The management change at Murray Income Trust is now complete. With the move first announced in November, Adrian Frost, Nick Shenton and Andy Marsh – the trio behind the £5.3bn Artemis Income fund – have taken the reins from abrdn's Charles Luke as of last week, following a board review that concluded the trust needed a new direction after years of relative underperformance.

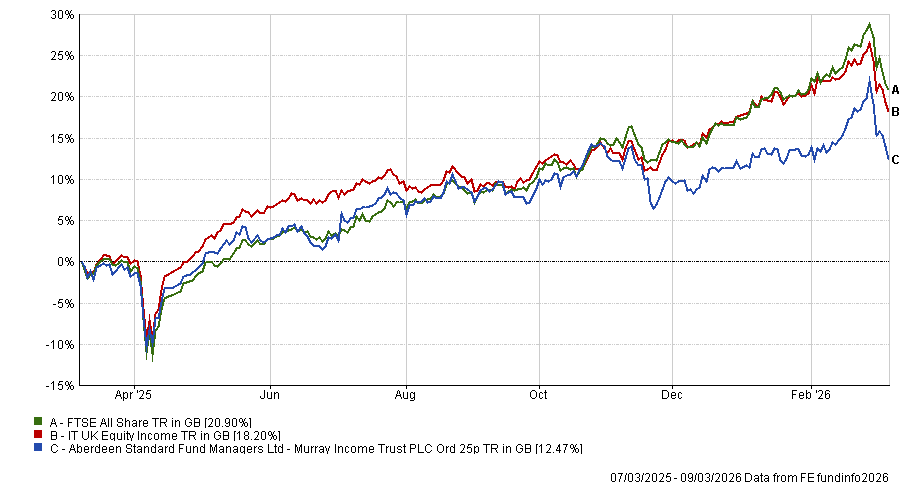

Over three and five years, Murray Income sat in the bottom quartile of the IT UK Equity Income sector, returning 19.1% and 32.3% respectively against a sector average of 31.2% and 49.2%. Even over a decade – where its record is a more respectable 111.2% against the sector's 102.8% – it trailed the FTSE All Share's 133.7%.

The incoming team carries a different record. Artemis Income has been top quartile over one, three, five and 10 years in the IA UK Equity Income sector and has beaten the FTSE All Share on a rolling five-year basis in 97% of monthly periods since its June 2000 launch.

Performance of fund against index and sector over 1yr

Source: FE Analytics

Initial reaction to the announcement was broadly positive, with Darius McDermott, managing director at FundCalibre, calling it “a positive move for shareholders” as there was “no reason why [the Artemis team] cannot replicate their success in the closed-ended structure.”

James Carthew, head of investment company research at QuotedData, said the pragmatic, style-agnostic Artemis approach “should help steady the ship,” though he noted the changes were not radical enough to warrant the modest share price dip that followed the announcement.

Now that the handover has completed, the question is whether the investment case has strengthened or whether the easy gains from the management change narrative are already made. Murray Income returned 15.7% in 2025, outpacing its sector, and has held up relatively well in recent weeks.

Rob Morgan, chief analyst at Charles Stanley, was constructive.

“Frost and his wider team have a very successful record of running the Artemis Income fund, which has been a go-to UK equity income cornerstone for years,” he said.

“That this team and approach is now available in closed-ended form with some gearing – as well as the potential to buy in at a discount at present – is appealing. The relatively low charges will also pique the interest of fund buyers in this competitive sector.”

Style continuity was also a plus for Morgan.

“The Artemis approach is fairly style neutral with relative performance driven mostly by stock selection rather than being skewed towards value or growth,” he said. “In that sense this is not an abrupt departure from one type of investing to another.”

Ben Yearsley, director at Fairview Investing, went further – he said he had started buying the trust both personally and for clients. However, the structural question is now more relevant than the performance one: with Frost's team running both vehicles, the choice between Murray Income and the open-ended Artemis Income fund comes down to whether an investor wants a trust or a fund.

“Murray Income and Artemis Income will end up being very similar in the next month or so – the choice is really down to structure, do you want an open- or closed-end fund?” he asked. “I have both in my portfolios but in this instance I'll favour trust over fund as there are very few core equity income trusts and the Artemis team is among the best.”

A question worth raising, however, is whether the Artemis team's exceptional record is itself a reason for caution. Artemis Income has been on a run that has spanned multiple market cycles, style rotations and economic regimes so, at some point, mean reversion is a legitimate concern.

Investors buying now could be backing a team at or near the peak of a long winning streak, in a strategy that has already re-rated on the back of the management change announcement.

Morgan acknowledged the point, noting that the style-neutral, stock-selection-driven approach had delivered returns without excessive risk – suggesting the outperformance is structural rather than cyclical – but past consistency is not a guarantee that the next cycle will be equally kind.

Yearsley was "not worried that recent performance has been good. Equity income is a portfolio mainstay that you stick with through thick and thin”.

Finally, abrdn’s Luke, who had been in charge of Murray Income since 2006, still manages abrdn UK Income Equity and abrdn Europe ex UK Income Equity but Yearsley said he’d “probably find other alternatives to his funds.”

“I just think many of [abrdn’s] UK funds have been average,” he concluded.