Markets fluctuate on a daily basis but every so often a major shock – like the Covid crash, Liberation Day and Russia’s invasion of Ukraine – sends stocks plummeting.

For investors, the challenge is identifying which funds are best positioned to take advantage of the following recovery, as valuations reset and sentiment begins to stabilise.

Rather than modelling a global crisis, this feature looks at each equity market in isolation, with Darius McDermott, managing director at Chelsea Financial Services, revealing his picks across each region.

In a market sell-off, he said it is typically value stocks that lead the recovery, as depressed valuations and improving sentiment drive a stronger rebound.

However, context is important. If the sell-off is being driven by a genuine structural shift – for example, a major repricing of a dominant theme such as AI – McDermott said he would be more cautious about “stepping in too quickly”.

“In those cases, what appears cheap can prove to be a value trap if earnings expectations are still too high,” he warned.

More often, however, sharp drawdowns are driven by fear rather than fundamentals. In those instances, he said the instinct is to “lean in, not step back – but selectively”.

While a 20% fall does not mean ‘buy everything’, McDermott noted it is usually a strong signal to start adding risk where valuations have become disconnected from long-term prospects.

“We would also look to increase exposure to higher beta areas – funds that move more than the market,” he added.

“You wouldn’t necessarily add to these funds at the height of the sell-off but once markets begin to stabilise, they are often the best way to capture the recovery.”

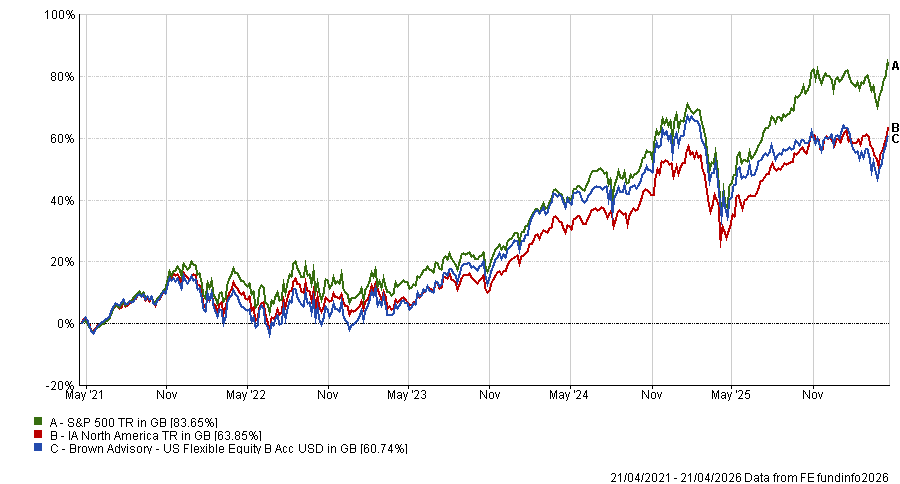

US equities: Brown Advisory US Flexible Equity

If the US market dropped 20%, McDermott said he would turn to the $878.3m Brown Advisory US Flexible Equity fund, noting it has the flexibility to invest across both growth and value, focusing on high-quality businesses where valuations have become disconnected from fundamentals.

“In a sell-off, this allows the manager [Maneesh Bajaj] to take advantage of market dislocations without being tied to a single style,” McDermott said.

“That flexibility is particularly valuable in uncertain environments, where the nature of the downturn is not always clear.”

As sentiment stabilises, McDermott noted that the fund is also well-positioned to participate in the recovery while maintaining a focus on downside risk.

The fund, which has an ‘Elite’ rating from FundCalibre, demonstrated its strengths when it outperformed the S&P 500 in the 12 months ending July 2024 – despite having little exposure to Nvidia during its surge.

As at 28 February 2026, many major AI players feature in the top 10, including Alphabet, TSMC, Microsoft, Meta and Amazon.

