Latin America represents some 7% of the world’s GDP, yet it is just 10 basis points of a typical global market tracker, according to BlackRock’s Sam Vecht.

Even among emerging markets – where most Latin American countries tend to sit – the group makes up just 7% of most indices.

“We sit in a world today where – and you may not know this – Samsung is about the same weight as all of Latin America in an Emerging Market Index, and TSMC is about twice the weight,” he said.

“I'm not saying there's anything wrong with TSMC or Samsung – they may be great companies – but the construct of an emerging market index today means that even if one overweights Latin America, it is at best a fringe allocation and at worst an irrelevant one.”

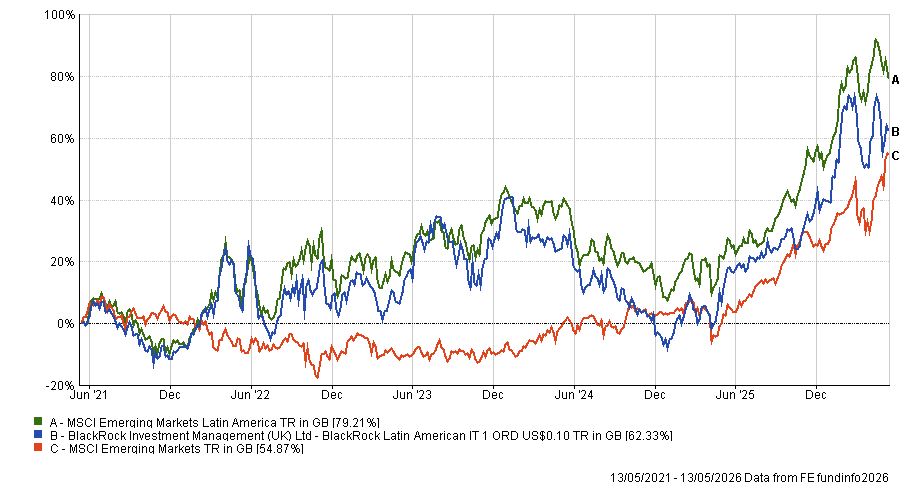

This is despite pretty strong performance. The MSCI Emerging Markets Latin America benchmark is up 79.2% over the past five years, ahead of the wider MSCI Emerging Markets index. Vecht’s BlackRock Latin American trust has made 62.3% during this time, as the chart below shows.

Performance of trust vs indices over 5yrs

Source: FE Analytics

Below, Vecht tells Trustnet why getting out there in different countries matters as much as meeting companies and how emerging market investors are like schoolboys playing football.

What is your process?

Our process is a combination of bottom-up and top-down principles. About 70% of our risk is bottom-up, we incorporate top-down insights – about politics, macroeconomics, fixed income and currencies – into our process.

It's critical that we spend time on the ground in the countries we invest in. We have spent time not just in Brazil, Mexico, Peru, Colombia and Chile, which are in the index, but also in places like Argentina, Guyana, El Salvador, Costa Rica, Panama, and lots of places that aren't in the benchmark.

It's not just about seeing the companies we invest in – it's also about understanding the society we invest in. So we will see accountants, lawyers, students, diplomats, politicians. It's about investing in a country understanding its society.

When it comes to the bottom-up, we typically meet companies, customers, suppliers and competitors. We build discounted cashflows on the companies we invest in and have target prices.

What have you got wrong in recent years?

Latin America and emerging markets in general have been in a bear market for most of the past 20 years. The Brazilian market isn't very different in price terms from where it was two decades ago.

The increasing behaviour of emerging-market managers and Latin American managers is to crowd around whatever has been working in the recent period. Right now, in an emerging market context, everyone is focused on AI.

About a year and a half ago everyone was focused on India. Three years ago it was ESG opportunities and five years ago everyone was focused on Chinese platform names.

It’s a bit like watching seven-year-olds play football. You know where the ball is because that's where you've got 18 little boys running. It's not the best way of scoring goals or thinking strategically about portfolio construction.

That's the reality with emerging market and Latin American fund managers – in part because so little has worked here. Unlike in the US, where you've had [beta] as a tailwind, in emerging markets and Latin America you haven't.

That's a long introduction to what I'm trying to say: when we think about the things we've got wrong, there has been a very conscious decision to stay away from some areas that everyone else finds very hot. They've probably got hotter and we've stayed away – and that's hurt us in relative performance.

Conversely, some of the things we've got very wrong over the past six, 12 and 18 months have been things that were already very out of favour and have become even more so. In particular, domestic Brazilian names, where companies that used to trade on 20 times earnings now trade on seven times.

What has helped performance?

What's helped the portfolio over the past 18 months, broadly, is that we've had leverage and the asset class has gone up, so the investment trust has amplified our returns.

What else has been helpful is we've owned mining companies that may not be listed in Latin America but whose operations are entirely in Latin America – across a variety of different mining sectors, whether gold or copper.

Does the trust hedge its currency exposure?

We are not focused on returns in reals or pesos – our functional currency is dollars.

If we thought – which we don't currently – that one of the currencies was going to fall very meaningfully, our general approach would be to avoid or underweight it.

Unlike in the UK, where the pound can weaken and the FTSE can go up, the reality of most of Latin America at almost all times is that when the currency goes down 10%, the market goes down 20%, and you lose 30% very quickly.

Why is looking at the top-down so important?

It is absolutely critical. It doesn't mean it's always easy to do, but we do have a view on the politics, macroeconomics, fixed income and currencies across all the markets we invest in. Do we always get it right? Of course not. But that's our job, and that's actually what makes investing in Latin America so much fun and interesting.

There are these different ways of adding return for clients. If you're investing in the Nasdaq, you've essentially got one dimension – one thing you can get right, one you can get wrong.

Here, you've got choices between countries, sectors, styles, currencies – so many different dimensions to think about. It's a much more challenging intellectual exercise. Of course, that means one can get a lot more wrong. But it also gives the opportunity of getting a lot more right.

Does that mean there’s more turnover?

You have to be prepared to move when things go wrong. But if you look at the trust over the past few years, turnover isn't that high.

Some years it's been around 40%, sometimes around 60% – so you're looking at roughly a two-to-three-year holding period, which in my mind isn't particularly exciting or unexciting.

But you have to be prepared: you have a thesis, you think this is a great investment, and then something happens and you have to be able to get out. You don't want to be stuck in illiquid positions – that's an important rule in emerging markets.

But you also have to be prepared to say: ‘I've been saying this for three years and actually it's rubbish. Something has happened and I've been proved wrong.’

What do you do outside fund management?

Football is a big part of my life. I support Spurs and play a couple of times a week. I'm completely hopeless, but I play eight-a-side and six-a-side at left wing back. I’m not very good but I try.

I also have five wonderful kids. They occupy a lot of my time, along with my wife.