The jump in mortgage rates is emerging as one of the biggest new threats to long-term pension saving, according to research by retirement specialist Standard Life.

Although the Bank of England’s decision to hold rates at 3.75% last week may bring about future stability, many homeowners nearing the end of their existing fixed-rate mortgage deals are still facing significantly higher borrowing costs.

According to Standard Life analysis, a homeowner coming to the end of a fixed-rate deal of around 2.50% – a common enough rate in 2021 – is facing an average rate of 5.63% today. Should the homeowner secure a new fixed-rate deal at this rate on a £500,000 repayment mortgage over 25 years, their monthly repayments will jump by £866.

Mike Ambery, retirement savings director at Standard Life, said: “That is putting real pressure on household budgets at a time when many people are already contending with higher day-to-day expenses, and may lead them to reassess their wider finances.”

Crucially, putting that £866 into pension savings over 25 years from the age of 34 – the average age of a first-time buyer in the UK – would add £268,000 to the overall pension pot, the analysis said.

The price jump is stark even for those who committed to their fixed-rate just months ago, as mortgage rates have spiked from an average of 4.91% at the start to 2026 to 5.63% today. This equates to a £213 difference a month on a £500,000 mortgage over 25 years.

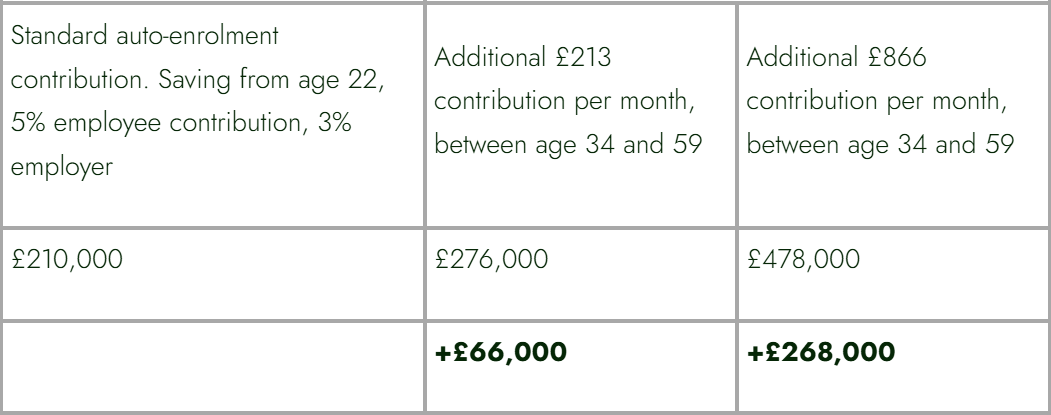

To outline again what this could mean for pension savings, the Standard Life analysis noted that someone who began working at age 22 with a salary of £25,000 who paid the minimum monthly auto-enrolment contributions throughout their career could build a total retirement fund of £210,000 by age 68.

However, as shown in the table below, if that person was able to contribute the additional £213 a month into their pension from the age of 34 for 25 years, their projected fund could rise substantially. The impact of £866 a month is even starker.

Total retirement fund at age of 68

Source: Standard Life. Assumptions: Starting salary £25,000, rising by 3.5% each year, 5% employee and 3% employer monthly contributions, 5% annual investment growth. Figures are reduced to take effect 2% inflation. Annual Management Charge of 0.75% assumed. The figures are an illustration and are not guaranteed. Earning limits not applied.

Ambery said: “For many people, buying a home is a key part of their long-term financial security – but, as mortgage costs rise, households may have less flexibility to save elsewhere, including into their pension.

“If someone needs to adjust their finances, reducing pension contributions may feel like a quick way to free up income.”

He encouraged homeowners to ensure they are getting as much value as possible from what they can afford to save, pointing out that pensions benefit from tax relief. For example, an £80 pension contribution is topped up to £100 for basic-rate taxpayers.

“If you pay higher- or additional-rate tax, you can usually claim back more through your self-assessment tax return or by contacting HMRC, reducing the true cost further,” he added.

In many workplaces, there is also the option of salary sacrifice, where additional contributions into your pension pot are matched by employer contributions, thus boosting pension savings further.

Even if an individual needs to reduce their pension contributions to keep up with mortgage payments, Ambery said it is better to remain consistent than pause pension saving altogether.

“Even small, regular payments can help avoid a much bigger catch-up later,” he said.

“But before cutting long-term savings, look across your regular spending to see whether there are areas where you can reduce costs.”

Setting a budget can also help to highlight alternative opportunities to shop around or cut back, Ambery suggested, adding that tracking any old pension plans will also provide a clearer picture of whether an individual is on track to have enough money saved for retirement.