The Asia Pacific region has been shaped by shifting macro conditions over the past 10 years – from China’s stuttering economic growth to the surge of South Korea and Taiwan’s technology sectors.

To identify which actively managed funds navigated this landscape most consistently, Trustnet compared the discrete annual returns over IA Asia Pacific ex Japan funds against the MSCI AC Asia Pacific ex Japan index between 2016 and 2025.

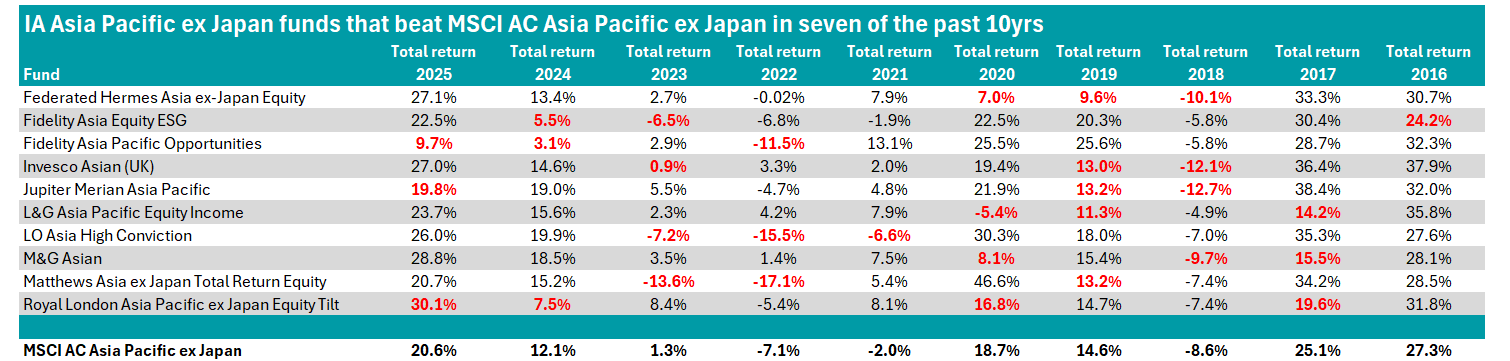

The funds in the table below beat the index in at least seven years.

Source: FE Analytics. Figures highlighted in red represent years in which a fund underperformed the MSCI AC Asia Pacific ex Japan index.

Despite their collective long-term consistency, annual performance varied significantly as a consistency score masks wide differences in volatility, drawdowns and investment style across the funds.

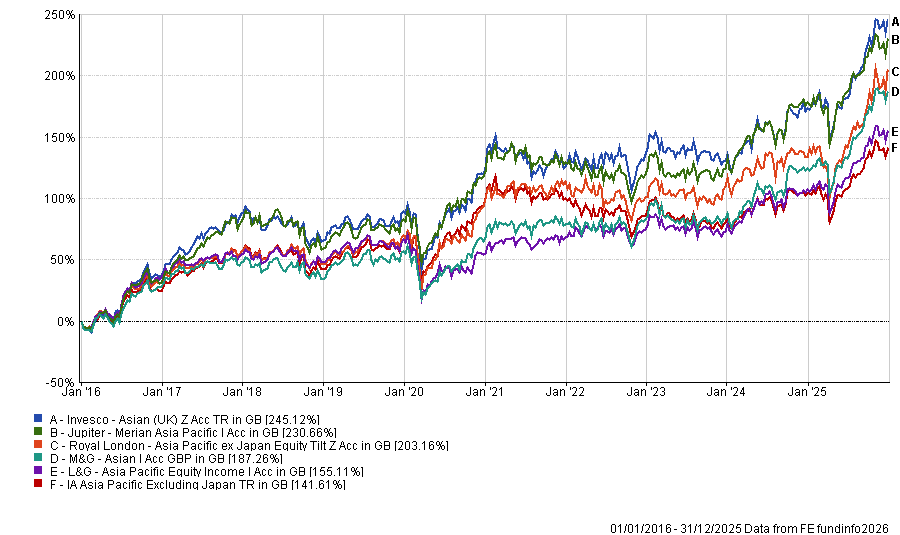

Over the full decade, Invesco Asian (UK), Jupiter Merian Asia Pacific and Royal London Asia Pacific ex Japan Equity Tilt were the top three performers in the table. The Invesco strategy posted one of the strongest long-term records in the sector, gaining 245.1%, while Jupiter Merian Asia Pacific and Royal London Asia Pacific ex Japan Equity Tilt also ranked in the top 10 in the sector, posting 230.7% and 203.1% respectively.

