Over the last five years, finding growth in the IA UK All Companies sector has been difficult when domestic stocks have been held back by issues such as Brexit, frequent general elections and now Covid-19.

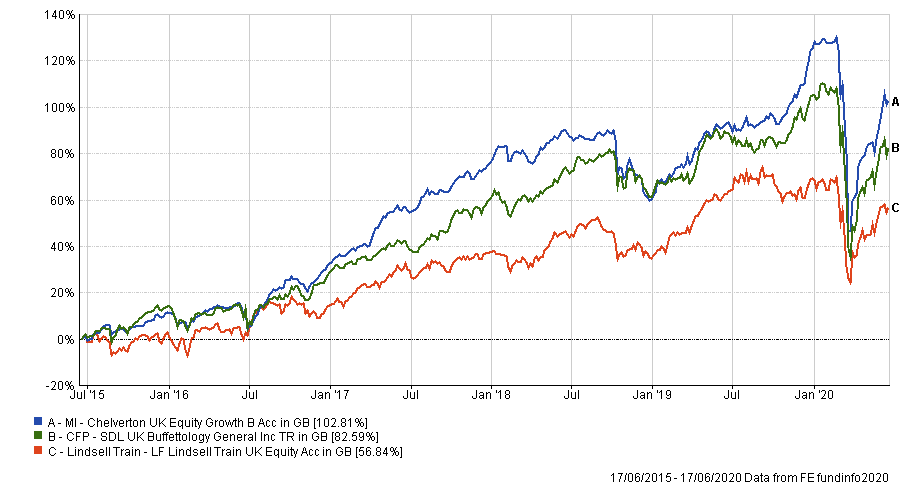

Total return for these funds over the period averaged 11 per cent, but the MI Chelverton UK Equity Growth fund would have just over doubled your investment over the same period after posting a 102.81 per cent gain.

The £601m small-cap focused UK growth fund, which is run by James Baker, operates under the thesis that small-caps tend to outperform in most market circumstances.

It isn’t entirely a small-cap only fund as it holds a few of the larger mid-cap names, but the portfolio is focused on everything below the FTSE 100.

Baker said: “Small- and mid-caps have historically had this outperformance effect and we want to harness that really to generate alpha and outperformance over the longer period.

“We try and do that in the lowest risk way as we possibly can, and that's reflected in the nature of the sort of companies that we would invest in, in terms of things like balance sheet strength and earnings visibility.”

Over the past five years, the fund has outperformed the sector’s second ranked fund, CFP SDL UK Buffettology, by 20 percentage points, and the well known LF Lindsell Train UK Equity by 45 percentage points.

Performance of funds over 5yrs

Source: FE Analytics

Small-caps, however, tend to be slightly riskier with higher share price volatility and less liquidity, which is partly why the manager has a five-stage screening process before investing.

The first stage of this is a financial screen looking at the company’s ability to convert its operating profit into cash after capital expenditure. “If you’re not, you're not going to be self-funding and you might be using accounting techniques quite aggressively to present a rather rosy picture of your profits,” Baker said.

The second and third screens are to ensure the company is growing at a reasonable rate over a GDP hurdle of 2.5 per cent per annum and that it has a sensible balance sheet, which translates into a 2.5x net debt to EBITDA requirement.

The final two screens look for companies with working capital intensity of below 30 per cent and gross margins of at least 20 per cent.

Baker explained that working capital intensity was important because “for every pound of sales you grow, that might suck in another 30p of working capital”.

“If you're growing, you don't want to always be wondering how you’re going to fund your growth,” he added. “It's the asset intensity of the business.”

Although he said in reality there are very few companies within MI Chelverton UK Equity Growth’s portfolio with working capital intensity of more than 20 per cent and with gross margins of less than 30 per cent.

“We’re giving companies a little bit of slack in the screening process, because there are so many companies with low margins, but don’t have any working capital,” the manager explained.

“They might have cash, rather than obligations in the form of money tied up in inventory or in receivables from customers.”

In this case, he said the company “can grow really fast because you don't have to finance capital so you can grow willy-nilly; it just doesn't matter”.

Conversely if a company has very high margins, they have a much larger amount of profit to finance all that working capital needed to grow the business, he noted.

“The nirvana situation for us would be a company that has very low working capital and very high margins, that's what you can find in certain things like software stocks,” Baker said.

A software stock that has been owned since the MI Chelverton UK Equity Growth fund’s launch in October 2014 is dotdigital, an omnichannel marketing automation platform.

“They’ve been growing since we’ve owned it,” the manager said. “Their top line is between 15-20 per cent per annum and it's doing that on a 20 per cent return plus on sales.

“So you have this wonderfully high return on sales and it's all dropping through as cash on the bottom line, so you kind of get into this virtuous circle.

“There aren't many companies who can grow their top line at 20 per cent and can actually increase their cash in the bank every year at the same time, and dotdigital is one of those.”

Out of all the companies that MI Chelverton UK Equity Growth looks at, its screening process has narrowed it down to about 180-200 stocks. At the moment, 121 of these have made it into the portfolio.

Baker said within these stocks, the fund’s turnover “can be quite high” but that it is always within the universe of stocks he wants to own.

The fund certainly has a very active approach to holdings. “We are changing in and out of stocks on valuations,” Baker said.

“If a company was attractively priced but the valuation is getting quite high, we might not come out of it but we might reduce our exposure to it, because it's going to be harder for it to perform from that level.

“Certainly at times of very high market volatility, you have an opportunity to add value because stocks get oversold just as they can get overbought.”

While MI Chelverton UK Equity Growth has held dotdigital since inception, Baker said he’s occasionally taken the top off and built it back up during periods of price weakness.

Dotdigital performance over the past 5 years

Source: Google Finance

When markets sold off in March, he used the opportunity to repurchase a stake in IMI Mobile, a mobile and digital communications software company: “Quite often the stocks that people really love hold up a bit longer than other stocks, and that gives you a liquidity opportunity.

“For IMI we took the top off at £4, and within four weeks we were able to buy shares back at as low as £2.35. So we are quite active in exploiting market volatility in stocks that we are confident about.”

During that same period, the fund acquired a stake in Advanced Medical Solutions, the wound care, surgical and wound closure product manufacturer.

“It is something that we’ve wanted to own for the five-year life of the fund, but literally only now has it become cheap enough in our view for us to own it because of this Covid-19 sell off,” the manager said.

On how the fund is positioned going forward, Baker said he is topping up companies whose earnings can be “reasonably robust regardless of what happens to the economy” and adding selectively to some more cyclical stocks who have been very badly hit by the sell-off where “valuations were getting ludicrous”.

He said that governments will have to do a lot of fiscal spending on infrastructure to get the economy going again and he thinks certain construction stocks are a good place to be.

“It's much more difficult to get an engineering business going again than it is a construction business,” he said.

Commenting on his investment strategy, the manager said: “We’re not trying to do anything too clever at all.

“We think if you can buy a company that’s going to grow faster than the rest of the market or faster than GDP, and that company is self-funding because they have strong cash flow, that generally means it has either strong margins or very low capital intensity. So you don't need any kind of dilutive equity issuance, and all that outperformance comes back to underlying shareholders.”

Performance of the fund vs sector since launch

Source: FE Analytics

Since launch in October 2014, MI Chelverton UK Equity Growth fund has returned 140.56 per cent compared with 29.18 per cent from its average IA UK All Companies peers.

It has an ongoing charges figure of 0.9 per cent and has an FE fundinfo Crown Rating of five.