UK equities have faced a turbulent few years, with shifting leadership and sharp rotations testing even the most experienced managers.

Liontrust UK Equity navigated this backdrop well in 2023 and 2024, delivering first-quartile returns in the IA UK All Companies sector in both years, but it fell short in 2025 as stock-specific setbacks, an underweight in banks and the de-rating of software and data names weighed on returns.

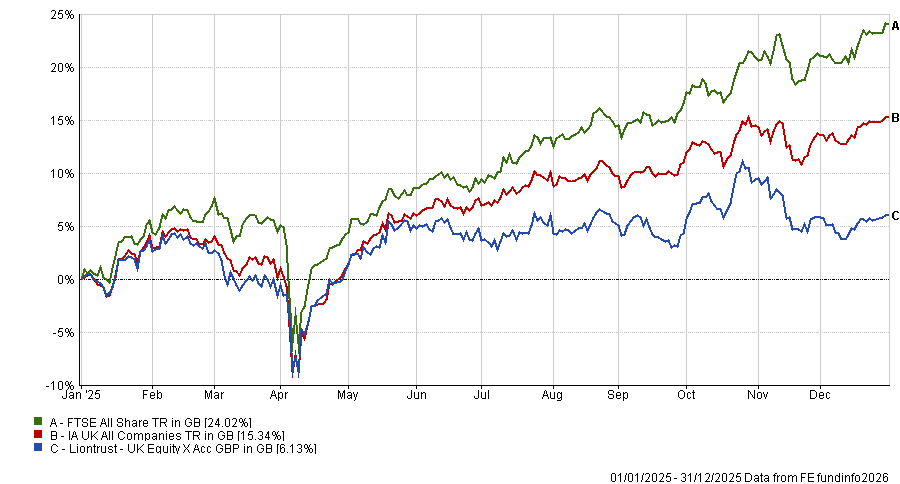

The fund gained 6.1% – less than half of the 15.4% sector average – while the FTSE All Share made 24%.

Performance of the fund vs benchmark and sector in 2025

Source: FE Analytics

Imran Sattar, manager of Liontrust UK Equity, said: “2025 was a difficult year – the toughest year of my career.”

When reflecting on this underperformance, he first highlighted the fund’s overweight position in UK bakery chain Greggs as a detractor, noting it had two profit warnings following a slowdown in sales growth in 2024.

Sattar, who is also lead manager of Edinburgh Investment Trust and Liontrust Income, said Greggs was impacted by a tougher consumer backdrop in the UK and is continuing to invest in future growth – both factors weighing on near-term margin progression.

“We also didn’t have enough in banks – and those were on a tear in 2025,” Sattar said.

“We owned some and made good money in them in 2022 and 2023 but, in hindsight, the position simply wasn’t large enough relative to the benchmark.”

As of 31 January 2026, NatWest Group is one of Liontrust UK Equity’s top five overweights at 3.4%, while HSBC is one of the biggest underweights in the portfolio.

The fund also had a “significant overweight” in data and software companies in 2025, including LSEG, RELX and Sage, Sattar said.

“All of these companies have been de-rated over the past 12 to 18 months, despite producing strong results,” he said, adding that the de-rating “centred on AI-related fears”, with investors concerned that AI will be able to replicate and ultimately replace the core functions and infrastructure such companies offer.

The fund did log some successes, however, with Sattar highlighting National Grid as an example.

Liontrust UK Equity bought a large position in the company at the end of 2024. “With economies electrifying because of AI, data centre needs and electric vehicles, it is clear we need more grid infrastructure and National Grid is a good way to play that,” he said.

“In this way, I like high-quality businesses with structural growth tailwinds and durable competitive advantage.”

Learning from mistakes

Nonetheless, Sattar said that “good investors learn from their mistakes” and has been tweaking the portfolio in recent weeks.

“In hindsight, I should have been braver on banks, so I have added to them,” he said, noting that “they have been relatively weak [so far] this year, which has given us opportunities”.

More broadly, Sattar said the portfolio was also “a bit too aggressively growth-biased and not balanced enough with value”.

“I am not a dogmatic investor – I am flexible enough to understand that there are many ways of making money and that there are stock market cycles just as there are economic cycles,” he said.

“I have biases towards growth, quality and economic moats but I am perfectly happy to own value stocks alongside.”

As such, Sattar has added a few names with more of a value tilt over the past 12 months, including building products company Marshalls and brick manufacturer Ibstock.

“These are small starter positions but represent a more balanced portfolio than we had in mid-2025, when it was a bit too growthy,” he said.

Looking ahead

Despite a bruising 2025, Sattar remains optimistic about the UK market in 2026.

“I’ve spent around 28 years looking after UK equity funds and clearly the shape of the market has changed in that time, but the performance of the UK equity market as a whole has actually been decent given the backdrop,” said Sattar.

He noted that the set of investment opportunities in the UK is far deeper and broader than it was at the start of his career.

“One of the criticisms of the UK market 20 or so years ago was the concentration in banking, mining, oil and telecoms. While some of that concentration still exists, the index is much broader today,” he said.

“It remains a really interesting pond to fish in to build a portfolio that is globally oriented, not just domestically focused, and full of companies with powerful economic moats at attractive valuations.”

However, with further volatility brewing on the horizon – spiked by the ongoing conflict in the Middle East – Sattar acknowledged the 15% per annum which the fund has compounded in markets over the past three to five years is “unlikely to continue at the same pace”.

“But my conviction in the portfolio is at an a ll-time high, [as] the companies we own are delivering very strongly operationally, strategically and financially, and that gives me confidence,” he said.