Not every fund manager desires for their fund to lead the pack. For Mark Peden, co-manager of the $1.2bn Aegon Global Equity Income fund, the goal is to be consistent “and let the long-term compounding take care of itself”.

He aims for the bottom end of the top quartile or the top end of the second quartile each year. The fund has delivered a first or second quartile return in the IA Global Equity Income sector in seven of the past 10 years.

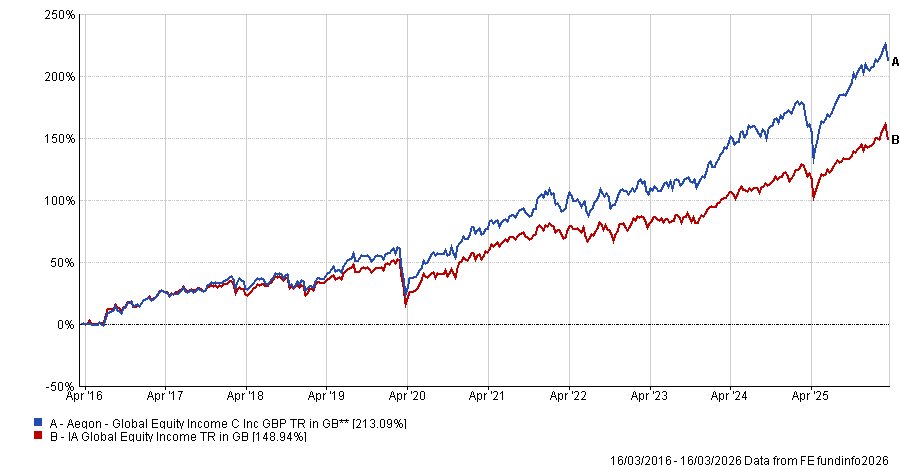

Performance of the fund vs sector over 10yrs

Source: FE Analytics

“We have beaten the median fund in the IA Global Equity Income sector every single year since launch – so 13 consecutive years of above‑median performance,” Peden said, adding that, as a result, the fund has compounded at over 12% since launch.

Below, Peden explains what constitutes a quality business and why he owns technology stocks in his income portfolio, including Microsoft and TSMC.

What is the main focus and investment process of the fund?

Aegon Global Equity Income does exactly what it says on the tin – it’s a 100% plain vanilla, long-only equity fund structured around 40 to 50 strong dividend-paying companies which have strong balance sheets and deliver good returns on equity.

We have two performance objectives. The first is the income objective, which is to distribute an around 30% premium income stream compared to the market. Given where markets are currently trading, with MSCI ACWI on roughly a 1.7% dividend yield, equity products aren’t delivering a huge amount of income in absolute terms but it is an income stream that grows – we delivered 9% growth in our income last year.

The other objective is to deliver the best total returns in our sector through our quality income strategy.

It’s very much a large-cap strategy as well – if you sift through the portfolio, you will recognise many of the names.

How do you approach geographic allocation in the fund and what regions are currently most attractive?

We are currently invested in 14 different geographic markets across 10 different super‑sectors.

Our geographic allocations haven’t changed much in recent quarters, although we have added a bit more to Europe with around 26% of the fund now invested there. It is a natural hunting ground for equity income because it’s a decent yielding region.

In contrast, people get preoccupied with tech, as if the US only performs if tech performs. But the US is still an incredibly deep market and we think there is a huge variety of ways to invest there, with 55% of the fund invested in US equities.

We have also had a longstanding structural preference in non‑Japan Asia, where we currently have just under 20%. We have run that full allocation for many years. A lot of Asian markets have the characteristics that suit us: they pay decent yields, they provide good income and earnings growth and valuations are still good. This includes markets like Singapore, Hong Kong, Australia and Taiwan.

How do you define ‘quality’ and how does that shape the way you construct the portfolio?

There is a quiet strength to quality. For us, quality means a strong balance sheet, good return on equity and the ability to keep growing cash returns to shareholders. It is sector‑agnostic and very stock‑specific.

We have been running a barbell strategy, with just under a quarter of the fund in what we define as quality financials. Within banks, we own JP Morgan and Morgan Stanley, alongside DBS in Singapore, Macquarie Group in Australia and DNB in Norway – all very high‑quality institutions.

We have balanced that exposure with a full allocation (roughly 20%) to quality tech stocks.

Within semiconductors, for example, we own TSMC – but who doesn’t own TSMC? You could argue it is one of the best, if not the best, companies in the world.

We have also owned Microsoft for many years. We bought it when it yielded 3% and it has been a five‑bagger for us. It now yields 0.8% but remains extremely high-quality despite all the AI‑disruption paranoia.

Across sectors the same quality theme holds – for example, in materials we own industrial gas companies like Linde in the US, which has grown its dividend for nearly 40 consecutive years.

What have been your best calls in the past 12 to 18 months – and your worst?

Our best performers were the AI winners. Delta Electronics, a Taiwanese power‑management company, more than doubled last year because it’s tied to the data centre build‑out. Broadcom followed, with its AI chip‑design capabilities and close ties to Google.

TSMC is one of the most obvious beneficiaries of the AI build-out. Microsoft, Google, Amazon, Meta – they are all spending hundreds of billions on AI infrastructure and the money has to go somewhere. TSMC is the only company in the world that can supply chips at the required volume.

However, some of our detractors are the AI losers – with some companies that initially benefited from the AI tide being caught out.

We bought Accenture in October 2024 – that turned out to be a mistake as these large people-based businesses look vulnerable to AI disruption. We sold it in August last year, and it has continued to underperform.

We also owned Automatic Data Processing (ADP), which we had held since September 2020 and sold earlier this year. It made us good money over the years, but it too has been caught up in fears that AI could replicate its payroll software.

In terms of attribution: Accenture cost the portfolio 75 basis points (bps) of relative performance last year and ADP cost us 79bps. On the positive side, Delta Electronics contributed 146bps, Broadcom contributed 102bps and TSMC contributed 102bps.

How do you expect the AI surge to play out?

The jury is still out on a lot of companies and the market tends to shoot first and ask questions later. Throughout the rest of this year, the market will keep hunting for where AI will disrupt operations, while the sell‑off in professional‑services firms and enterprise‑software companies reflects fears that they will be hit hard.

We are in a technological paradigm where nobody fully knows what an AI‑driven world looks like. Fund managers need to stay laser‑focused on understanding who the winners and losers are going to be.

What do you enjoy doing outside of fund management?

Outside work, walking is my big thing. I’m a very avid walker. I also watch every sport I can.