Gold is on track to hit a new record high of $2,225 per ounce by this time next year, according to Nitesh Shah, head of commodities and macroeconomic research at WisdomTree. However, if things go right, the precious metal may shoot even higher to $2,500 per ounce.

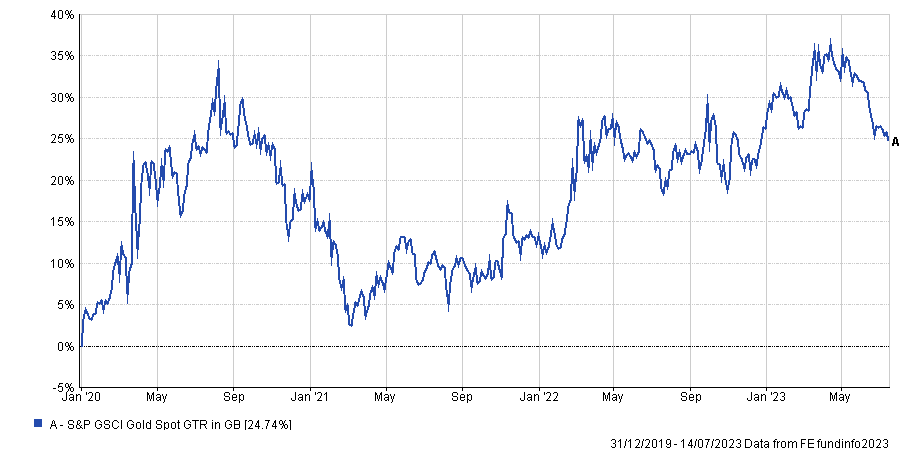

Investors in the yellow metal have had a rollercoaster over the past few years. In 2020, when the pandemic caused investors to duck for cover, it held up as a safe haven, with prices rising 17.2%. In 2021, with expectations of a recovery, it softened 3.4%.

Last year was another upswing as markets were shook by rising interest rates and inflation, war in Ukraine and the prolonged lockdown measures in China. As a result, gold surged another 11.8%.

This year, with investors taking a sanguine view on markets, it has nudged 1.4% lower. Overall, it leaves investors that bought the metal at the start of 2020 up a glistering 24.7%, with the spot price at $1,955 at the time of writing.

Gold spot price since start of 2020

Source: FE Analytics

Shah said much relies on macroeconomic data, specifically from the US. Consensus expectations are “for inflation to continue to decline (although above the Federal Reserve target), the US dollar to depreciate, and bond yields to continue to fall”.

Theoretically, rising rates is poor for gold, as the better yield on offer from low-risk bonds means investors move from the speculative gains from the precious metal to the certainty of yield.

However, rising rates this time around brings the world closer to recession – an environment where its safe haven status should prop up the price.

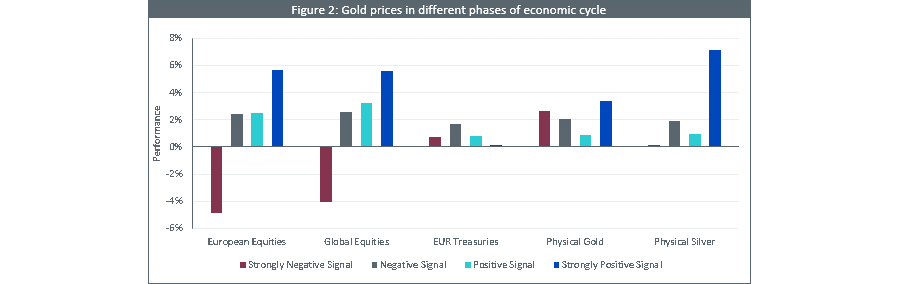

“Gold tends to perform well in times of economic stress. As the chart below shows, when composite leading indicators turn strongly negative, gold performs positively while equities tend to be negative. Gold also outperforms Treasuries, which are seen as competing defensive assets,” said Shah.

Source: WisdomTree

As such, in the consensus case scenario, gold could reach $2,225 per ounce by the second quarter of 2024, clearing the previous all-time nominal highs of $2,061 per ounce set in August 2020.

Invesco’s Paul Syms, head of EMEA ETF fixed income and commodity product management, was also bullish on the precious metal.

Last month he wrote: “We believe gold remains an asset worth holding especially given uncertainties around the US debt ceiling, any further banking crisis, a correction in stock markets, escalation in the war or countless other geopolitical concerns.”

But things could get even better, said Shah, if we get a scenario where the Federal Reserve “pays heed to the recession warning signs and pivots its monetary policy to cutting rates faster” before inflation is below the target level.

“If the Fed begins monetary expansion by autumn 2023, bond yields will be falling and, assuming it moves before the European Central Bank and other major central banks, we could see the US dollar depreciate at a faster rate.

“We assume inflation will be stronger than in the consensus scenario as a result of the Fed loosening monetary conditions. Assuming that the recession fears that the Fed is responding to are real, we expect positioning in gold futures to remain elevated.”

In this scenario, gold could reach $2,490 per ounce, 22% higher than the all-time high.

The bearish view, which is that inflation falls below the Fed target meaning the central bank overdoes its monetary tightening, would cause the US dollar to appreciate and bond yields to rise.

While this increases recession risk and could be positive for gold as a hedge, it does pose the most risk to the yellow metal.

In this scenario, gold would reach $1,710 per ounce, bringing prices back to November 2022 levels.