Japan’s stock market has been on a trajectory of new heights, with the Nikkei 225 index hitting an all-time record high this year – the first time it has achieved this in 34 years.

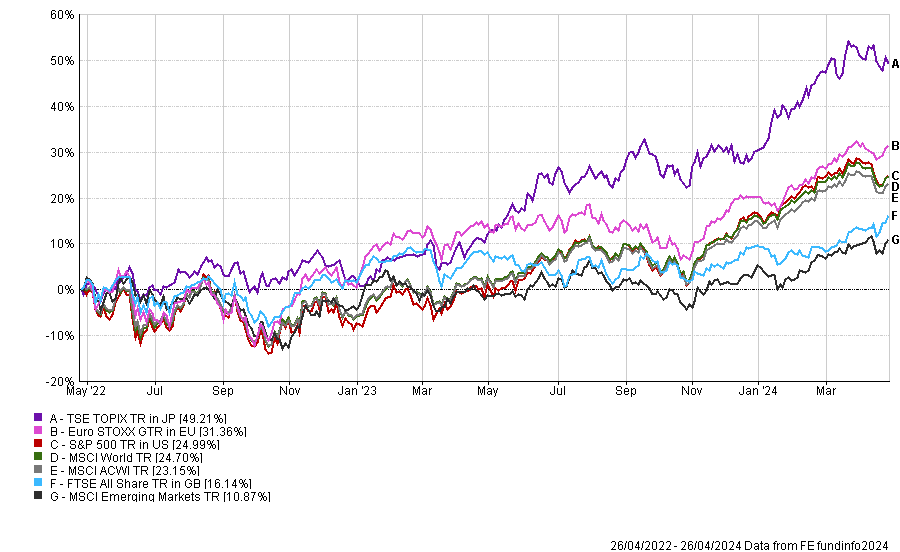

Yet much of the returns have been in local currency thanks to the weakening of the yen. Indeed, over two years, the TSE Topix index – another popular Japan equity benchmark – has been the best performing major market in local currency terms, as the below chart shows.

Its 49.2% gain is almost double that of the much ballyhooed US S&P 500 index, while the European Euro STOXX index took second place, up 31.4%.

Performance of indices over 2yrs

Source: FE Analytics

For UK investors the returns have been more muted. In sterling terms, the Japan index drops down the pecking order substantially.

Indeed, Euro STOXX is top with a return of 33.4%, followed by the S&P 500 (26.6%) and the broader MSCI World (24.2%), which is largely dominated by the US names. The TSE Topix sits in fourth with a total return of 22.2%.

Despite this, returns have still been strong. Kate Marshall, lead investment analyst at Hargreaves Lansdown, said investors will now have to ask themselves whether they’ve missed the boat or if Japan’s market has further to go.

“Like the US, which has been led by the ‘Magnificent Seven’, Japan has benefited from a narrow group of stocks performing well, dubbed the ‘Seven Samurai’. This includes some of Japan’s largest companies, including car maker Toyota and semiconductor companies such as Tokyo Electron,” she said.

“In some cases, their valuations have become stretched. But this doesn’t apply to the entire market. Small and medium-sized companies, on average, currently look better value. And, as a whole, Japan’s market still looks good value compared with other global markets and its own history.”

There could be more catalysts for future growth ahead. For example, Marshall highlighted the end of negative interest rates earlier in 2024 could be followed by another rate hike later in the year if inflation remains around 2% and wages continue rising.

“This could be good news for economic activity, partly because there’s a huge amount of savings in Japan, most of which hasn’t been earning anything in interest. Higher rates could change this, boosting spending and stimulating the economy,” she said.

“However, higher rates could mean that cash becomes more attractive relative to equities for local investors, as we have seen in the UK in recent years – it is a fine line that the central bank will have to navigate.”

