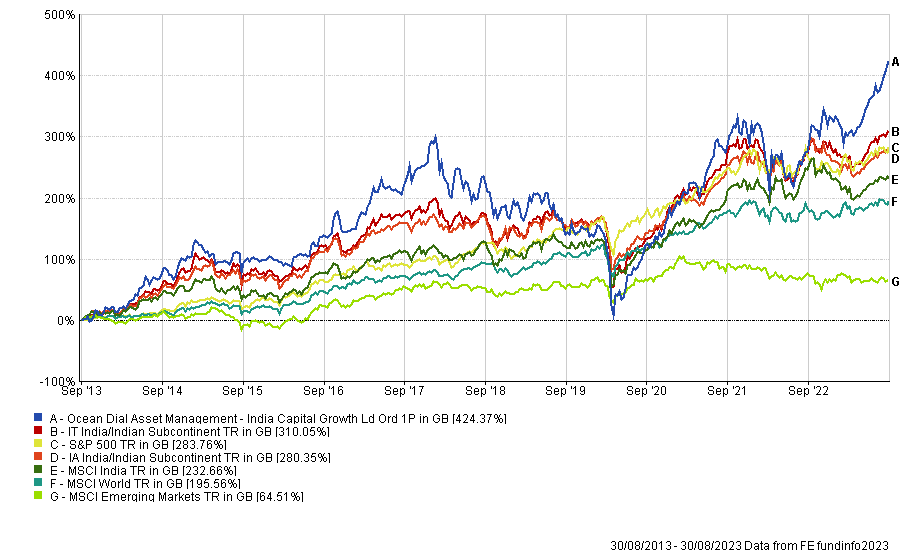

Emerging markets have delivered modest returns in the past 10 years, significantly lagging global indices, but Indian equities have been a hidden gem, outperforming both emerging markets and global indices over this time.

Among the India specialist trusts, India Capital Growth would have been the best bet as it has outperformed its peers in the IT India/Indian Subcontinent and IA India/Indian Subcontinent universes over the past decade. In fact, the trust has even beaten the S&P 500 in a period during which US equities have reigned supreme, and is the fourth-best investment trust across the entire Association of Investment Companies (AIC) space over 10 years.

Performance of trust over 10yrs vs sectors and indices

Source: FE Analytics

Below, the manager Gaurav Narain explains why India deserves a dedicated focus in portfolios and why India will remain the most expensive emerging market.

Could you explain your investment process?

We're bottom up stock pickers and we invest with a long-term view. When we buy a business, it's always for a three-to-five years holding period.

The second thing is that we are quality focused. We buy businesses we believe are predictable, scalable and have some unique selling propositions and don't go into businesses we find difficult to understand.

What do you do differently from your peers?

We focus on the mid- and small-cap segment of the market, which has done well until now.

But I think the difference is more about the stock picking itself. We only buy quality and try to protect on the downside. At worst, the downside is due to a valuation correction or a bit of growth slowdown, but we ensure we don't buy businesses that have structural problems.

What have been your best and worst calls in the past 12 months?

We've had three companies from very diversified businesses grow more than 200% in terms of returns. One is a company called Neuland, which is a pharmaceutical company, another one is Ramkrishna, which is an auto ancillary company and the third is a company called Skipper, which is an industrial company.

On the negative side, City Union Bank has fallen about 30%, over the past 12 months. The company has had a bit of a derating, simply because it’s growing below the industry average, but it has very strong fundamentals with annual returns on assets of about 1.4%. On a long-term perspective, I’m not worried.

Why should investors have a dedicated exposure to India?

India has always grown at a reasonable pace and it is also one of the fastest growing economies in the world today, faster than China. My guess is that this growth will be fairly sustainable over time.

On the top of that, it’s a very well regulated market. So for investors, I think the risk levels are much lower. You shouldn’t club India with emerging markets. It’s a large economy that deserves its individual attention.

Indian equities are sometimes criticised for being expensive relative to emerging markets peers. What do you make of this?

India has historically traded – and will continue to trade – at a premium to emerging markets. There are some structural reasons behind it.

The first is the nature of the market itself, it's very diversified. Unlike, say, most Southeast Asian countries, it is not a commodity heavy market. It has everything from consumption to IT. The range of companies listed in India is very wide. So, the weight of commodity businesses that typically trade on low price-to-earnings (P/E) multiples is much lower.

The second is about the financials of the companies. If you compare India to other Asian countries, you will find that the return on capital employed (ROCE) and return on equity (ROE) of the Indian market is significantly higher.

Also, if you look at India historically, it used to be a capital scarce country. People value capital so all companies are very focused on cash flows and returns simply because the cost of debt used to be 12% to 14%. By nature, people are very cash cautious unlike in a lot of other counties. This is why when you look at the P/E multiples, you also have to adjust it with the fact that the return ratios are higher and that the growth has always been higher.

Adjustments might keep happening, but I don’t see a situation where India would trade at a similar valuation to other Asian markets.

There will be general elections in India next year. Could it impact Indian equities?

It's widely expected that the [Narendra] Modi government will come back into power. The current government is very popular, has done exceptionally well on the development agenda and been very good on execution.

A problem could happen if the opposition tries to gobble up all parties together and unite against this government as one opposition bloc. If they succeed to some extent and the government gets a weaker majority or doesn't come into power, then there will be a short-term fall in the market because the current government is very development and business friendly.

The trust is trading on a 5% discount at the moment. Is that normal?

The board is very focused on managing and reducing the discount. When I came in about a decade ago, we were trading at a discount over 20%. It has settled down at 14-15% in the past few years and it has been in the 6-8% range in more recent times.

We've done a lot to try to reduce the discount and have a redemption window every alternate year in which we give investors a redemption option at a fixed 3% discount. That has ensured that investors always have an option of redeeming at a much smaller discount.

What do you do outside of fund management?

I'm a big foodie, I love travelling and spending time with my dog back home. We go on long walks together in the early morning.