Large-caps may have dominated global equity markets over the past decade but fund managers believe the next 10 years are unlikely to be as one-sided.

A recent Trustnet analysis of 18 major indices showed that large-caps outperformed in every region except Europe in the decade ending May 2026, driven by a perfect storm including ultra-low interest rates, passive flows and AI-related enthusiasm.

Trustnet asked fund managers whether they expect large-cap dominance to persist or whether they expect a widening of leadership across the market capitalisation spectrum.

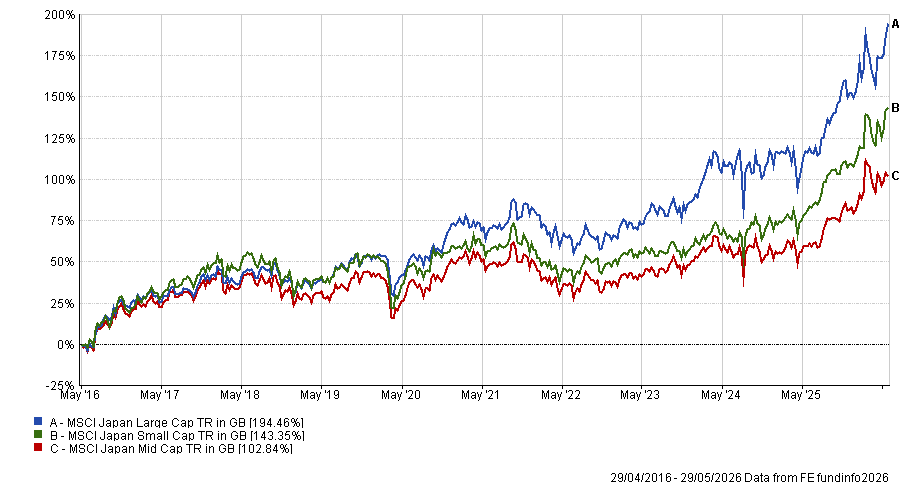

Japan

In Japan, large-cap exporters and global industrial leaders benefited from a weaker yen, improved corporate governance and strong inflows from foreign investors.

Performance of Japan’s large-, mid- and small-caps over 10yrs

Source: FE Analytics

While all these factors pushed large-caps higher, some managers argued that the longer-term benefits of governance reforms will be especially felt across smaller companies.

Joe Bauernfreund, manager of AVI Global Trust and AVI Japan Opportunity Trust, said that such reform takes longer to be priced in.

“But it will be transformational,” he argued, noting that small- and mid-cap companies, which make up 65% of the Japanese universe, have the most to gain as regulatory pressure turns disclosure into action.

The signs are already there, with buybacks and takeover bids hitting “historic highs and cross-shareholding unwinds accelerating, driven by a coordinated push from the TSE [Japan Exchange Group], the government and domestic asset owners”.

Shareholder activism is increasingly shaping capital allocation into the country’s small- and mid-cap companies, according to research from the Japan Research Institute.

Rather than simply calling for better governance, investors are increasingly pushing smaller companies to deploy excess cash through buybacks or to pursue strategic deals, including tender offers and management buyouts.

Companies valued at less than ¥100bn currently represent more than half of companies targeted by activists, the research said.

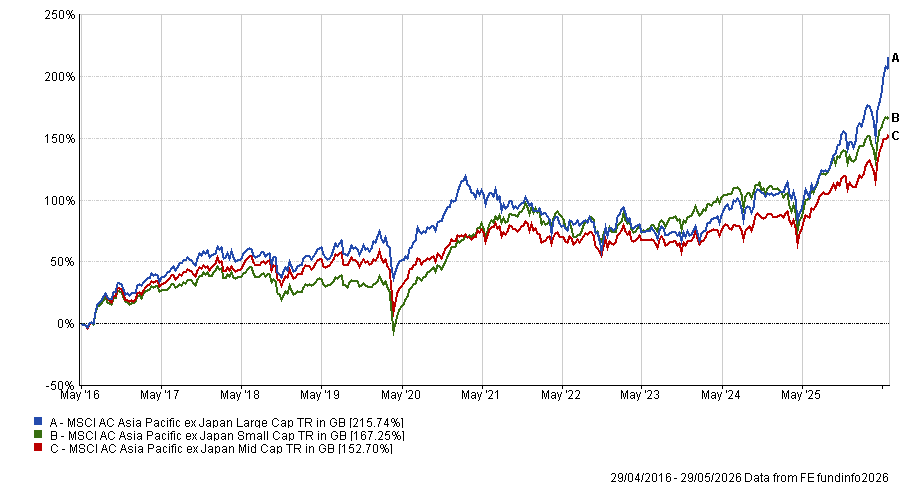

Asia-Pacific

Looking at the Asia-Pacific region more broadly, the impact of tech-focused large-caps in select countries – such as South Korea, Taiwan and China – has skewed the overall picture.