Performance of the fund vs sector and benchmark over 5yrs

Source: FE Analytics

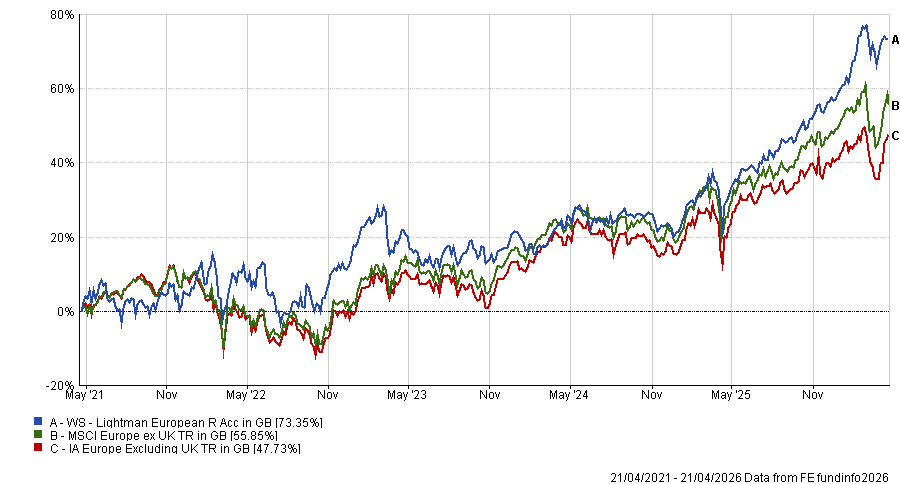

European equities: WS Lightman European

In the event the European market fell, McDermott said WS Lightman European is his pick. The £1.4bn strategy, which is co-managed by FE fundinfo Alpha Manager Rob Burnett and George Boyd-Bowman, was one of the most bought European equity funds in 2025, attracting £368m in inflows.

He described it as a “deeply contrarian, value-focused fund” that leans into the parts of the market that are most out of favour during downturns.

The portfolio typically holds between 40 and 50 stocks, with positions averaging 2-3% and no formal sector or country limits. The active share is usually above 80%.

McDermott noted that the fund’s value-focused approach “can be challenging when growth is in favour but in a recovery phase – particularly one driven by improving economic sentiment – these stocks are often well-positioned for a sharp re-rating”.

“That gives up confidence in the fund’s ability to capture a strong rebound,” McDermott said.

Performance of the fund vs sector and benchmark over 5yrs

Source: FE Analytics

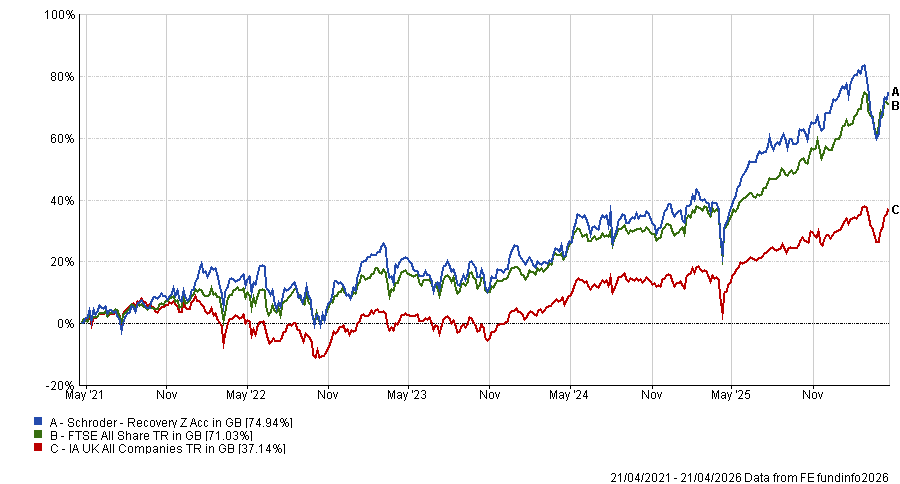

UK equities: Schroder Recovery

If the UK market fell 20%, McDermott said a deep value strategy would be his choice, highlighting Schroder Recovery.

The strategy is focused on companies that have lagged the FTSE All Share for several years and appear undervalued on measures such as price-to-equity (P/E), price-to-book and dividend yield.

“In a rebound scenario, these are typically the stocks that move first and fastest as sentiment improves, and therefore the fund is well-positioned to benefit disproportionately from any recovery following a sell-off,” McDermott said.

The £647.8m strategy is now co-managed by Andrew Lyddon and Tom Grady, following the departure of former manager Nick Kirrage last year.

Between 2016 and 2025, the fund achieved a first-quartile return in the IA UK All Companies sector in five separate years.

