The latest bout of sustained market volatility may increasingly push investors toward more defensive portfolio structures, favouring strategies that prioritise capital preservation and steady long-term returns.

Vanguard LifeStrategy 40% Equity is an established option in this space – albeit slightly smaller than its more equity-driven stable mates with £5.7bn in assets – offering a 40% and 60% split between equities and bonds.

Following previous articles suggesting funds to hold alongside Vanguard LifeStrategy 100% Equity, 80% and 60%, fund selectors outlined four strategies they believe could complement the more defensive portfolio.

Doubling down on the lower-risk profile of Vanguard LifeStrategy 40% Equity, Sheridan Admans, founder and chief investment strategist at Infundly, suggested a cautious, capital preservation-focused multi-asset strategy.

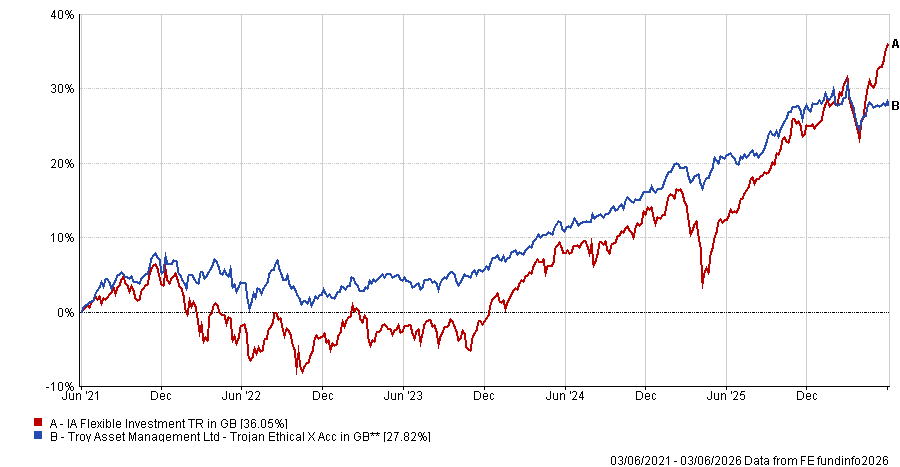

He said the £1bn Trojan Ethical fund can “reinforce the defensive purpose of Vanguard LifeStrategy 40% Equity, while adding an ethical framework and a more absolute return-minded approach than a conventional strategic asset allocation fund”.

The fund, managed by Charlotte Yonge, also complements the LifeStrategy fund by adding a more active, preservation-led philosophy, Admans added.

This philosophy is the same that underpins Troy Asset Management’s flagship Trojan strategy – using a diversified mix of high-quality developed market equities, government bonds, gold-related investments and cash – but with an added ethical framework which screens out areas such as armaments, fossil fuels, gambling, pornography and high-interest lending.

As of 30 April 2026, Trojan Ethical held 33% in equities, 55% in fixed income, 9% in gold and 3% in cash.

RSMR analysts noted that Troy may have a quality-led bias to equity selection but will utilise strategic positioning to define the way in which the funds are constructed and this will include cash management.

“The funds will be deliberately contrarian, will nearly always have holdings away from the index and pay little attention to tracking error,” the analysts said.

“Due to the absolute return approach of the fund, it will typically be a strong performer in defensive markets and will lag equity or momentum-based rallies.”

Performance of fund vs sector over 5yrs

Source: FE Analytics

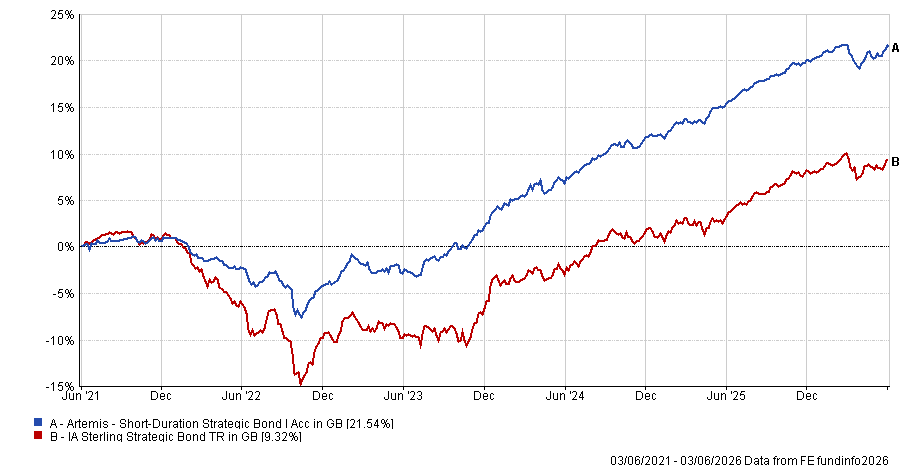

Adding short-duration fixed income flexibility to the bond-heavy LifeStrategy portfolio is Admans’ next move. For this, he suggested Artemis Short-Duration Strategic Bond, a popular choice for investors after attracting £251m of net inflows in 2025.

Admans said he likes the defensive design of the £766.5m strategy through its short-dated credit, diversified fixed income exposure and largely market-neutral rates positioning.

“The fund’s short-duration emphasis helps limit sensitivity to rising yields and supports steadier income-led returns,” Admans said.

Co-managed by Stephen Snowdon, Jack Holmes and Liam O’Donnell, Artemis Short-Duration Strategic Bond invests across government bonds, investment-grade credit and high-yield corporate bonds, adjusting allocations as market conditions evolve. Less than 5% of assets sit in bonds maturing beyond seven years.