Yoram Lustig, head of global investment solutions in EMEA at T. Rowe Price, said: “[Across Asia] performance became increasingly concentrated among a small group of dominant regional champions, particularly TSMC, Samsung, Tencent, Alibaba and Reliance Industries.

“Like the dominance of the Magnificent Seven, these firms captured a disproportionate share of earnings growth, index returns and capital flows.”

Performance of Asia-Pacific ex Japan large-, mid- and small-caps over 10yrs

Source: FE Analytics

However, Robin Black, co-manager of Aegon Global Equity Income, noted that tech stocks in Asia have quickly re-rated and are no longer cheap.

“If hyperscaler capex slows, a market correction is likely,” he predicted.

Technological innovation is also expected to create opportunities beyond established market leaders, with smaller companies enabling or adopting AI likely to emerge as important beneficiaries in the years ahead.

Meanwhile, Bauernfreund pointed out that not all large-caps are performing as strongly as it may appear.

“In South Korea, for example, if you strip out the two largest names in the KOSPI, Samsung and SK Hynix (which account for 52% of the index), the rest of the Korean market returned just 5% in May 2026 versus 29% for the headline index,” Bauernfreund said.

“When a single theme drives that degree of concentration, it raises a legitimate question about sustainability over the next decade.”

In addition, he said small- and mid-caps in South Korea, in particular, are set to benefit in the longer-term from governance reforms designed to materially strengthen minority shareholder rights. So far, the re-rating has “barely begun beyond the index heavyweights”.

“Like Japan, smaller companies have been the slowest to feel the effects of reform, which is why the most exciting returns over the next decade may not come from the widely owned larger names,” Bauernfreund said.

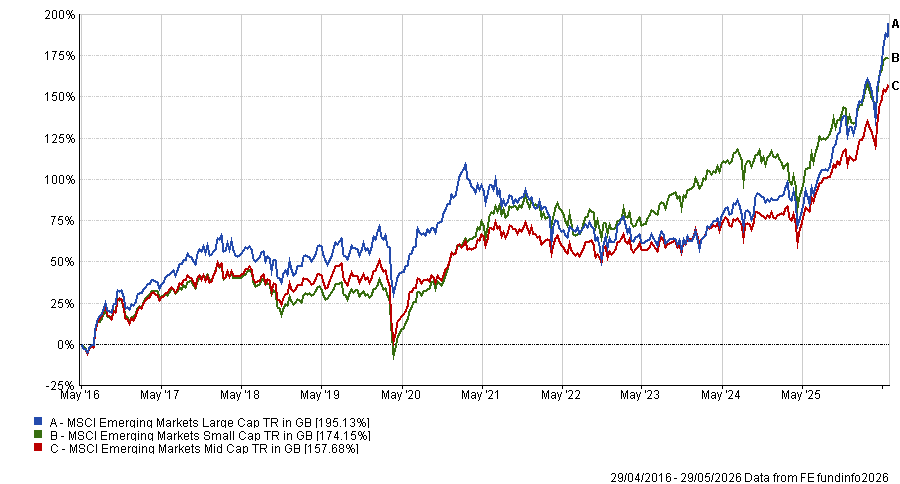

Emerging markets

While AI has played its part, Mike Sell, head of emerging markets at Alquity, said it is important not to overlook other significant structural trends that are taking root across emerging markets and have attracted less investor attention.

One example he gave is large fintech companies addressing severely underpenetrated consumer credit and online financial services markets in countries such as Egypt or India, pointing to large-cap stocks like Valu and Billionbrains.

Performance of emerging markets large-, mid- and small-caps over 10yrs

Source: FE Analytics

Yet Sell said smaller companies have still performed strongly, claiming emerging market small-cap stocks have outperformed large-caps in eight of the past 14 years.

“We believe this trend could strengthen over time, as smaller companies are often more agile and better positioned to adopt new technologies quickly,” he said, adding that they also diversify portfolios by providing more balanced exposure.

Alongside AI and fintech developments, emerging markets are benefiting from a wave of population growth, with T. Rowe Price’s Lustig pointing to the expansion of the middle class and broadening economic growth across regions like India and China.

“This creates a favourable backdrop for smaller and mid-sized companies that are more closely tied to domestic growth opportunities,” Lustig said.

“As a result, I would expect market leadership to become less concentrated over the next decade, with the performance gap between large- and small-cap stocks likely to narrow.”