Performance of the fund vs sector and benchmark over 5yrs

Source: FE Analytics

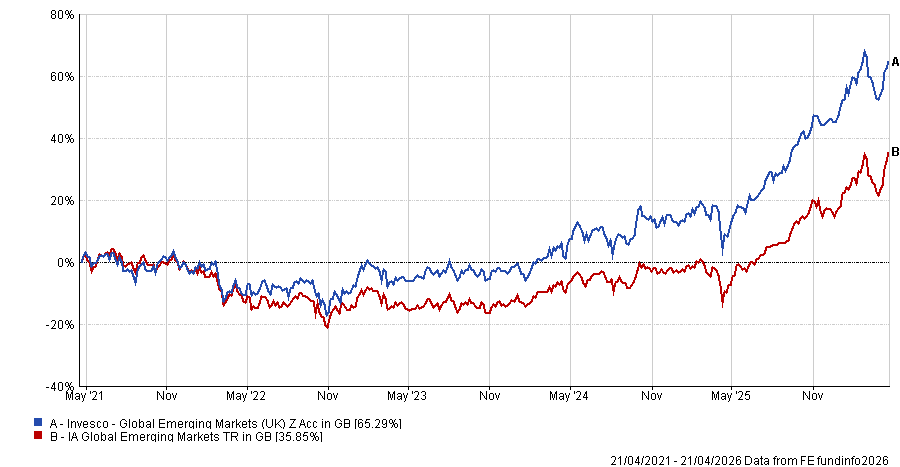

Emerging markets equities: Invesco Global Emerging Markets

In emerging markets, sell-offs tend to be more pronounced given higher volatility and sensitivity to global risk sentiment.

As such, McDermott picked the £1.1bn Invesco Global Emerging Markets, which he said “combines a strong valuation discipline with a focus on fundamentally sound companies that have been mispriced by the market”.

“Following a sharp correction, these types of businesses can rebound strongly as capital flows return and sentiment stabilises, giving us confidence in the fund’s recovery potential,” McDermott said.

The strategy – which is co-managed by Alpha Managers Charles Bond and William Lam alongside Ian Hargreaves and Matthew Pigott – has consistently outperformed, posting a 215.8% 10-year return to the end of December 2025.

Performance of the fund vs sector over 5yrs

Source: FE Analytics

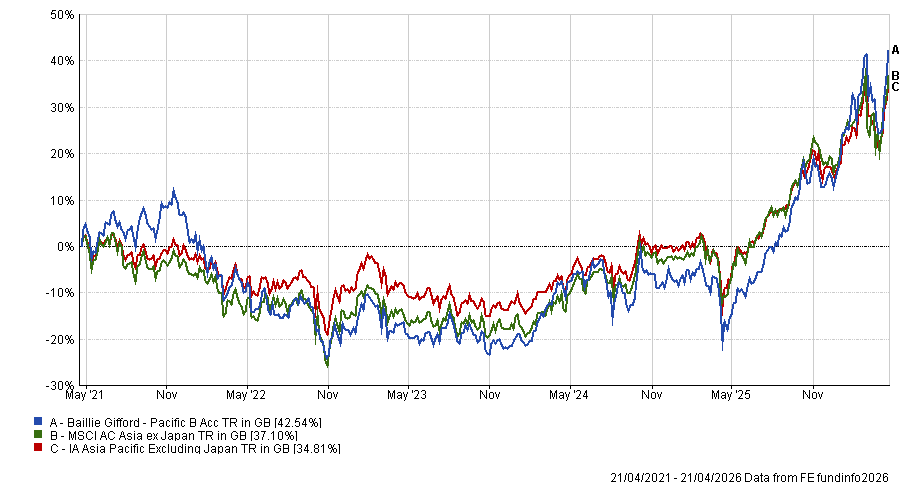

Asia Pacific equities: Baillie Gifford Pacific

McDermott said a sell-off in Asia would likely create opportunities in higher-growth areas that have been de-rated.

“It remains one of the most compelling regions globally in terms of long-term structural growth, driven by favourable demographics, rising middle classes and ongoing innovation,” he said.

“A sharp correction can therefore provide an attractive entry point into these themes at more reasonable valuations.”

He pointed to the £3.7bn Baillie Gifford Pacific fund, which is co-managed by Roderick Snell and Ben Durrant and was one of the most sold IA Asia Pacific ex Japan funds in 2025 – shedding £831.5m.

McDermott noted that the fund “can be more volatile in the short-term” but that it tends to benefit significantly once markets recover and investors refocus on structural.

This is clear to see when looking at its returns year-to-year. In 2022 – a tough year for equity markets – the fund lost 20.2%. In 2025, the fund posted a first-quartile return in the sector with a 28.8% gain.

“The managers are willing to add to their highest-conviction ideas during periods of weakness, which gives the fund strong rebound potential as sentiment improves,” McDermott added.

Performance of the fund vs sector and benchmark over 5yrs

Source: FE Analytics