against a sector average of 2.3%.

Below, Dobbie explains the fund’s risk framework, where he is finding income today and why the top 13 stocks in the FTSE All Share are at uncomfortable valuations.

Performance of fund against index and sector over 1yr

Source: FE Analytics

What is the process behind Rathbone Income?

We call it winning by not losing. It’s about trying to keep the ball in play, avoiding unforced errors. Mistakes are an inevitable part of investing, but if we can minimise both the frequency and the magnitude of those mistakes, rather than trying to find the next 10-bagger, then we can perform very well.

We think about risk through three lenses: business risk or the chance of loss from investing in companies with poor models, highly competitive industries or weak management teams; financial risk, i.e. the chance of loss from companies having inappropriate leverage; and price risk. You can own the best business in the world, but if you pay the wrong price, you can still lose a lot of money. We saw that in 2022 when interest rates rose and a lot of quality compounders fell despite operating very well.

The fund has just under a quarter in mid-caps. Why are you finding more opportunities there?

The market has been led by the largest stocks. The top 13 now account for half of the FTSE All Share, up from 36% five years ago, and those stocks are more expensive. The top 13 are up about 155% over five years, while the median stock is up about 12%. Most of the index has gone nowhere.

We’re seeing more opportunities in mid-caps and further down the spectrum. Having the ability to rotate around style and market cap is important. Ultimately, we want to own the best businesses we can if they’re trading at attractive prices.

You’ve been adding to Relx and Experian after the AI-related sell-off. Aren’t those businesses at risk from AI disruption?

It’s very stock specific. If we look at Relx, we would view it more as a content owner than a software company. They have proprietary information that lawyers or scientific researchers rely on, built up over hundreds of years. The part with more risk of being commoditised is the software and analytical tools, but we’re less concerned because the value of the company is in the proprietary, trusted, verifiable information.

We had been reducing Relx until last summer, down to just over 1% of the fund. The sell-off in February meant we could increase it and it’s now almost 3%. Relx and Experian are two areas where UK income funds don’t generally have large exposure, but you could buy Relx on an attractive dividend yield in February.

What were your best calls over the past 12 months?

The largest contributor over the 12 months to the end of March was GSK, up 47% total return, contributing 1.7 percentage points to the fund. AstraZeneca was up 33%, contributing 1.3 percentage points. Both benefited from a weak starting point due to tariff concerns. GSK also improved its delivery, consistently beating and raising guidance. AstraZeneca continued to deliver through its oncology pipeline.

Utilities were another big driver. SSE was up 68%, contributing 1.7, and National Grid up 31%, contributing 1.2. These companies are key to the UK’s energy transition, with large capex programmes and regulated returns. They now have genuine earnings growth, which wasn’t always the case. BAE Systems was up 44%.

And the worst?

Relx was the largest detractor, down 36% total return, contributing minus 0.84 percentage points to the fund. It’s still a great business but sentiment shifted from AI winner to AI loser. We had reduced it as valuations rose and bought back in during the sell-off.

The second largest detractor was Breedon, down 31%, contributing minus 0.75%, due to weak demand in UK housebuilding.

What do you do outside of fund management?

I’ve got a young family, so I spend most of my time watching their sporting activities. If I get time, I play golf and tennis, but mostly it’s family.