All three funds beat the MSCI AC Asia Pacific ex Japan, which gained 147.1% in that period.

Invesco Asian (UK) was identified as one of the sector’s most consistent performers over the decade, appearing in the top three in the sector in 2016 and delivering a first-quartile return in 2022.

The strategy, which holds just under £3bn in assets under management (AUM) and sits on AJ Bell’s ‘Favourite Funds’ list, is co-managed by FE fundinfo Alpha Managers William Lam and Charles Bond, alongside Matthew Pigott.

The management team focuses on undervalued opportunities in unloved areas of the market. The strategy is fundamentally driven, with detailed research into demand trends, pricing power, market share, cashflow and management quality. Around 100 stocks are monitored and between 50 and 70 are held in the portfolio – with top holdings including TSMC, Samsung Electronics and Tencent.

RSMR analysts noted “the managers are disciplined in adhering to the process and actively seek out contrarian positions”.

The next strongest long-term performer in the table was Jupiter Merian Asia Pacific, which also appeared in the top 10 in the sector in 2024 with a gain of 19%.

The £633.9m strategy has previously been highlighted as one of the more expensive funds justifying its higher cost, with an OCF of 1%. It was one of the most bought in the sector last year and the fund’s assets have more than doubled since May 2025.

Amadeo Alentorn has managed the strategy since 2011 and now co-manages it with Yuangao Liu, Matus Mrazik, Sean Storey, James Murray and Tarun Inani.

RSMR analysts said the investment process is “more regimented” than typical active funds in the peer group, as it is managed using a proprietary multi-factor quantitative model that aims to exploit market inefficiencies and deliver consistent performance relative to the benchmark over time.

“The approach focuses equally on risk and return, resulting in a well-diversified fund run by a highly risk-aware team,” the analysts said.

The £2.3bn Royal London Asia Pacific ex Japan Equity Tilt fund also delivered a strong decade-long record. It topped the table in 2025 with a gain of 30.1% and holds a ‘Responsible’ rating from Titan Square Mile.

While classed as active, the strategy is systematic. In 2021, management was passed to JoJo Chen and Michael Sprot who have implemented this tilt approach.

Alongside targeting a return in line with the FTSE World Asia Pacific ex Japan GBP Net Total Return index, the fund also aims to maintain a carbon footprint at least 10% below that of the benchmark, while also reducing exposure to companies involved in social controversies, human rights violations, tobacco-related business, controversial weapons or poor governance practices.

While not among the sector’s top decade-long performers, M&G Asian’s consistency has proven popular among investors and it attracted £663.4m in inflows last year as assets rose sharply, growing from around $500m in early 2025 to more than $2bn by April 2026.

The fund also boasts an FE fundinfo Crown Rating of five and is managed by Alpha Manager Dave Perrett, supported by Carl Vine. Perrett became the lead manager in 2019 following a restructure of M&G’s Asia Pacific equity team.

The M&G strategy’s largest sector exposure is information technology, although it is underweight relative to the index, while being slightly overweight consumer discretionary, industrials and communication services.

FundCalibre analysts – who gave the fund an ‘Elite’ rating – said the management team’s “hands-on approach and willingness to take meaningful differentiated positions sets them apart from their peers”, while RSMR analysts noted that the fund is “not designed to ‘shoot the lights out” but has ultimately produced consistently above average returns.

Elsewhere, the £57.8m L&G Asia Pacific Equity Income fund has struggled in some of the boom periods but has offered strong downside protection in tough markets.

While it delivered a fourth-quartile return in 2017, it did well in 2018, down 4.9% - the lowest loss among funds in the table above and almost half of the MSCI AC Asia Pacific ex Japan index’s 8.6% drop.

Co-managers Ji Shi and Camilla Ayling took over in 2023 from longstanding manager Paul Hilsley, who led the strategy for more than 14 years – within which time he also helped establish LGIM’s Asia Pacific equity income capability.

The fund’s largest geographic exposures are China (23.6%), Korea (21.1%) and Taiwan (17.4%). The portfolio is mostly invested in large-caps – with some of its biggest overweights including Samsung Electronics and Ping An Insurance - but 8.6% is invested in mid-caps.

Performance of the funds vs sector, 2016-2025

Source: FE Analytics