“It looks well-suited to a higher for longer environment, where income carry and compounding can matter more than taking large duration bets,” Admans said.

The fund has posted a first quartile return in the IA Sterling Strategic Bond sector over the five years to the end of May 2026, gaining 22.1%.

Performance of fund vs sector over 5yrs

Source: FE Analytics

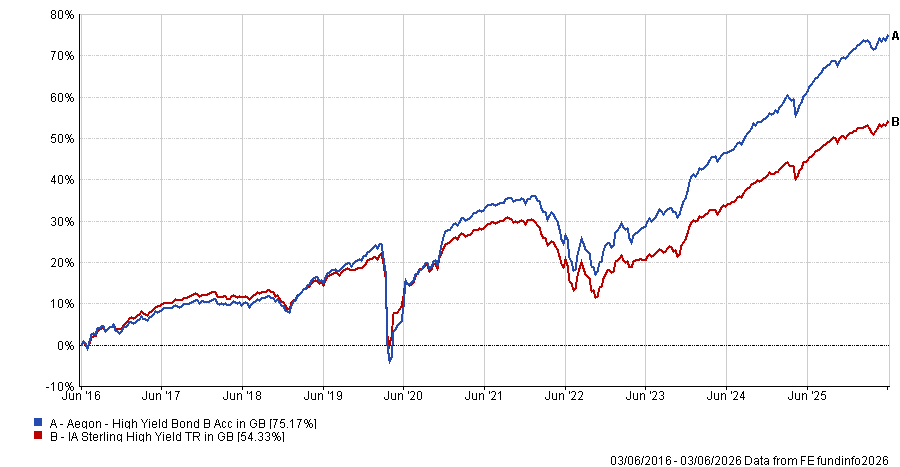

Paul Angell, head of investment research at AJ Bell, also turned to fixed income, suggesting that the £1.6bn Aegon High Yield Bond fund “blends the balanced multi-asset approach of the Vanguard strategy with a high yield exposure that typically sits between equities and bonds from a risk/return perspective”.

“The Aegon High Yield Bond fund is paying out a c.8.5% yield, delivered alongside a low level of duration thanks to high yield bonds being typically shorter maturity than their investment grade counterparts,” Angell said.

It is also actively managed from a top-down perspective, with the co-managers Mark Benbow and Thomas Hanson assessing the fundamentals, valuation, technicals and sentiment of the market.

“The extent to which they have a positive outlook across these factors then determines the fund’s target beta (0.8 to 1.2),” Angell noted.

Trustnet recently highlighted the popular fund as one of the most consistent in the IA Sterling High Yield sector over the past 10 years, beating the sector average in eight years.

Performance of the fund vs sector over 10yrs

Source: FE Analytics

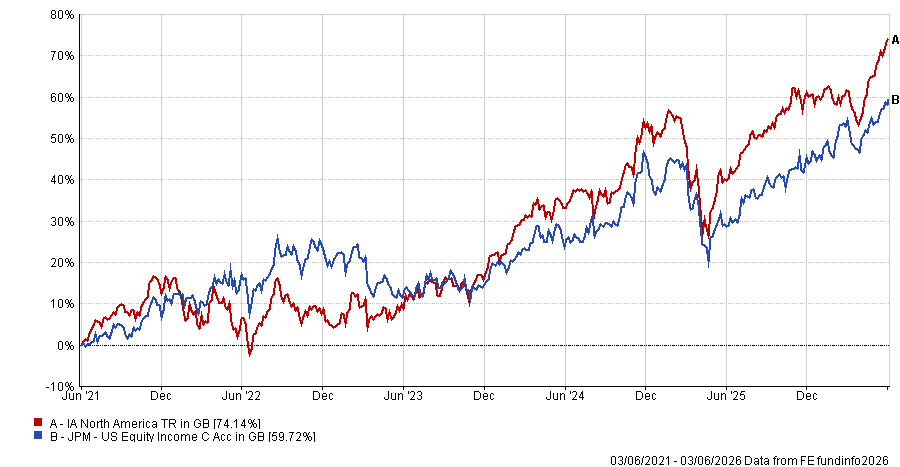

Unlike the other fund selectors, Darius McDermott, managing director of Chelsea Financial Services, looked to bolster the equity sleeve for investors, noting that the equity side “needs to work hard to bolster the more conservative LifeStrategy portfolio without adding unnecessary risk”. His suggestion is JPM US Equity Income, which is rated by both AJ Bell and Barclays.

JPM US Equity Income is the largest of the funds highlighted by selectors, with £2.6bn in assets. Launched in 2011 and co-managed by Clare Hart, Andrew Brandon and David Silberman, the strategy aims to deliver a portfolio of US equities that provides a reliable income stream while participating in long-term capital growth.

McDermott pointed to the fund’s quality and income-focused approach to the world's largest stock market, targeting companies with durable franchises, strong balance sheets and healthy dividends.

“That dividend discipline acts as a natural quality filter, producing a portfolio that tends to hold up better in weaker markets than a straight index tracker,” McDermott said.

The managers run a well-diversified 85-110 stock portfolio with low turnover, he added, ensuring “steady, defensive US equity exposure that complements rather than amplifies the risk”.

RSMR analysts noted that JPM US Equity Income has consistently delivered a yield above the market average in the US and has typically done so with lower volatility and lower drawdowns than the IA North America sector average.

“The fund tends to outperform when markets are volatile or led by high-quality dividend payers, but may underperform in markets led by highly cyclical stocks or businesses that employ a significant amount of leverage,” the analysts said.

Performance of fund vs sector over 5yrs

Source: FE Analytics