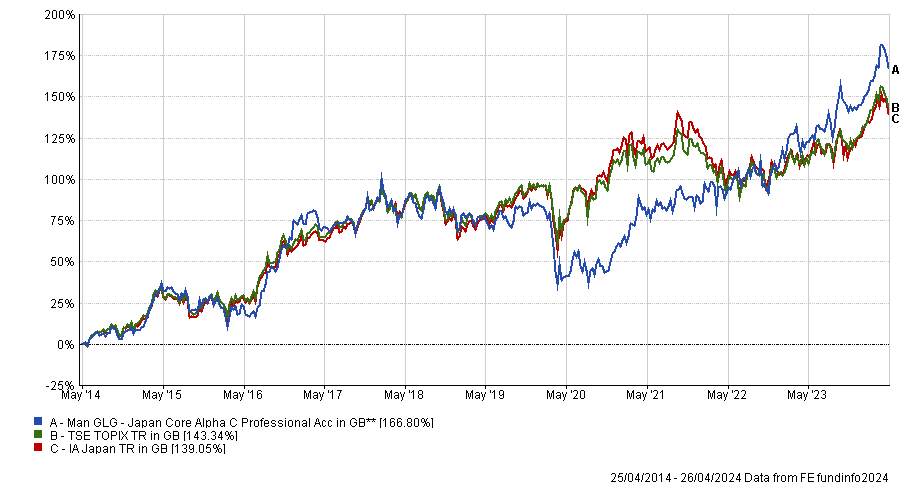

For those wishing to get in now, Marshall highlighted three potential fund options. The first is Man GLG Japan Core Alpha managed by Jeff Atherton and Adrian Edwards alongside recently appointed co-managers Emily Badger and Stephen Harget.

The £2.2bn fund focuses on larger Japanese companies, using a contrarian approach often known as 'value investing'. They buy out-of-favour companies and gradually sell them as they recover.

“The fund could work well in a global equity portfolio designed to provide long-term growth. Its focus on large companies means it could sit well alongside a Japanese equity fund focused on medium-sized or smaller companies,” she said.

The Man GLG fund has been a top-quartile performer in the IA Japan sector over one, three, five and 10 years and was the third best performer since April 2021.

Performance of fund vs sector and benchmark over 10yrs

Source: FE Analytics

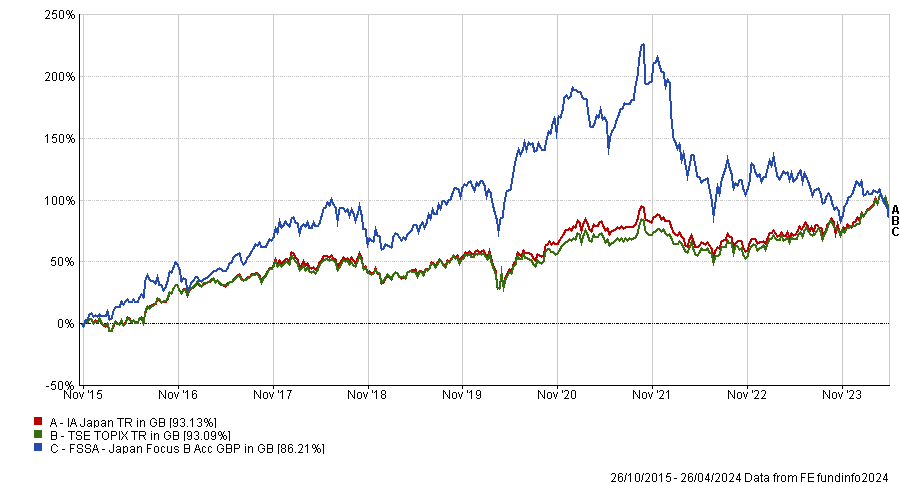

Second is FE fundinfo Alpha Manager Martin Lau and Sophia Li’s FSSA Japan Focus fund. At £81.6m it is much smaller than its Man GLG rival.

It invests with a quality-growth style across the large and mid-cap range of the market, as well as backing more domestically focused Japanese businesses.

“The fund could help diversify a global investment portfolio. Its focus on high-quality companies with the potential for above-average earnings growth means it could work well alongside other value-focused funds,” said Marshall.

It’s performance however has not been so sharp. Indeed it has been a bottom-quartile performer in the IA Japan sector over one, three and five years. Much of this has been over the short term, with the fund down 9.6% in just the past month.

Performance of fund vs sector and benchmark over 10yrs

Source: FE Analytics

Over three years it has lost 31.3%, although since launch in 2015 it has done slightly better, climbing to the third quartile of the sector. A year ago, the fund had been the fourth best performing fund in the sector – before its recent fall from grace.

Lastly, for those unwilling to take the risk with an active manager, iShares Japan Equity Index is Marshall’s preferred option for simply tracking the market.

“It provides low-cost exposure to large and medium-sized companies in Japan and aims to track its benchmark, the FTSE Japan, by investing in every company in the index,” she said.

“An index tracker fund is one of the simplest ways to invest. This fund could be a great, low-cost starting point to invest in Japan in a portfolio aiming for long-term growth.”