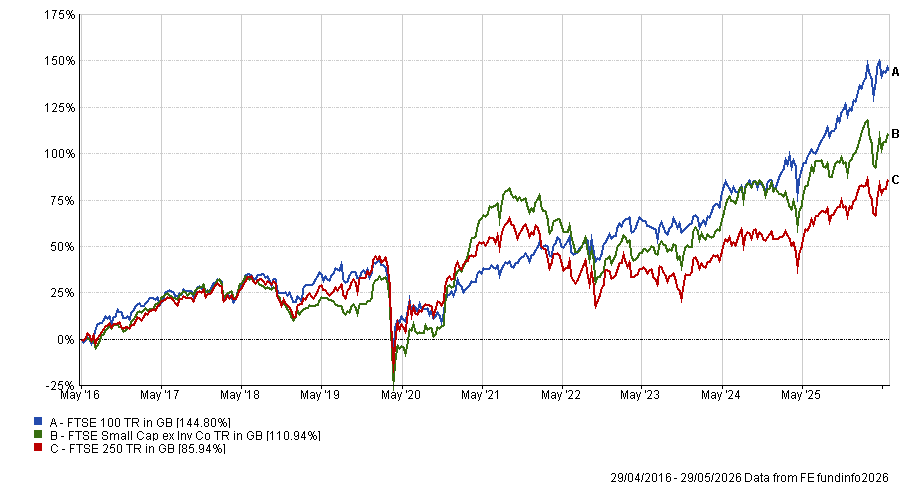

UK

When it came to discussing the UK, managers were quick to acknowledge the underperformance of mid- and small-caps driven by exceptionally weak sentiment, following years of political uncertainty, Brexit-related concerns and a lack of domestic investor demand.

Performance of UK large-, mid- and small-caps over 10yrs

Source: FE Analytics

As such, they agreed that the UK offers perhaps the strongest case for small- and mid-cap recovery – and therefore better returns – over the next decade.

Philip Matthews, manager of IFSL Wise Multi-Asset Income said: “Many [small and mid-sized] businesses emerged from a challenging period with strong balance sheets, growing dividends and robust cash generation.”

He added that depressed valuations – both relative to history and larger companies’ – mean that small- and mid-sized UK companies have “significant scope” to re-rate.

Paul O’Neill, chief investment officer at Bentley Reid, added: “On the basis that stock prices improve the most when things stop getting worse (as opposed to when things get better), I struggle to see how much worse things can be than they have been for the past decade.”

US

With the drivers of US large-cap dominance well documented, the focus now turns to whether smaller companies can close the gap.

Indeed, Richard Scrope, manager of VT Tyndall Global Select, said the valuation gap between large- and small-caps has “seldom been wider”, with greater upside potential for investors backing smaller businesses.

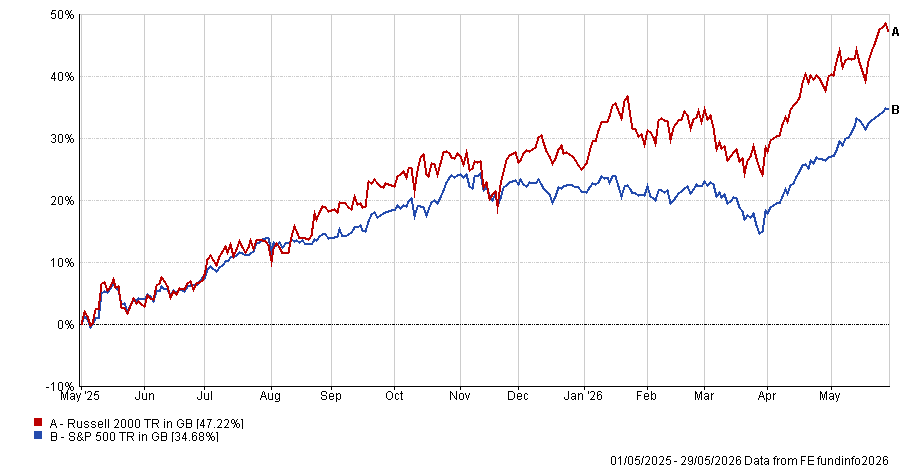

It could be argued that change is already on the cards. Over one year to the end of May 2026, Russell 2000 outperformed the S&P 500, posting a 41.4% return versus 28.3%.

Performance of S&P 500 vs Russell 2000 over 1yr

Source: FE Analytics

However, Mark Ellis, chief executive officer at Nutshell Asset Management, is cautious about calling it a regime change this early.

“The Russell 2000 has a very different composition to the S&P 500 – it is more domestically exposed, more rate-sensitive and includes a higher proportion of lower-quality or less profitable businesses” he noted.

Nonetheless, Bentley Reid’s O’Neill argued there is a credible scenario in which US small- and mid-sized companies close the gap to the S&P 500 over the next 10 years, as investors look for opportunities to diversify beyond the dominant mega-caps.

Should the Magnificent Seven run into issues, such as capacity constraints, data costs rising or user levels being lower than expected, then O’Neill expects the pace of flows to small- and mid-caps to “increase significantly”.

“If protectionism continues to rise, if business on a large scale gets harder, if support for small- and mid-caps gets better, then inflows will shift and the cycle can become self-fulfilling,” he added.

“I wouldn’t bet my whole portfolio on it but there are credible scenarios where US small- and mid-caps close the gap for sure.”