TSMC is such a large part of the MSCI Emerging Markets index that managers “cannot leave it out”, according to Michael Bourke, who runs the M&G Global Emerging Markets fund.

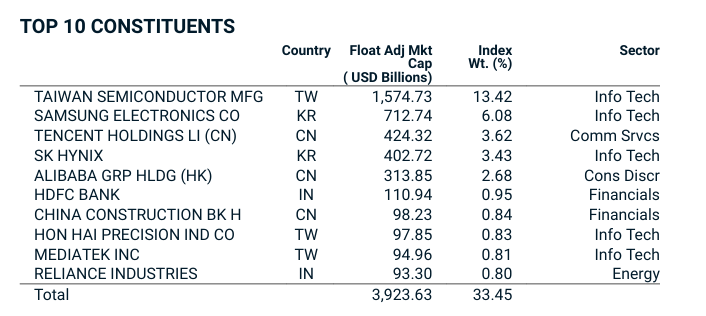

Leading semiconductor foundry TSMC has grown significantly in recent years. It now stands at 13.4% of the MSCI Emerging Markets index and is the only non-US stock in the MSCI AC World’s top 10, accounting for 1.6% of the global equity including emerging markets index.

“Global managers own it by choice but emerging market managers own it by benchmark compulsion,” said Bourke.

For emerging market managers, the company’s weighting in their benchmark index is above the limit available when running a UCITS fund, with rules dictating that no stock can be worth more than 10% of a portfolio.

Percentage of TSMC in MSCI Emerging Markets index

Source: MSCI

As a result, all managers in the IA Global Emerging Markets sector must be underweight the stock, but that is a different proposition from avoiding the company entirely.

In his M&G Global Emerging Markets fund, Bourke has an 8.3% holding in TSMC, which highlights both his belief in the stock but also the risks that surround it.

“It’s a systemically important company in our view. It is the monopoly provider of leading‑edge semiconductor logic chips,” said Bourke, noting these are used in everything from AI to smartphones.

“It happens to be in this incredible sweet spot, which of course explains the 13% weight and why it’s gone from say 7-8% of the index two years ago to where it is today,” he said.

TSMC’s shares have almost doubled (up 94%) over the past year and the stock has “incredibly strong” momentum, but Bourke noted that he looks at companies by asking more long-term questions: what is the profitability; what is happening with the company right now; and how will it evolve over the next three-to-five years?

Performance of stock over 12 months

Source: Google Finance

“We think in this long‑term view, because we know short‑term momentum may fade and we could be whipsawed if we’re too short-term,” he said.

The M&G Global Emerging Markets manager noted that the stock is in a strong position within the global tech boom with “huge demand” for its products. This is complemented by improving margins.

On top of this, TSMC is not too expensive, sitting on a price-to-earnings of around 30x (currently 33x). While this is high compared to the average emerging market stock, he noted that if the company can continue to grow and compound at its current levels over the next three years (something he believes is the base case), it represents good value.

However, he said the risks around the stock are “manifold”. Firstly, there is concern that there could be a slowdown in the implementation of AI, something that would hit the stock as it is “at the epicentre” of the technology boom.

“Even a slowdown – not obliteration – would matter,” he said.

Then there is political risk, which he said is the “least discussed point” but one that warrants understanding. Taiwan functions as a sovereign, democratic state with its own government, but China sees it as a breakaway province that will come under its rule – threatening military action if necessary.

This threat has impacted TSMC, with customers more sensitive to a potential disruption in the supply of semiconductor chips that would be brought about by conflict.

As such, the company is striking deals with other countries, including investing in the US to diversify its geographic footprint. Bourke noted that, as part of the CHIPS & Science Act, the company has already invested $25bn in Arizona to build a manufacturing complex, with the total potentially reaching as much as $125bn across five sites.

“Diversification is exploding to satisfy US customer concerns around supply‑chain resilience,” he said.

On a three-to-five-year view, the stock must continue to spend capital to improve its position. This would amplify any slowdown in the AI trade, as there would be a disjoint between the investment made by TSMC and its profitability.

“We’re not there yet, but that’s a risk on the horizon,” said Bourke, adding that the company is “uniquely sensitive” politically, geographically and due to the sector it is in.

These risks have caused the manager to start trimming his position, but he is not “ready to accelerate yet” as he remains watchful over the company’s profitability and its language around future investments.

“At what point could that get out of sync? We’re not there, but it’s on our radar,” he concluded.